Is active management complementary in a concentrated market?

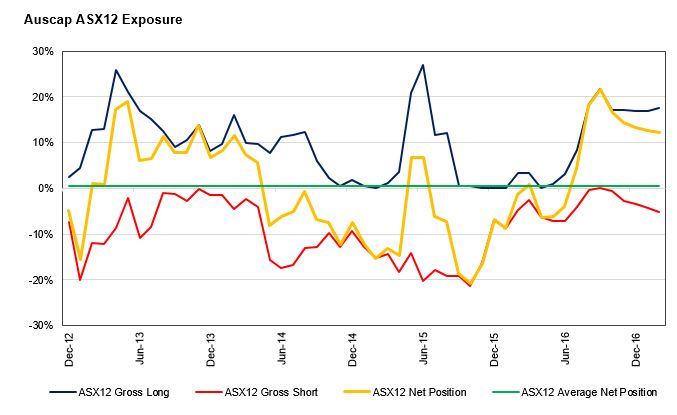

The Australian sharemarket is a highly concentrated one. As outlined in the Auscap November 2015 newsletter, just twelve stocks constitute approximately half of the market capitalisation of the ASX200 (Index). In fact, as at the time of publication, these stocks represent 48.7% of the Index, with a combined market capitalisation that is almost the same as the next 188 companies that make up Australia’s most recognised index. When we consider an investment opportunity, a company’s proportion of any index plays no part in our decision. We are a completely index unaware fund. We recently analysed the Fund’s historical exposure to the twelve largest ASX listed securities, which comprise Commonwealth Bank of Australia, Westpac Banking Corporation, Australia and New Zealand Banking Group, National Australia Bank, BHP Billiton, CSL, Telstra, Wesfarmers, Woolworths, Macquarie Group, Woodside Petroleum and Rio Tinto (hereafter the ASX12).

Since its inception in 2012, the Fund has averaged only 0.5% net exposure to the ASX12. That is an average of practically zero net exposure to half of the ASX200 Index. It might lead an observer to ask a number of questions. Firstly, does that mean that our performance will look very little like the Index’s performance? And secondly, given the importance of the top twelve securities to the overall performance of the market, should we be making decisions with the size of companies relative to the Index in mind?

The answer to the first question, whether our performance will deviate frequently from the performance of the broader indices, is a most definitive yes. Much of the time our performance has not mirrored or even resembled the performance of the major indices given we have had, on average, no material exposure to half of the Australian market by “index weight”. Further, we are a long short fund, which means that not only do we not share the major exposures of the market, sometimes we may be net short a particular sector. Our performance over time will be determined far more by our ability to select stocks that have compelling reward and risk metrics than it will be a function of what happens to the broader stockmarket. This is borne out in Auscap’s low correlation with markets, which is running at 52.3% against the All Ordinaries Accumulation Index since the Fund’s inception.

Our answer to the second question, whether index weight should be a major determinant in our investment making decision, is for us a most definitive no. The fact that a company has a very large market capitalisation, in and of itself, tells us very little about whether the company is a compelling investment proposition. The Auscap portfolio’s investments are sized by investment merit, old fashioned value based investing and an evaluation of risk and reward.

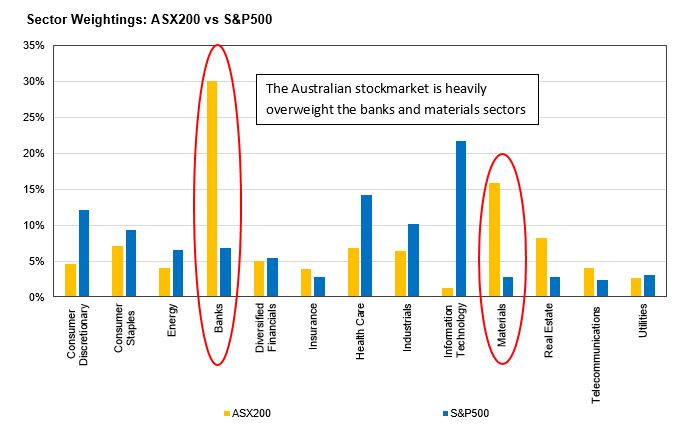

The fact that the Australian equities market is very concentrated in a few sectors actually means that the average domestic investor is considerably overweight the major Australian sectors. Consider, for example, the Australian market’s exposure to various sectors compared to the broader and more representative S&P500 index.

