Is retail facing a fiscal cliff or a speed bump?

Australian retailers have overcome a number of hurdles in recent years, from challenging macroeconomic conditions and a slowing housing market to the trend towards e-commerce and, more recently, the impact of COVID-19. Despite this, a select group of high quality retailers have been performing strongly in recent months. Now, COVID-19 has raised another potential challenge: the risks associated with a potential “September fiscal cliff” when key fiscal support measures are due to expire. This newsletter discusses our thoughts on the fiscal cliff and how these retailers are positioned to navigate this period.

In March, it was feared that COVID-19 would present a particularly challenging scenario to Australian retailers, with potentially no revenue from physical stores for an indefinite period and ongoing business operating expenditures, leading to losses and stretched balance sheets. Not only have a group of Australian listed retailers avoided this scenario, they have instead reported solid sales results in recent months. Some highlights from recent trading updates are below:

- Wesfarmers (9-June): CY20 YTD revenue growth of 19.2% at Bunnings. CY20 YTD online revenue growth of 89% across Wesfarmers.

- JB Hi-Fi (11-June): CY20 YTD revenue growth of 20.0% at JB Hi-Fi Australia and 23.5% at The Good Guys. Management also noted a “significant acceleration” in online sales. FY20 profit growth of 20-22% is expected ($60m higher than management expectations in February on an underlying basis).

- Super Retail Group (15-June): Reported financial year to date revenue growth of 1.2% to 23 May, slightly lower than the 1.9% growth it had reported in February prior to the impact of COVID-19. Specifically, its major divisions saw financial year to date revenue growth of 4.6% for Supercheap Auto and 2.1% for Rebel, with declines for the smaller brands of 0.6% for BCF and 10% for MacPac. Revenue had “continued to benefit from the strong consumer environment in June”. Online sales growth of 126% was achieved over April and May.

- Nick Scali (19-June): After store closures materially impacted April sales, furniture orders in May and June were up 54% on the prior year. The company advised that 2H FY20 profit growth of 15-20% is expected, driven by cost reduction initiatives. The strength of sales orders in May and June, which will be recognised as revenue in Q1 FY21, have already “underwritten” profit growth in 1H FY21 according to management. Nick Scali has launched a digital offering over the COVID-19 period and “is pleased with the growth it is demonstrating and sees further scope to invest in this capability”.

- Motorcycle Holdings (24-June): The number of motorcycles sold in May “substantially exceed normal levels”, a trend which has “continued into June” according to the company. Federal Chamber of Automotive Industries data indicates Australian motorcycle sales volumes have grown 24.5% over CY20 YTD. Motorcycle Holdings’ FY20 underlying EBITDA growth is expected to be between 33% and 50% (even though 1H FY20 EBITDA was below FY19 levels).

These retailers have benefited from a high level of consumer demand in recent months, which has clearly been supported by the elevated levels of fiscal and monetary stimulus in response to COVID-19. In addition, gross margins have generally been good and cost reduction measures (including the benefit of JobKeeper in some cases) have reduced operational costs. This means profit for the above retailers should also be solid.

