TOL - 1st Dec, 2020

Investing in a vaccinated world

The endless vaccine speculation of 2020 has crystallized into a single reality: coronavirus vaccines will be rolled out around the world over the coming 3-6 months. They are safe and effective.

Moderna, Pfizer and Astrazeneca have all succeeded, and the Russians and Chinese seem to believe they have vaccines as well. This has immense consequences for global spending patterns, and there is still time to get ahead of it.

In March, people suddenly stopped eating out and travelling. As it turns out, we actually spend quite a bit on those things.

Most people kept their jobs (one of the harshest things about this crisis is that it hit so unevenly), and the excess spending power went to other areas, notably online retail. When people start taking those long-delayed trips to visit friends and family, that spending power will necessarily come from somewhere else.

We're using four principles to guide our decision-making:

1) Our portfolio will always consist of winners.* No theories, opinions, or speculations - every company must be firing on all cylinders. Earlier in the year, we decided to shift entirely to companies accelerating through the coronavirus, which led us straight to digital health, digital payments and e-commerce. That was more successful than we could have hoped. We will use the same philosophy over the coming months and indeed decades.

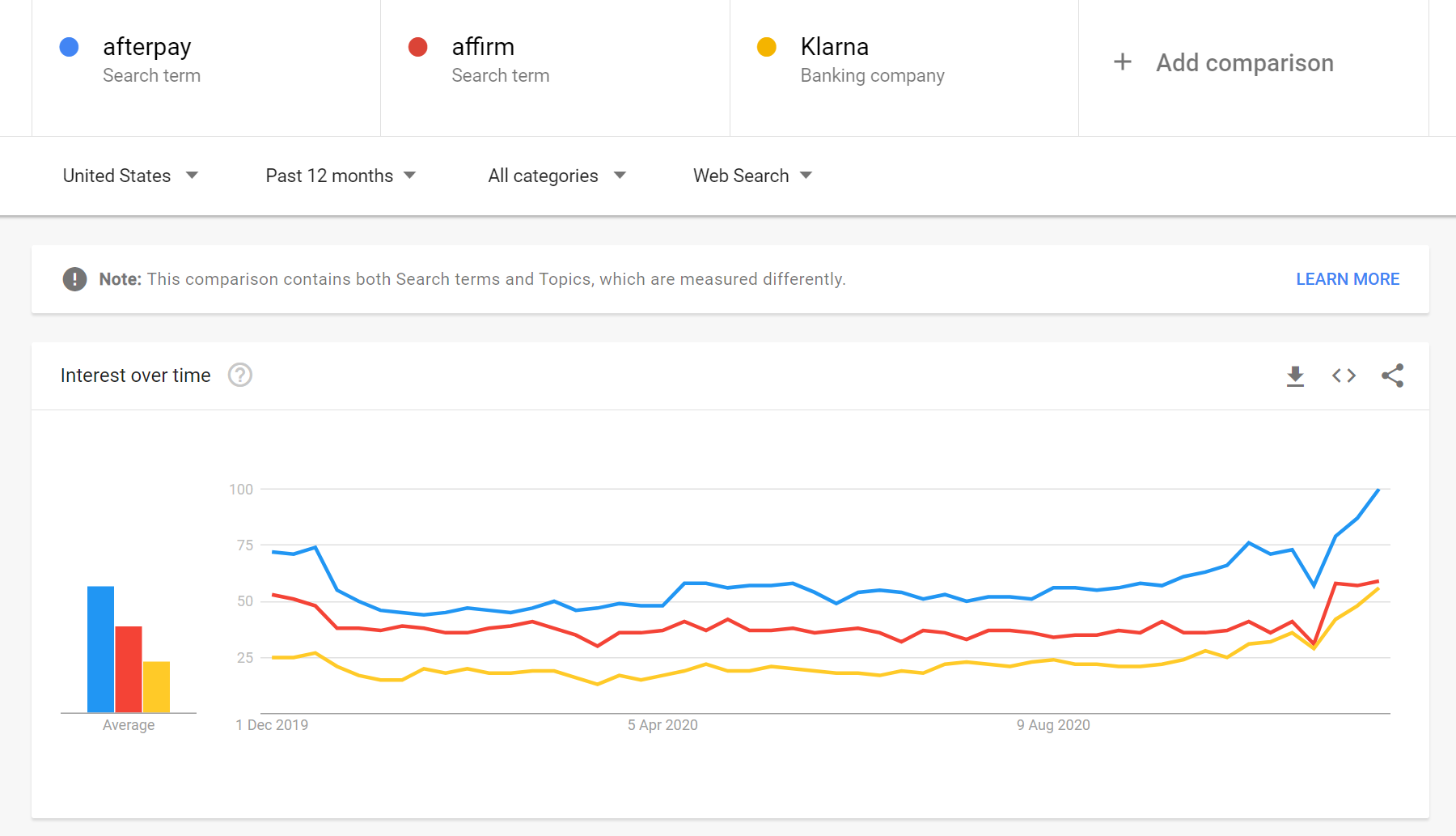

To preempt the question, Afterpay is a modest position but we generally view growth profiles like this as buys, not sells:

2) As readers will know, we have been trading out of 40x sales software and other high multiple businesses for some time now, and reallocating to companies on 1/10th of the multiple, which in many cases are growing faster anyway. We haven't had to wait long for this to work.

