Is it time to panic?

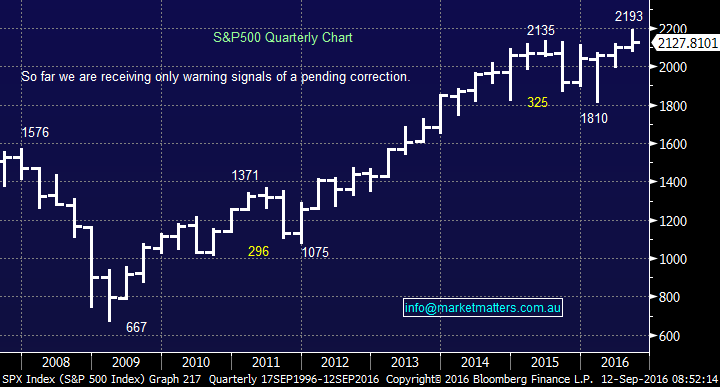

Good morning everybody, on what is likely to be a tough day for local stocks with the futures pointing to at least a 1.5% fall in early trading. Today, we have changed our usual question style report due to the large nature of emails received over the weekend on the same subject, following Friday’s savage decline by US stocks – basically, is it time to be scared? We have to ask ourselves, "is the bull market advance since early 2009 complete for US stocks?" If the answer is yes, then the likelihood is that the S&P500 will correct ~600-points minimum or a whopping 25%. At this stage, as can be seen on the longer-term chart, Friday’s fall is hardly noticeable at this point in time. However, we have to reiterate we can see only a maximum of 10% upside from current levels, compared to at least 25% downside = clearly of concern.

Nicholas Forsyth

Market Matters

US S&P500 Quarterly Chart

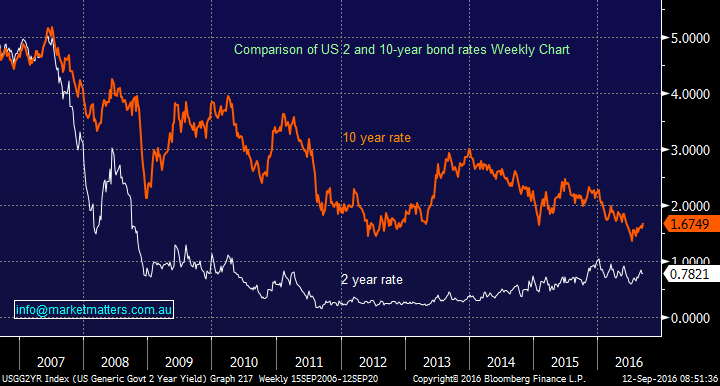

Friday’s decline in equities was not surprisingly, led by the bond market - a looming problem we have been flagging for many weeks. The ECB disappointed markets by not extending quantitative easing last week, lighting the fuse for a pullback in global bonds = higher interest rates. Rumours are now in overdrive around what Japan will do later in the month, as well as the whether the Fed will raise rates in September, December or even both.

As we have covered a number of times recently, investors should be prepared for rising interest rates, increased volatility and higher inflation - exciting times ahead!

The main characteristic of Friday’s shakeout in the bond markets, was the longer-dated interest rates rising faster than at the shorter dated, referred to as a "Bear Steepener". In simple terms, markets are pricing in more inflation and potentially some fiscal stimulus - scenarios we have discussed recently.

If central banks do engineer, this rumoured steepening of the yield curve the likely motivation is to improve the economy by aiding the banks, which in turn will lead to more lending, hence helping the economy to grow.

Comparing US 2-year and 10-year interest rates

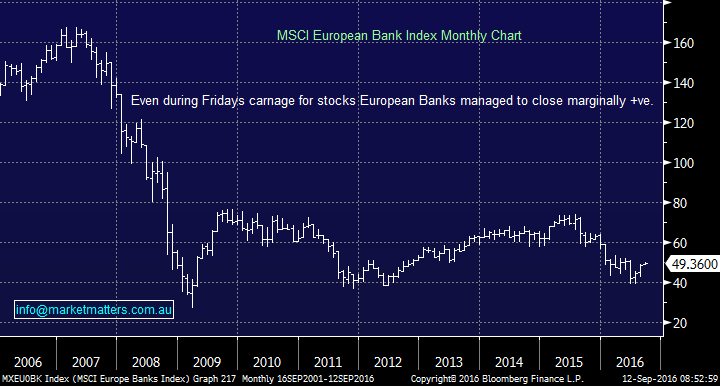

This "steepening" move in the yield curve is good news for banks margins/profitability. On Friday night during the carnage for stocks, European banks impressively managed to close positive, plus they actually closed over their 200-day moving average for the first time in a year. In the US where the sell -off became more aggressive, the banks closed down only 1.2%, around half of the fall across the broader market.

We remain relatively bullish banks at this stage in the cycle and for sophisticated investors "Buy-Writes" in the banks look very attractive into the anticipated weakness today plus increased option volatility.

N.B.: We are relatively positive, but if markets get hammered, they are still likely to fall but by just a smaller degree e.g. US banks on Friday night.

MSCI European Banks Index Monthly Chart

We feel that Friday’s deep correction by US equities owes a large part to the recent history breaking period of sideways movement. Rate rises in the US are likely nothing new and a move to steepen the yield curve should be positive for the banking sector. At this point, we do not see this as a "Black Swan" style news that should send stocks into a tailspin, but major follow through tonight will technically be very concerning.

At this point of writing this morning's report, the US S&P500 futures have opened basically unchanged which is some short-term comfort.

Summary

We are not bearish US stocks at this point, but the risk/reward profile at this point is NOT compelling to aggressively buy the broader market. Unfortunately, the ASX200 does now feel to have peaked at 5611 for 2016. Hence we will be looking for countertrend rallies to lighten our overall equity exposure.

We remain relatively bullish banks and negative quasi-bond style stocks. For sophisticated investors, we like buy/writes in the banks into current weakness and high volatility. We will explain this in more detail in tomorrow morning’s report.

Livewire readers can receive 14 days’ free access to our Platinum level membership by registering here: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Market Matters is an online investment and share trading advisory service designed for those that want to take their wealth further. We specialise in advice for active share market investors, including those new to the markets or those with a Self Managed Super Fund (SMSF). As a member, you will receive twice daily and weekly trading and investment advice focusing primarily on ASX equity investments. Additionally, we share his market positions and provide an ongoing outlook on key stocks and markets that matter. We provide clear share trading and investment buy and sell recommendations with the clear aim of outperforming the market. https://marketmatters.com.au/

3 topics

Nicholas Forsyth

Director

Market Matters

Market Matters is an online investment and share trading advisory service designed for those that want to take their wealth further. We specialise in advice for active share market investors, including those new to the markets or those with a Self...

Expertise

No areas of expertise

Nicholas Forsyth

Director

Market Matters

Market Matters is an online investment and share trading advisory service designed for those that want to take their wealth further. We specialise in advice for active share market investors, including those new to the markets or those with a Self...

Expertise

No areas of expertise

Comments

Comments

Sign In or Join Free to comment