I tried to warn them about the coming liquidity crisis...

On 28 February I wrote to the Reserve Bank of Australia, the prime minister, and the treasurer warning that “it is clear both equity and bond markets are starting to fail: the problem is extreme information asymmetries”. At that point the US equity market had slumped only 13 per cent. (You can also click here to read the column.)

“Markets have never had to properly price a real global pandemic, which is an almost impossible task, and they are basically shutting down,” I continued. “Unlike the trade wars, Brexit, or Grexit, you are not handicapping human probabilities. This is about pricing the spread of a deadly global virus that is completely new and has no vaccine or drug mitigants as yet.”

“The information asymmetries are being exacerbated by the containment policies, which are shutting down parts of the global economy. One might rationally let the virus spread and just seek to mitigate. But by shutting down globalisation, the economic effects are going to be much, much worse.”

“In the medium term we are all fine. We get a vaccine, anti-viral drugs, and go through summer. But in the next three months, I think governments are going to have to act to keep markets functioning through temporary liquidity bridges coupled with extra stimulus.”

The RBA was listening, but I was worried policymakers were underestimating the gravity of the crisis. That anxiety has certainly been vindicated by the comedic series of all-too-human mis-steps from the US Federal Reserve, European Central Bank, US Treasury and US President Donald Trump.

On 29 February I wrote to the RBA and government, expanding on these warnings: “We are currently experiencing a global liquidity crisis across both equity and bond markets, which will get much worse in the days/weeks ahead as global economic activity declines dramatically”.

“The global liquidity crisis is being driven by the inherent difficulty private markets have pricing and predicting the future financial paths associated with the emergence of a deadly pandemic. The information asymmetries are enormous, and as we saw during the GFC, this leads inevitably to limited-to-no liquidity or outright market failure.”

“Market participants have seen these liquidity crises before, and know that they very rapidly shift to solvency crises via negative feedback loops amplified by the sharp simultaneous retrenchment in global economic activity. Unlike previous shocks, such as 1987, 1991, 1998, 2001, 2007-09, 2011-12, 2015-16, and 2018, there is no natural human circuit breaker. This is not about excess leverage, overvalued assets, poor credit decisions, the collapse of the EU, trade wars or military conflict between nation states.”

“This is about the impact of a deadly global virus. It is a virus markets have never seen before, and carries with it a range of horrific known unknowns and unknown unknowns. The negative financial accelerator—and the negative feedback loops between financial markets and economic activity—are now well and truly in full flight. Time is, as a result, absolutely of the essence. The longer decision-makers wait, the greater the economic damage is going to be.”

“Policy is the only thing that can cauterise the rapidly accelerating liquidity/solvency crisis. It is imperative that global synchronised monetary policy immediately offers to vouchsafe liquidity and funding to all parts of the financial system."

If I made one key mistake, it was assuming that policymakers would immediately embrace these demonstrably obvious solutions. Instead, we had the Fed telling the market that rate cuts could not fix broken supply chains and that it was not considering quantitative easing (QE). Cue an immediate 3.5 per cent drop in US shares after they had rallied more than 5 per cent before the Fed’s 50 basis point emergency cut. (The demand-side aspects of this crisis, which policy can address, are orders of magnitude worse than the short-term supply-side interruptions, which will rapidly disappear.)

Next we had statements from the G7 and G20 that they would use all available tools to combat the virus, but this rhetoric was not matched with any tangible action. Concurrently, President Trump was trying to reject the Democrat’s proposal for US$8.3 billion of emergency funding to fight the virus, bizarrely arguing for a fraction of this sum.

We also astonishingly had no action at all from either the Bank of England or the ECB.

On 7 March I wrote to the RBA and the government again: “With central banks failing to provide any liquidity (as opposed to interest rate) support to markets that were demonstrably starting to fail over a week ago, we are seeing—as I warned—the clear emergence of a very serious liquidity crisis, which will rapidly transform into a sovereign, banking and corporate credit crisis worse than the GFC unless policymakers take rapid mitigating actions.”

“While most central banks are running out of traditional monetary policy ammo, they have an almost unlimited ability to provide massive liquidity support, which will be immensely impactful in unlocking the paralysis in global markets. This cannot be just government bond QE—it needs to be full-spectrum, unrestricted QE across all sectors, including governments, banks and corporates on a temporary basis until the virus-induced air-pocket in liquidity has passed.”