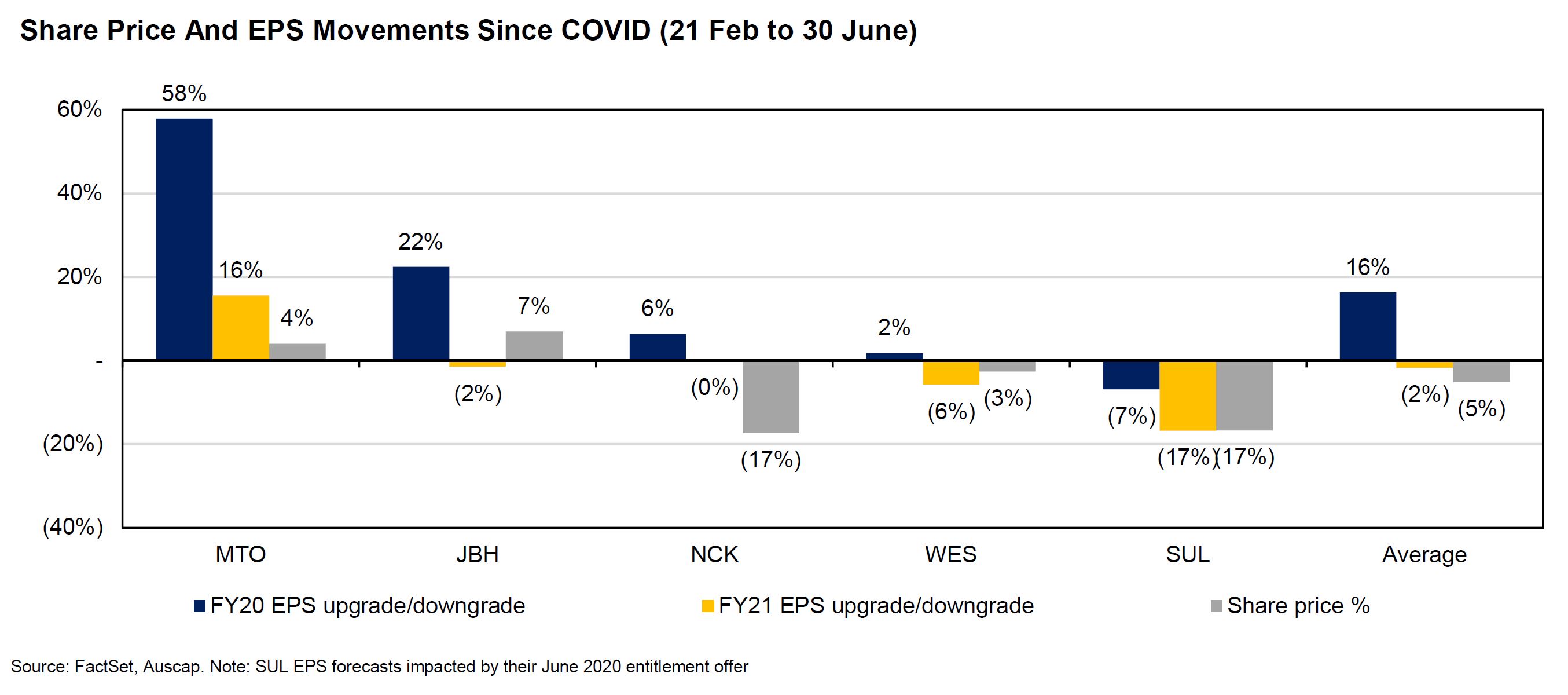

Over time, the share price performance of a company tends to track the growth of its Earnings Per Share (EPS). Since COVID-19 hit markets in late February, sell-side research analysts have upgraded their FY20 EPS estimates for the above retailers by an average of 16%. These large EPS upgrades are in stark contrast to the broader ASX market, which has seen FY20 EPS downgrades of approximately 20% since February. Despite the strength in FY20 for this group of companies, their share prices are on average below pre-COVID levels, no doubt in part driven by the changes analysts have made to forecast earnings which have resulted in, on average, modest downgrades to their FY21 EPS estimates.

Evidently, equity markets are unwilling to extrapolate the recent retail sector strength beyond FY20. This is largely because some key fiscal support measures, particularly JobKeeper, JobSeeker and the early release of superannuation, may be wound back in September, which has the potential to cause a decline in consumption, employment and economic activity – the “fiscal cliff”. Retailers have of course been major beneficiaries of these schemes and few would argue that the much-discussed current acceleration in spending can continue at its current pace. Nevertheless, given this heightened level of market scepticism, it is worth considering five factors that could lead the performance of these retailers to continue to positively surprise the market.

