How to assess this viable fixed-income investment

.png)

Omar Khan

Freehold Investment Management

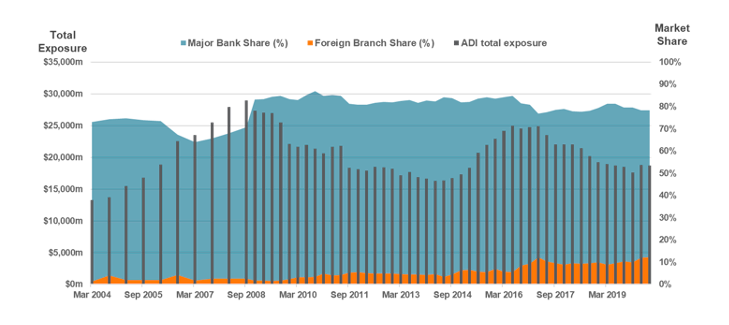

The latest APRA statistics for lending by Authorised Deposit-taking Institutions have recently been released for the June quarter. A noticeable trend is the declining commitment by the banks and mutuals to the residential development sector and the increasing market share of foreign banks and anecdotally, non-bank lenders.

Whilst Australian banks continue their well-documented pullback from the sector, the significant growth in lending from non-banks or fund managers to this sector is helping to meet the demand and fill the lending gap.

We reasonably estimate the total funds under management of the bigger non-bank lenders in residential development finance to be around $11 billion (1) as at 30 June 2020, although estimating the size of the non-bank sector remains difficult given data is not collected by APRA or ASIC. This suggests the non-banks have carved out a market share of about 38% over the last decade.

The investment benefits of real estate debt

With total lending to the residential development sector currently at over $29 billion, what are the benefits to investors? Why should it form part of the income strategy for investors?

Over the last 10 years, a significant amount of capital has been invested in direct real estate to derive income, at tightening yields, the opportunity for capital appreciation, plus the perceived security or stability in the underlying asset value.

For similar reasons, real estate debt is an attractive segment within the private debt market. Notably, these investments offer investors superior risk-adjusted returns or regular income with capital secured by the underlying asset. Of course, real estate debt is particularly attractive in the current market where ‘traditional’ fixed income assets are delivering minimal net returns. For example, a conservatively managed fund is delivering monthly net returns of 7 - 8% per annum.

The growing interest in private debt is illustrated by more and more family offices, high-net worth investors and recently, retail investors via LITs, allocating to the sector. Earlier this year, Chris Cuffe announced that 27% of the Australian Philanthropic Services Foundation, a $110 million public ancillary fund he manages, is allocated to private debt and, the investment has been a major contributor to performance during the COVID-19 period.

Considerations when investing in real estate debt

As with all asset allocation and investment decisions, there are key considerations when investing in real estate debt. How the investment fits in clients’ portfolios, what percentage of the fixed income allocation should be invested in this income-generating asset, and the risks of this type of investment.

Maarten van der Spek (2) has written extensively on private assets and real estate. In his 2017 paper in the Journal of Accounting, Finance and Business Studies, he contends that senior secured debt is most akin to fixed income given investors receive a fixed or floating return that has no, or very little, correlation with investment outcomes for the underlying real estate or the equity component.

Some key points that advisors should consider when looking at real estate deals or funds for their clients are discussed below. Beyond these considerations, it is equally important to look at the depth of experience of the team managing the fund and their expertise in real estate.

1. Leverage Ratios

For most investors, it is easy to focus on the peak leverage ratio (LVR). Loans based on conservative LVRs – generally, LVRs of less than 65% for construction loans with pre-sales - provide greater security for investors and, the returns investors receive, bear very little correlation to the end value of the underlying real estate or security.

Let’s consider an example.

Using the assumptions below, we’ve modelled a scenario illustrating the impact on investment outcomes for debt holders based on a reduction in the asset value at completion (row) and pre-sale defaults (column).

Assumptions:

- A construction loan with an end asset value of $100 million

- Loan size: $65 million (65% peak LVR)

- Gross interest: 11.75% p.a. (interest capitalised)

- Pre-sales: 45% of total borrowed capital (including interest where capitalised)

- Term: 18 months, with delays resulting in a 24-month term

- Penalty interest: 3% p.a. (payable after the initial 18-month term)

The results show there’s minimal impact on the return until the end value drops by at least 40% and, there is no principal loss until values drop by more than 45%.