“This is precisely why we established central banks in the first place: to serve as lenders of last resort to critical funding markets when they face crises precipitated by exogenous liquidity as opposed to solvency shocks.”

This week the Bank of England belatedly stepped up and delivered a 50 basis point cut combined with more than GBP100 billion of near-free 4 year funding for UK banks, protecting them from the soaring costs in their bond markets. Concurrently, the ECB president, Christine Lagarde, signalled she was about to shock and awe. Instead, the ECB offered the absolute bare minimum markets expected, which was no rate cut, a modest EUR10 billion monthly increase in its existing QE program (with no changes to the limits on what sovereign and corporate bonds it can buy). The ECB also offered to provide virtually unlimited long-term funding to European banks at a negative 0.25 per cent interest rate.

What the market wanted was a “Draghi moment”. In mid 2012 the former ECB chief cauterised the extreme volatility wrought by the European sovereign bond crisis by declaring the ECB would do “whatever it takes” to save the Eurozone.

Lagarde betrayed her extreme naivete by doing the exact opposite, stupidly stating that “we are not here to close spreads, this is not the function or the mission of the ECB.” By spreads, she means borrowing costs for governments, banks and companies. And that is exactly the role of all central banks: to control borrowing rates!

Spreads on once safe government bonds across Europe sky-rocketed. A trader this morning told me he tried to sell ultra-safe German government “bunds” and could not find a bid. As predicted, liquidity had evaporated.

Only days ago the Fed chair scared the hell out of markets by saying QE was not coming. Overnight markets forced him to unleash massive QE with the New York Fed injecting US$1 trillion into short-term money markets and embarking on massive purchases of longer-term US government bonds. Why? Because liquidity in the supposedly the safest asset on earth, US treasuries, had vaporised. This was total market failure, as I warned the RBA weeks ago.

The extreme instability intensifying across global financial systems was amplified 24 hours earlier by President Trump’s bumbling attempt at addressing his nation via an emergency, 9pm telecast. For weeks the market had been begging the world’s largest economy to provide a clear fiscal policy response to the coronavirus. What did Trump offer? Absolutely nothing other than inexplicable misstatements from a frail old man who looked like he had caught the disease himself.

But markets will have their way: the US has no choice but to quickly pull together a cohesive, circa US$100 billion to $200 billion stimulus package that is the pro-rata equivalent of what prime minister Scott Morrison and Treasurer Josh Frydenberg have sensibly constructed.

Even the RBA has appeared asleep at the wheel, telling this newspaper only days ago that the current crisis was nothing like the GFC and that “the liquidity environment in bond markets and markets more generally is different than it was 10 to 12 twelve years ago now.” The only correct part of that assessment is it is now possibly worse.

There have been other knock-on consequences. For a year this column has warned investors that the wave of high yield (aka junk) bond funds offered on the ASX via listed investment trusts (LITs) would trade at steep discounts to their net tangible assets (NTAs) in any stress event. I was relentlessly shouted down by the vested interests. The sector has since been smashed with the most recent issue from KKR (ASX: KKC), a $925 million LIT that listed for $2.50 in November, trading down to $1.65 on Friday, or a 35 per cent discount to NTA.

