How to fix Financial Services

It ain’t over yet. Round 6 of the Financial Services Royal Commission, set for September, is going to focus on insurance. An investment in the Forager Australian Shares Fund, Freedom Insurance (FIG), has been called to appear. The revelations are likely to be ugly.

But we don’t need round 6 to tell us something needs to change. We have already seen enough—this is an industry rife with conflicts of interest and woeful consumer outcomes.

The question now is how to fix it? As the year draws to an end, that’s the question to which Commissioner Kenneth Hayne will be turning his mind. And it’s one I haven’t seen many sensible answers to.

There are two key problems from where I sit.

Why aren’t people in jail?

Firstly, why haven’t these companies and the people behind them been punished for breaking the law?

I attended a compliance course recently that went right back to basics. As an AFSL holder, your obligations are pretty clear. This is Part 1 of Section 912A of the Corporations Act:

(1) A financial services licensee must:

(a) do all things necessary to ensure that the financial services covered by the licence are provided efficiently, honestly and fairly;

Efficiently, honestly and fairly. How does any of what we have seen meet that criteria? And this is not some regulatory guide or compliance statement. It is the law.

The natural reaction to what we have seen is going to be more regulation and red tape, but I can’t see what is wrong with the law that currently exists. I can tell you from personal experience that smothering the industry in expensive compliance obligations only entrenches the large established participants.

We need stricter penalties. And an ability or willingness to enforce the law. Extreme behaviour needs to be criminal. What is the point of fining the company or their insurers if the executives responsible get to retire with their bonuses?

The default needs to change

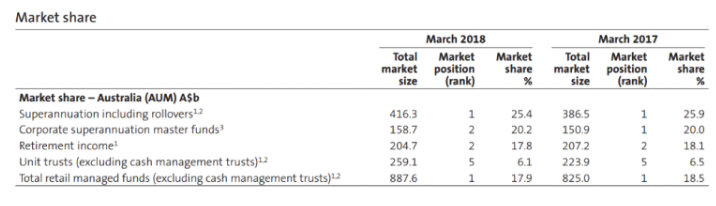

The second big issue is that the customers of these financial institutions are letting them get away with it. Here is a table from AMP’s half year results showing their market share in various parts of our asset management industry:

AMP’s market share in retail superannuation fell 0.4 of one percent on a year ago. You couldn’t script a worse quarter of public relations, and the company loses less than half a percent of market share. In fact, if you go into the details, the company matched its outflows with inflows.

It is tempting to think that people don’t care. There is certainly a part of the population — frustratingly for me — that see their super as too far into the future and don’t give it any attention. But the public outrage to the Royal Commission suggests the problem is far more nuanced than that. A lot of people do care. But they still don’t do anything about it.

One reason is that what to do with your savings is a big and difficult decision. And the more difficult a decision, the more likely we are to stay with the status quo.

Psychologist Dan Ariely talks about this using organ donation rates as an example. Trying to explain the high level of variability of organ donation rates between similar countries, researchers discovered that the main cause of difference was whether people were asked to opt in or opt out:

“It turns out that it is the design of the form … In countries where the form is set as “opt-in” (check this box if you want to participate in the organ donation program) people do not check the box and as a consequence they do not become a part of the program. In countries where the form is set as “opt-out” (check this box if you don’t want to participate in the organ donation program) people also do not check the box and are automatically enrolled in the program. In both cases large proportions of people simply adopt the default option.

You might think that people do this because they don’t care. That the decision about donating their organs is so trivial that they can’t be bothered to lift up the pencil and check the box. But in fact the opposite is true. This is a hard emotional decision about what will happen to our bodies after we die and what effect it will have on our those close to us. It is because of the difficulty and the emotionality of these decisions that they just don’t know what to do so they adopt the default option (by the way this also happens to physicians making medical decisions, and also to people making investment and retirement decisions).”

Sound familiar? Faced with a complicated decision, people choose the default. And that is something Australia’s financial institutions have made billions of dollars out of.

If I were to make one change to the system it would be to make the default choice one that is good for consumers. If you want to do some research, tick a box and go with a different option, that is completely up to you. And if you lose your money or get bad advice, then tough. Most of this cohort are pretty good at looking after themselves.

But if you do nothing, it should not be possible for you to end up with AMP. I know MySuper is a step in this direction. But I would take a significant step further. Australia has a well run sovereign wealth fund, the Future Fund. Why not make it the default manager for Australians’ superannuation?

Beware the unintended consequences

Sadly, I can’t say much of what I have heard at the Royal Commission has surprised me. I have worked in the industry for 20 years and built a business on the back of the small percentage of the population who worked out what was going on long ago. But that’s precisely why this Royal Commission needed to happen. Much of the behaviour had become culturally ingrained. And it wasn’t going to change without a public inquisition.

But now we enter the risky phase. History is littered with unintended consequences of well meaning responses to public outrage. Getting the response right is going to be the most difficult step.

Find out more

If you are interested in receiving the Forager monthly and quarterly reports, please register here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Steve began Forager Funds in 2009, and now manages approximately $470m across two funds. The Forager Australian Shares Fund and Forager International Shares Fund are both unlisted and are available to investors with daily applications and redemptions. Steve focuses on long-term investing in undervalued, underappreciated and sometimes unloved companies.

.jpg)

1 stock mentioned

.jpg)

Steve began Forager Funds in 2009, and now manages approximately $470m across two funds. The Forager Australian Shares Fund and Forager International Shares Fund are both unlisted and are available to investors with daily applications and...

Expertise

Steve began Forager Funds in 2009, and now manages approximately $470m across two funds. The Forager Australian Shares Fund and Forager International Shares Fund are both unlisted and are available to investors with daily applications and...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions

Equities

Morgans’ top large-cap picks for October 2025

Morgans Financial