We are also trying to avoid forming opinions on questions like, how much of the growth in e-commerce is here to stay, and how much was just a product of the epidemic? We will reserve judgement until the evidence comes in.

Companies like Shopify, Datadog, et al will all do fine, but they have multiple compression in their future, rather than the expansion that made them some of the top performing investments on the planet. The best returns come from multiple expansion on multipled revenues. You are simply not going to get that from something trading at 40x sales, and the world in which you do is a scary one!

Furthermore, we think interest rates might rise and take the wind out of the growth complex, and this has already happened to some degree.

It's a good time to stay away from the crowd.

3) We've been working hard over the past few months to identify companies that will benefit from a recovery. That seemed odd and premature in August and September, but is now serving us well, as many high-flying tech names are well off their highs and tech indices have stagnated.

I'm somewhat reluctant to mention names, but on the recovery side we've discussed companies like Disney before. The perfect candidate is something that was already growing fast through coronavirus, but has a strong recovery element too. Disney certainly fits, with their consumer business exploding upwards and the profit from their parks soon to reappear on their financial statements. Maybe Square does as well, I don't think that's too controversial.

Healthcare stocks focused on non-coronavirus sectors which have had a tough time in 2020 are also likely to benefit.

4) The life sciences opportunity set is better than ever and a core focus. After the last six months, these firms can be sure of significant investor attention, so best-in-class, fast-growing companies will not be short of a bid.

The next best thing to a fast-growing company accelerating in a vaccinated world is one that has nothing to do with coronavirus or the broader economic cycle - which is true of most of the sector.

We have identified a handful of companies which we expect to 5-10x revenues, and are focusing largely on these. Examples include Ultragenyx:

And Shockwave:

(Note - we bought these at significantly lower levels so don't rush in).

The advantage of these is that they are largely immune to the tech/growth rotations that have convulsed markets over the past month or so and will probably continue to do so. The cure to high multiples is not always a crash, it can also be years of sideways price action with significant volatility that nobody wants to be a part of.

Despite this period of activity, the bulk of our portfolio remains largely unchanged, and we are working to maintain an average weighted organic growth rate across the portfolio of comfortably over 75%, across over 35 positions.

Learn more

Stay up to date with all our latest Livewire insights by clicking the follow button below, or visit our website for more information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael manages a global equity investment fund focused on technology and the life sciences. Michael completed undergraduate and graduate chemistry degrees at Magdalen College, Oxford University, and studied finance at the London School of Economics

........

The information in this note has been prepared and issued by Frazis Capital Partners Pty Ltd ABN 16 625 521 986 as a corporate authorised representative (CAR No. 1263393) of Frazis Capital Management Pty Ltd ABN 91 638 965 910 AFSL 521445. The Frazis Fund is open to wholesale investors only, as defined in the Corporations Act 2001 (Cth). The Company is not authorised to provide financial product advice to retail clients and information provided does not constitute financial product advice to retail clients.

The information provided is for general information purposes only, and does not take into account the personal circumstances or needs of investors. The Company and its directors or employees or associates will use their endeavours to ensure that the information is accurate as at the time of its publication. Notwithstanding this, the Company excludes any representation or warranty as to the accuracy, reliability, or completeness of the information contained on the company website and published documents.

The past results of the Company’s investment strategy do not necessarily guarantee the future performance or profitability of any investment strategies devised or suggested by the Company.

The Company, and its directors or employees or associates, do not guarantee the performance of any financial product or investment decision made in reliance of any material in this document. The Company does not accept any loss or liability which may be suffered by a reader of this document.

1 stock mentioned

Michael manages a global equity investment fund focused on technology and the life sciences. Michael completed undergraduate and graduate chemistry degrees at Magdalen College, Oxford University, and studied finance at the London School of Economics

Michael manages a global equity investment fund focused on technology and the life sciences. Michael completed undergraduate and graduate chemistry degrees at Magdalen College, Oxford University, and studied finance at the London School of Economics

Comments

Comments

Sign In or Join Free to comment