2. The construction contract and overruns

There is no capital appreciation in debt investment. This means investors’ focus must be entirely on downside protection. So, it’s important to undertake proper due diligence to ensure the right contractual structure is in place, and financial due diligence on the counterparties – the asset being developed, the developer, and the builder.

The construction contract should be a fixed price contract, meaning the builder should absorb cost overruns due to labour, building material increases or weather delays. A good builder will generally have locked in as many of their costs as they can with their suppliers and sub-contractors at the time of signing.

Even though a fixed-price contract may be in place, it is possible that construction costs could still increase. The two main reasons are unexpected complications in groundworks and variations in build specifications at the request of the developer. Irrespective of the reason for cost increases, any increase in build costs that are outside of the fixed-price contract are the responsibility of the developer.

An experienced lender will require the developer to fund out of scope cost increases at the time they are identified, generally by increasing its equity contribution and before any additional construction facility drawdowns can occur.

While it is difficult for advisers to check some of these risks, a Q&A with the fund manager should uncover their approach on the underlying structure.

3. Protecting against builder insolvency

The most significant risk in any residential construction project financing is builder solvency. It is very difficult and expensive to replace builders part way through a project.

There should generally be a multipartite deed in place between the financier, borrower, and builder, and in some instances, the builder’s subcontractors. Such a deed has several functions, including:

- Ensuring that construction assets, once they are fixed to the site, become the security of the lender, and

- The senior lender can quickly take control of the asset if there is a serious default.

An independent Quantity Surveyor should also be appointed by the lender. They provide an independent due diligence assessment of the project, drawdown and cost to complete reports, ensuring that sufficient funds are always available to complete the project and that additional drawdown only occur when the relevant conditions are met.

4. Quality of development partner

If you only compare loans based on Internal Rates of Return (IRR) and LVRs, it’s likely you’ll risk missing some key assumptions that go to supporting the security of the loan.

The strength of both the development partner and the building partner is particularly important for construction loans. Strong development partners demonstrate a solid track record of success, have strong balance sheets and, are leaders in their areas of specialty. While pre-sales do provide significant protection, clarity on exit mechanisms and strong protection against real estate price falls, they can only be enforced when a project completes.

Conclusion

- Real estate debt continues to offer attractive risk-adjusted returns for yield investors.

- There are now a number of options available for investors to gain exposure to this asset class.

- Deals or portfolios with conservative LVRs can sustain a significant reduction in end values before there is a principal loss for investors.

- It is difficult for investors or advisors to undertake due diligence on the underlying contractual arrangements in a deal, or counterparties. This is also where most of the risk sits for investors.

- Investors or advisors should get comfortable with a manager’s approach and are likely to be better served with a diversified open-ended vehicle rather than a deal by deal or syndicate investment structure.

Focus on capital preservation and income

The Freehold Debt Income Fund* aims to deliver regular income from a diversified, and conservative, portfolio of debt secured by real estate. The fund targets an annualised net return to investors of between 7 - 8%. Click the contact button below for more information.

*The Fund is only open to wholesale or sophisticated investors.

Footnotes

- In our analysis, only groups that originate deals are counted, which removes the impact of double counting.

- Maarten VDS., ‘Investing in Real Estate Debt: Is it Real Estate or Fixed Income?’ ABACUS, Vol. 53, No.3, 2017

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Omar has over 15 years' experience across funds management and real estate. His experience extends across structuring, due diligence, capital raising, as well as managing and growing funds management businesses.

.png)

1 topic

Omar Khan

Executive Director and Portfolio Manager

Freehold Investment Management

Omar has over 15 years' experience across funds management and real estate. His experience extends across structuring, due diligence, capital raising, as well as managing and growing funds management businesses.

Expertise

Omar Khan

Executive Director and Portfolio Manager

Freehold Investment Management

Omar has over 15 years' experience across funds management and real estate. His experience extends across structuring, due diligence, capital raising, as well as managing and growing funds management businesses.

Expertise

Comments

Comments

Sign In or Join Free to comment