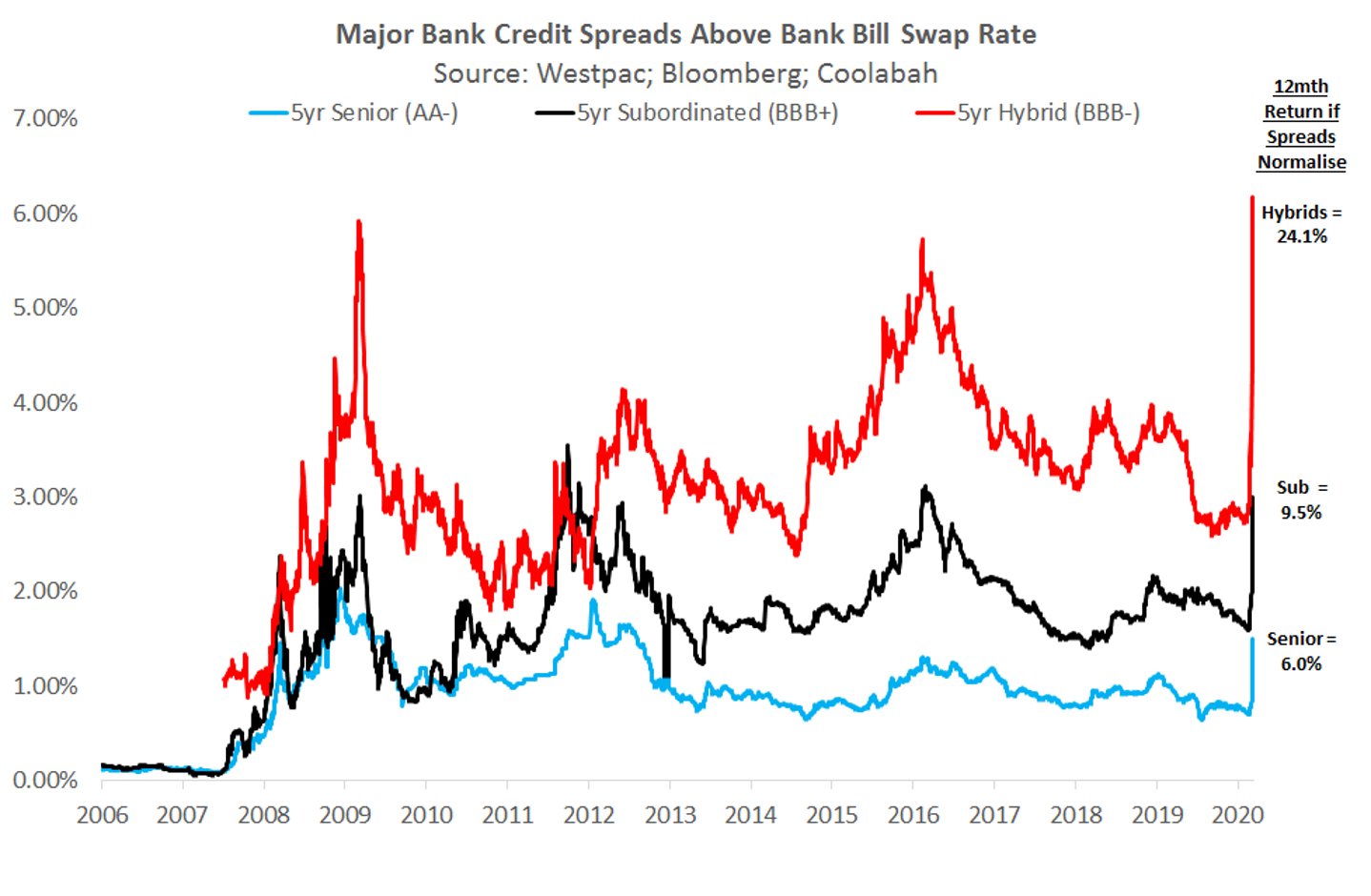

At the same time, we have seen NAB and Macquarie very generously return almost $1 billion in cash to investors who were going to subscribe for their latest hybrid offers while still repaying their existing NABPC and MBLPA securities, which will return another circa $1.8 billion of cash to holders.

They did so because they recognised that the hybrid spreads on the ASX right now, which have jumped from 2.7 per cent to 6.27 per cent above bank bills, are as high as those recorded during the GFC. They make the recent NAB and Macquarie hybrid spreads look awfully low, and the banks did the right thing by investors by not taking this cheap money.

When all is said and done, markets will get what they want through signalling what is and is not acceptable. Order will eventually be restored. And this crisis will pass, probably within one or two months. Those that survive will face the investment opportunity of a life-time.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

Disclaimer: This information has been prepared by Smarter Money Investments Pty Ltd. It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Past performance is not an indicator of nor assures any future returns or risks. Smarter Money Investments Pty Limited (ACN 153 555 867) is authorised representative #000414337 of Coolabah Capital Institutional Investments Pty Ltd, which holds Australian Financial Services Licence No. 482238 and authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271.

1 topic

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment