How much upside is left for NXT?

When we started the Montgomery Small Companies Fund 12 months ago, data centre operator NEXTDC (ASX:NXT) was one of the first businesses we bought. On our analysis, the shares were cheap. One year on and the share price has almost doubled. NXT continues to be a great business but, at current prices, is it still a good investment?

Recap: what’s happened – “problems” resolved

At $6.50 back in October 2019 the market was fixated on two things; NXT’s earnings growth had hit an ‘air pocket’ driven by delivery problems with S2 (its huge Sydney data centre development) and the company’s ability to fund the growth pipeline. On our assessment it was those issues that were causing the shares to trade at just half of the $13 long term valuation we had for NXT back then.

Problem 1 – Tick: Earnings “air pocket” gone and certainty clarified. NXT management delivered S2, and that development is now sold out. Investors now view the company’s next data centre development in Sydney, S3, as an asset that can’t come quickly enough rather than wondering if it would get built at all. The earnings “air pocket” is now long forgotten, as it should be. Next year’s earnings is a pretty useless yardstick with which to assess value in a growth business developing and operating 30+ year assets.

Problem 2 – Tick: Capital raised and growth funding assured. NXT’s growth is capital intensive, however the company has a proven track record of developing multiple datacentres (9 and counting) having to date organically deployed $1.5 billion, building from scratch arguably the highest quality connectivity-neutral datacentres in Australia. Management have built these (mostly) on time and on budget and have demonstrated consistent returns on capital in the range of 15-20 per cent EBITDA/Capital, unlevered.

These returns are great, and these are 30+ year assets. Put your hand up if you want some of that!

As it turned out, when NXT asked that exact question lots of investors did, and the company executed a $860 million equity raise that transformed the balance sheet and its ability to fund its growth potential. Long term high returning assets, growth driven by structural themes deserve long term thinking. That $860 million was gobbled up quick smart and at $7.80 it was a bargain.

The Future – Big runway, big growth, big dollars

As corporates and consumers the world over have adjusted their operating posture and daily habits to cope with the challenges of COVID-19 they have gone digital. Cloud based collaboration tools (work from anywhere) and e-commerce are just some examples of what we expect is now understood to be very visible long term trends of digital and data.

These trends aren’t new, it’s just that COVID has accelerated them to warp speed; digital enables you to pivot to cope with whatever comes next and data provides the knowledge of how to make the most of it. Datacentres and connectivity are the nexus of that theme. Investors have scrambled to position portfolios for this shift and it seems that you just can’t have enough datacentres in your portfolio in a pandemic (or in the aftermath of one). Our view is that we are early in the digital transformation of global economies and that NXT retains a long runway of growth.

To keep this simple (and brief) we will just look at the growth potential in existing developments in NXT’s 2 main markets of Melbourne and Sydney.

- Melbourne – M1 is full, M2 is undergoing expansion and land has been identified for M3.

- Sydney – S1 is full, S2 is sold out and being built out, S3 is in construction and we estimate availability in late F22/early F23

Just focusing on building out this asset position in these two markets, we estimate that NXT could deploy another 65MW in Melbourne and 70MW in Sydney by the end of F25 (and even then M3 and S3 won’t be fully built out). Over that time, we think NXT deploys a whopping $2.7 billion in capex on land, buildings and fit-out infrastructure….Australia’s datacentre (mini) monster.

Post the recent capital raise NXT has now got the balance sheet to fund this level of investment. And that changes the game, as the market can now look forward with confidence to the growth this investment brings. But what could this look like?

Big numbers. NXT now has the option of re-levering that reset balance sheet, and by F25 it could look a bit like this: net debt of circa $1.8 billion, against a hard asset base of $3.9 billion, net debt to EBITDA in the 4.5-5.0x zone. EBITDA growing like a train along the way to $400 million or so but with assets built that could deliver more than double that, providing a decent growth runway ahead as these facilities mature into a full utilisation in the years beyond. Big dollars.

What does valuation tell us – $13

A lot has happened in the last 11 months, and so we update the inputs into our model for the capital raise, and news flow from its recent F20 results release. These include:

- Higher share count and $860 million more equity capital from the equity raise;

- Revised assumption for peak debt carry – now $1.8 billion, made possible by the extra equity;

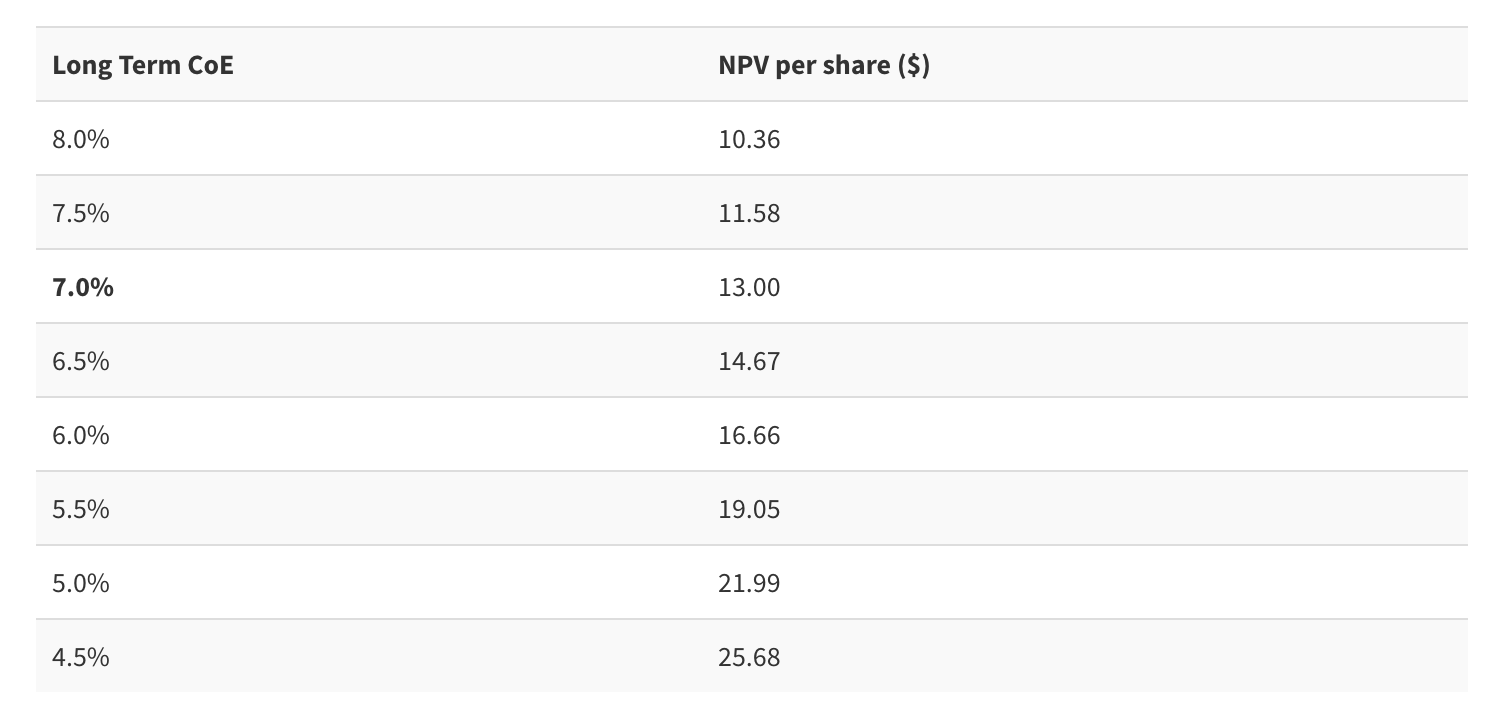

- Balance sheet reset also re-calibrates the risks, we now have more certainty of how and when NXT can fund its portfolio of growth options, and the duration of period of investment up to the point where NXT could start to pay dividends from this asset pool. Previously we applied a cost of equity to that period of 12 per cent, reflecting higher risk and uncertainty. We have now lowered that to 9 per cent. Our long term steady state cost of equity assumption of 7 per cent is unchanged – more on NXT’s sensitivity to long term cost of capital assumptions later;

- Operationally we have lifted capacity at M2 from 40 to 60MW – M2 is NXT’s lowest unit capital cost development site (and all other things being equal best bang for buck in terms of returns); and

- We have made no material change to our pricing or cost structure assumptions.

After all that the model spits out $13 per share valuation.

So what are you playing for now?

At $11.50 it appears to us the easy money has been made, albeit it with some upside remaining. It’s not the potential doubler we identified back in October. However, as we see it there are two value driver catalysts that may lift that $13 view of value;

- Our model captures value up to and including S3 and M3, but not for developments beyond this. The structural forces powering demand for NXT’s services are long term and growing strongly. Investors are likely going to take the view that there is growth beyond the “series 3” assets, and that this option should have some value imputed into NXT’s equity price; and

- Falling cost of equity. We see NXT as digital infrastructure, and the investor base that are the long term owners of that type of asset class tend to apply or bring a low cost of equity, lower than the 7 per cent long term cost of equity we have used in our valuation framework. We think NXT’s long term cashflows will be valued REIT-like when the growth story part of its lifecycle is over (whenever that is). And NXT’s equity valuation is very sensitive to that long-term cost of equity assumption as shown in the table below.

NXT should enjoy a strong period of growth in the near term, of all the growth names we look at NXT is one of the highest quality, from its structural drivers, through to management execution and business model – NXT ticks a lot of boxes. However, we are driven by our view of fundamentals and value on offer for the risk accepted and its clear to us that the easy money has been made. Consequently, our position size in NXT is now a lot lower as we move our capital on to find the next one.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Gary is the Portfolio Manager of the Montgomery Small Companies Fund – a small-cap Australian equity fund investing in 30 to 50 high quality, undervalued small and emerging companies with strong growth potential. The fund invests outside the ASX100.

2 topics

1 stock mentioned

Gary is the Portfolio Manager of the Montgomery Small Companies Fund – a small-cap Australian equity fund investing in 30 to 50 high quality, undervalued small and emerging companies with strong growth potential. The fund invests outside the ASX100.

Expertise

Gary is the Portfolio Manager of the Montgomery Small Companies Fund – a small-cap Australian equity fund investing in 30 to 50 high quality, undervalued small and emerging companies with strong growth potential. The fund invests outside the ASX100.

Expertise

Comments

Comments

Sign In or Join Free to comment