5 factors to watch in retail

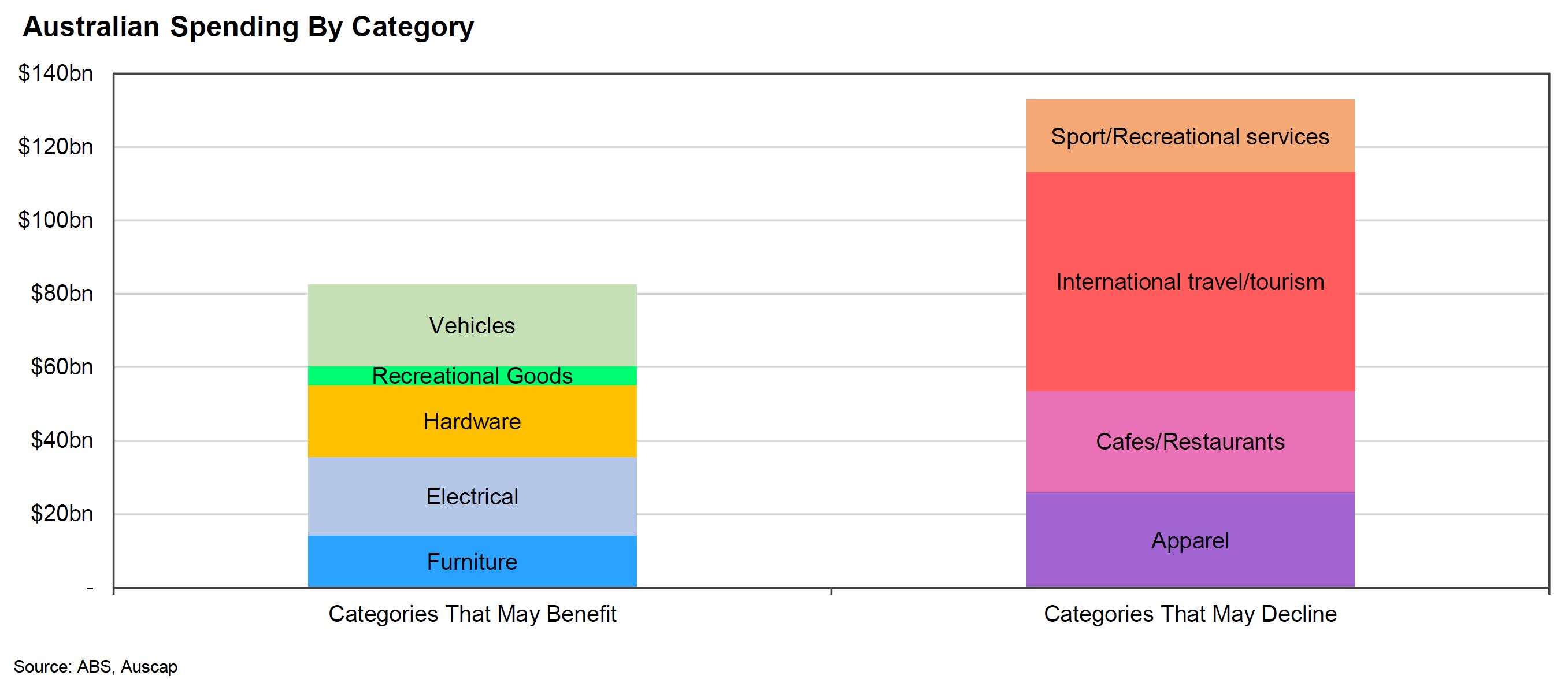

- Firstly, not all types of consumer discretionary spending have been impacted equally by COVID-19. Some categories that are directly impacted by COVID-19 (e.g. international travel) will see steep reductions in spending, creating new pools of cash that can be partially diverted elsewhere, including to listed retailers. Australians spend approximately $60bn per year on international travel and tourism, $28bn on restaurants and cafes, $26bn on apparel and footwear and $20bn on recreational and cultural services. These categories are likely to see some level of reduced spending for as long as social distancing is in place and borders are closed. With Australians spending $55bn a year on household goods (electronics, furniture and hardware), $22bn on motor vehicles and $5bn on recreational goods, even a modest continued diversion from the affected categories could be material.