The Australian market is heavily overweight banks and resource companies compared to the S&P500 or most other international indices. Should we naturally lean towards being overweight these sectors simply because they contain some of the largest domestically listed companies? We prefer to evaluate opportunities on a stock specific basis, sticking to our strict investment criteria and disciplined, patient approach to managing our investors’ capital. This will mean regular divergence in the Fund’s performance compared with the domestic indices. Whether actively managed funds have the ability to complement the typical Australian investor’s portfolio is potentially worthy of some consideration, especially if the firm’s investment philosophy, approach and stock selection process appeal to the particular investor.

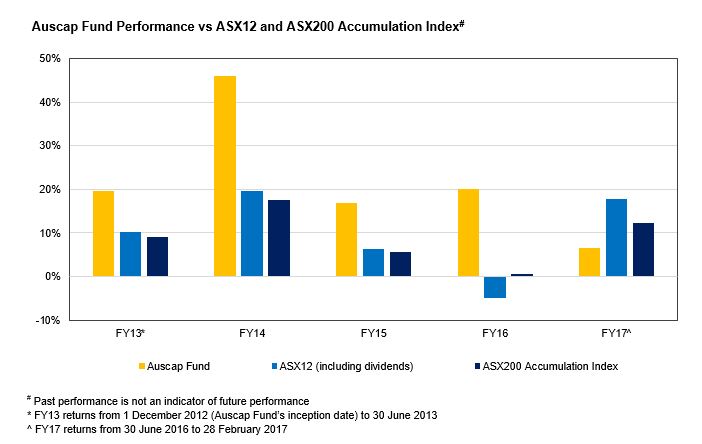

While passive portfolio management is gaining in popularity around the world, in Australia this means having close to a 50% exposure in just twelve stocks without a consideration of the merits of these investments. Many of these securities are already owned in some capacity by the average investor, which might make an investment in a genuine active manager a complementary exposure. As shown below, Auscap outperformed in FY16 when the ASX12 detracted from the market’s overall performance. The converse has been true thus far in FY17, with the biggest companies driving the market’s performance. We continue to see better investment opportunities outside of these mega-cap stocks.

By all means, careful manager evaluation and selection is critical when choosing active managers. Our belief is that investors should search for managers with whom they have a shared investment philosophy as well as those managers who have a demonstrated track record of performance. It is possible for a managed fund’s portfolio to be highly complementary to the average investor’s portfolio. Given most domestic investors’ exposure to the largest twelve Australian listed companies, funds that have lower exposure to these stocks are not adding to already overweight positions. While some funds go to the other end of the spectrum, and are concentrated in small and micro cap stocks, this is not true of the Auscap Fund. Approximately 80% of the Fund’s returns in FY16 came from stocks within the ASX100. Our preference is to invest in large and mid cap securities. These are companies that have the characteristics we are looking for, including: significant cash flow generation; a track record of strong returns on invested capital; sensibly geared balance sheets; simple and proven business models and significant sustainable competitive advantages to ensure continued profitability.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Auscap Asset Management is a value based, active Australian equities investment manager established in 2012. Auscap Asset Management is the Responsible Entity and Investment Manager for the Auscap High Conviction Australian Equities Fund and Auscap Ex-20 Australian Equities Fund. The Funds target solid risk-adjusted returns, looking to invest in companies that generate strong cash flows and are trading at attractive prices.

Auscap Asset Management

Auscap Asset Management is a value based, active Australian equities investment manager established in 2012. Auscap Asset Management is the Responsible Entity and Investment Manager for the Auscap High Conviction Australian Equities Fund and...

Expertise

Auscap Asset Management

Auscap Asset Management is a value based, active Australian equities investment manager established in 2012. Auscap Asset Management is the Responsible Entity and Investment Manager for the Auscap High Conviction Australian Equities Fund and...

Expertise

Comments

Comments

Sign In or Join Free to comment