Is it time to sell the bond proxies?

Clime Investment Management

Clime Investment Management

One of the strongest and most predictable relationships in global equity markets over the last few years is that of bond yields and so-called ‘bond proxies’. As the name suggests, a bond proxy is a stock that is held in place of fixed interest securities, primarily for yield. They are typically large and stable with annuity-style cash flows supporting a predictable and reliable dividend stream.

In the Australian market, this category is dominated by REITs and listed infrastructure. Both groups fell sharply in the latter half of 2016 as government bond yields jumped and signs begun to emerge that global interest rates were finally on an upward trajectory.

Infrastructure giants like Transurban (TCL.AX) and Sydney Airports (SYD.AX) have since recovered to reclaim the bloated valuations that characterised the infrastructure sector over the last few years. REITs have not been so fortunate, with bond yields threatening to exert pressure on valuations. The question on many investors’ minds is whether now is the right time to sell the bond proxies or if valuations (and invested capital) can continue to be sustained.

Is it time to sell them?

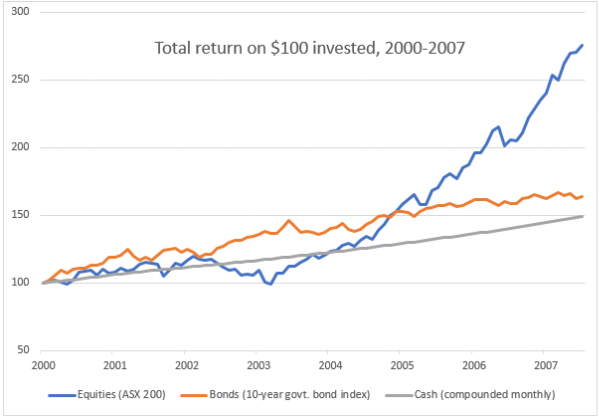

The answer is ultimately and inextricably linked to a view on bond yields both domestically and abroad. The post-GFC decade of investing has been defined by staggering monetary stimulus, ultra-low interest rates and extreme yield compression in the bond market. These are conditions perfectly suited to the cultivation of inflated bond proxy valuations. Consider the illustrative charts below. Pre-GFC, cash was yielding around 5-7%, setting a higher benchmark for yields of bonds and bond proxies alike. Following the financial crisis, that paradigm shifted dramatically.

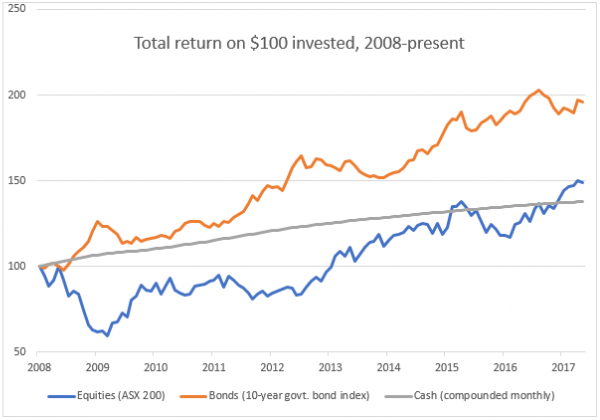

Lower cash rates coupled with extraordinary stimulus measures led to lower interest rates on bonds as investors were prepared to accept lower and lower yields. Suddenly, the same income seeking investors who had previously sat in cash found themselves drawn into riskier and riskier investments and expanded asset classes to find a sufficient yield. Hence, investors piled into REITs and listed infrastructure, compressing their yields and inflating corresponding valuations. As these conditions normalise, the yield demanded from bond proxies will rise, and more than likely cause valuations to fall.

Figure 1. Total return on $100 invested in different asset classes, 2000-2007

Source: Thomson Reuters

Figure 2. Total return on $100 invested in different asset classes, 2008-present

Source: Thomson Reuters

At the same time, the discount rates – typically a WACC for infrastructure and Cap Rate for REITs – used to value the underlying assets will increase as the risk-free rate, for which government bonds are the common proxy, increases. Since the GFC, REITs have enjoyed a strong tail wind in the form of falling cap rates, taking their lead from private markets. As was demonstrated in November of 2016, we believe this trend could reverse quickly should bond yields begin to rise, shrinking valuations. Our own central bank is aware of these issues and is also contending with a stubbornly strong Australian dollar, which it is trying to keep closer to 70 rather than 80 US cents. As the US itself continues to raise its own rates and other developed economies such as Canada and the EU follow suit, pressure will eventually build for Australia to do the same.

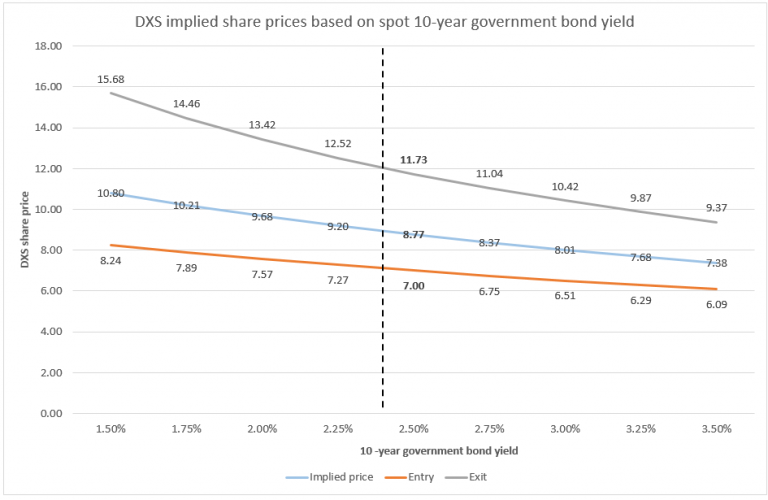

One model we are aware of when forecasting prices of bond proxies is the historical spread (premium) of their dividends over government bond yields to determine what the market is willing to pay for them. For example, Transurban has historically offered a yield of 2.2% over 10-year government bonds. If we extrapolate that premium onto the current yield (around 2.4%), we get an implied share price of $12.21 (based on a forecast distribution of $0.57). The stock’s prevailing market price has fallen below this level, implying that the investors have begun to take a view that long-term bond yields have bottomed. If we conduct the same analysis on Dexus Property, one of the premier REITs in the Australian listed market, we see a somewhat different story with current prices seeming to imply some further head room for valuations.

![]()

Figure 3. TCL implied share prices based on government bond yields

Source: Thomson Reuters, Clime estimates

Figure 4. DXS implied share prices based on government bond yields

Source: Thomson Reuters, Clime estimates

Our own views mirror the above, with REIT’s still using higher cap rates than private markets in many cases and therefore still offering some growth potential in the short-term. We remain more cautious around listed infrastructure, which despite retracing from recent highs, still looks very expensive in our view. Regardless of your own expectations of what the future may bring, understanding the relationship between bond yields and bond proxies is imperative. They are some of the most widely held stocks in the market and have been primary beneficiaries of an extremely accommodating monetary regime which may be reversing sooner rather than later. While it may not be time to rush for the exits just yet, particularly where REITs are concerned, the prospect of rising yields should be at the forefront of investors’ minds when making capital allocation decisions in the pursuit of yield opportunities.

Contributed by Damen Kloeckner, Analyst.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

3 stocks mentioned

Clime Investment Management

Funds Management & Stock Research

Clime Investment Management

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

Expertise

Clime Investment Management

Funds Management & Stock Research

Clime Investment Management

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management