- Secondly, a portion of new spending is genuine new demand, as opposed to a “pull-forward” of demand from future periods. COVID-19 has forced Australians to make significant lifestyle changes in recent months. These changes include a dramatic rise in time spent at home, a drop in public transport usage and an increased capacity to undertake household projects. This has led to new demand for motor vehicles, home offices, home gym equipment, entertainment units, hardware goods as well as home furnishings. Further, categories that are exposed to domestic tourism, road travel and outdoor activities should see continued growth in demand. Because a portion of the incremental money spent in these categories is solving a new need, this portion of spending is less likely to negatively impact future demand. In fact, it could even create a new need for additional products and services in these categories over the coming years.

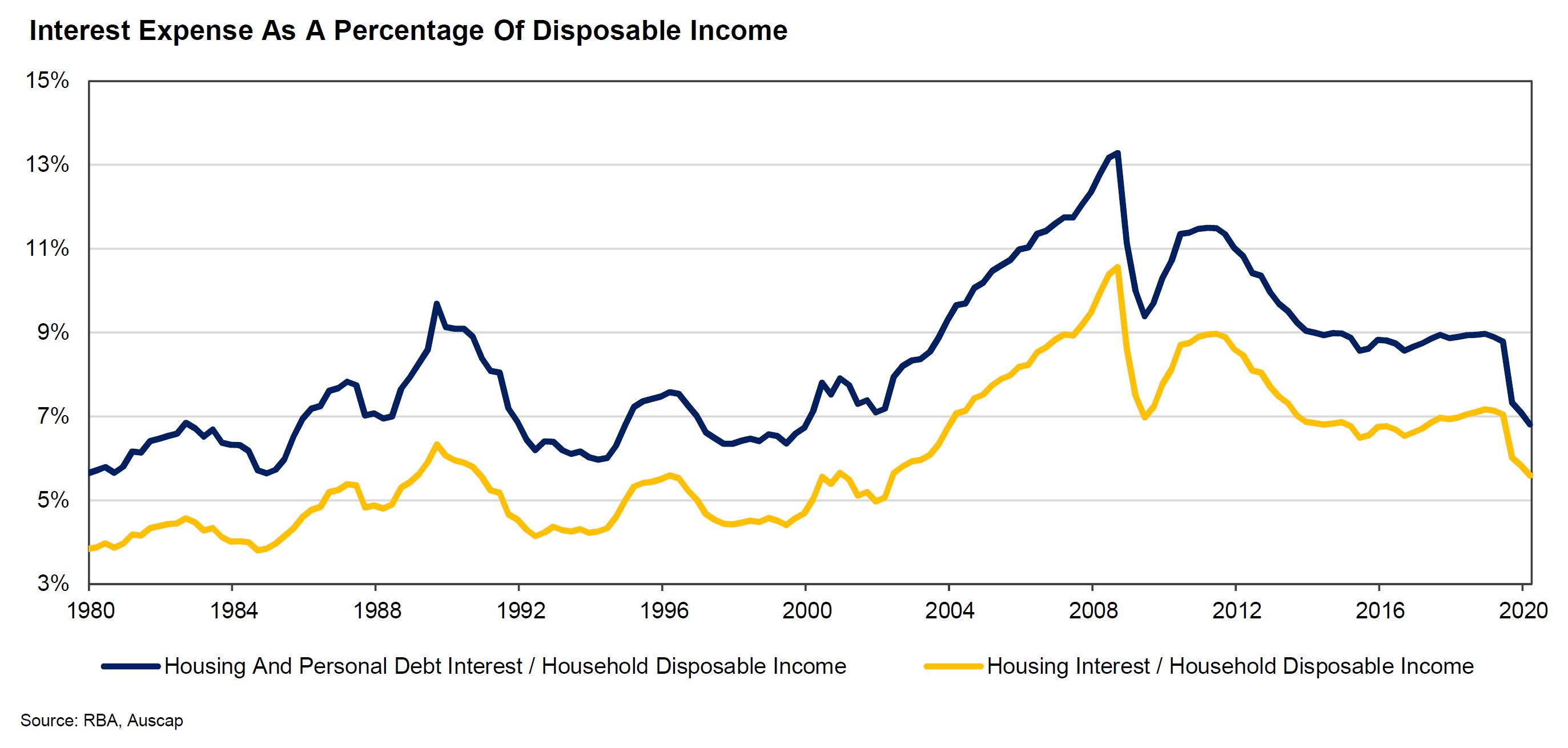

- Thirdly, the JobKeeper and JobSeeker programs have not been the only positives for consumer disposable income in recent months. The Reserve Bank of Australia has cut the cash rate to 0.25%, whilst providing forward guidance that this course will not be reversed for some time, pushing household interest serviceability to multi-decade lows. Rental costs and fuel costs, both significant contributors to Australian inflation, have fallen. As discussed in last month’s Auscap Newsletter, there are significant government stimulus programs directed at the housing market. Press reports also suggest that the July Federal Budget may lead to a permanent increase in JobSeeker/Newstart payments and a pull forward of personal income tax cuts. These factors are all major reasons to be positive on Australian discretionary spending.

- Fourthly, sharply withdrawing stimulus measures in September is unlikely to be in the best interests of the Federal Government. A “cliff” scenario in September would be deeply politically unpopular, run the risk of plunging the country into a much deeper recession and could create a perception of “government mismanagement”. Unlike the Global Financial Crisis, COVID-19 has no obvious villain or sector to blame. Instead, Australian individuals and businesses alike have simply followed government instructions, which has led to short term economic pain. Subsequently, there is no moral hazard argument for allowing previously profitable Australian businesses to fail. Prime Minister Scott Morrison has already confirmed that he will implement a second phase of JobKeeper beyond September, whilst acknowledging it is likely to become more targeted. The Australian Banking Association has also confirmed that customers who are still struggling financially due to COVID-19 can defer their loans for an additional four months beyond the initial September deadline. Similar announcements are likely to be made in coming weeks.

- Finally, Australian retailers have been taking full advantage of the recent crisis to create permanent benefits for their businesses. Nick Scali has launched an online offering and permanently optimised its store hours. Wesfarmers has taken significant steps towards restructuring its underperforming Target business. Super Retail Group has invested heavily in its digital capabilities and supply chain. AP Eagers has permanently reduced its work force by approximately 1,200 staff. These initiatives should help to underpin the profitability of these businesses in coming years.

Conclusion

To conclude, we are not suggesting that the currently elevated levels of retail sales and earnings growth will continue indefinitely. However, the market has heavily discounted the recent strength due to its broader concern regarding the looming September “fiscal cliff”. We think the market may be overestimating the size of the cliff and underestimating other factors at play. Given current valuations of Australian retailers, we remain positive on the sector and excited about the prospects for these companies.

Get investment insights from industry leaders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short portfolio using Proprietary funds. Prior to 2007 he worked at Macquarie Bank within the Investment Banking Group. Tim is a CFA charterholder, a CMT charterholder, a Senior Associate of FINSIA, a Graduate of the Australian Institute of Company Directors (GAICD) and has a Bachelor of Laws (Hons) from the University of Sydney and a Bachelor of Commerce from the University of Sydney.

........

Tim Carleton is a Principal and Portfolio Manager at Auscap Asset Management (Auscap), a boutique equities long/short investment manager. This article contains information that is general in nature and does not constitute investment or any other form of advice. This article does not take into account the objectives, financial situation or needs of any particular person nor does it constitute a recommendation to be relied upon when making an investment or any other decision. You need to consider your financial needs before making any decision based on the information in this article and a person should obtain and consider the relevant disclosure document before deciding whether to invest in an Auscap fund. No part of this article is to be reproduced or disclosed without the prior written consent of Auscap. In relation to any MSCI data in this article, the MSCI data is comprised of a custom index calculated by MSCI for, and as requested by, Auscap. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

2 topics

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short...

Expertise

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short...

Expertise

Comments

Comments

Sign In or Join Free to comment