Janus Henderson: Merger Making Progress

Janus Henderson Group (JHG) is a global asset manager listed on the ASX and NYSE. In 2017 London based Henderson Group (which was created after its spin-off from AMP in 2004) merged with US based Janus Capital to form Janus Henderson. The company provides investment management services across retail and institutional channels throughout Europe, North America and Asia. As at December 2017, JHG reported US$371 billion AUM, more than 2,000 employees and offices in 27 cities worldwide.

The Group posted a strong 4Q17 result ahead of most brokers estimates driven by a bump in performance fees and better cost controls already flowing from the merged entity. FUM closed up over US$423m for the 3-month period reflecting the benefits of scale in distribution. Debt is decreasing as cash flow improves along with a meaningful reduction in the tax liability driven by US tax cuts offering investors exposure to this thematic as well.

Some highlights from the December Quarter:

- 4Q NPAT of US$147.9m

- FY17 NPAT of US$503.9m

- 4Q performance fee of US$33.5m

- 4Q net-flows of US$2.9b driven by the US Quant Fund returning to over 90% outperformance in FY17 which should drive further net positive flows in future periods.

Balance Sheet and Financial Position

As at 31 Dec 2017, cash and investment securities totaled nearly US$1.5 billion compared to outstanding debt of US$379 million declining 7% or US$27m from an early conversion of Senior Convertible Notes. Cash and investment securities increased 6% as strong cash flow generation was partially offset by a dividend payment and the aforementioned convertible note repayment. We view this conversion as positive for the stock as these sophisticated investors early conversion view the equity as cheap relative to debt on a risk adjusted basis.

Looking Ahead to the 1Q18 Result On 9th May

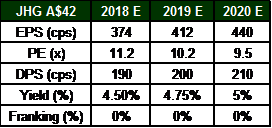

We are expecting 1Q18 to be another solid result with the market potentially rerating the stock to reflect the benefits of last year’s merger. We believe JHG is currently trading at a value which puts a low estimation of the business and management to execute on the stated ~US$80m a year in cost synergies along with upside to increased global distribution - trading at a little over 11x FY18 P/E multiple and paying a 4.5% unfranked dividend yield. We are expecting at least US$20m of realised cost synergies, a slight dip in FUM to US$365b driven by recent volatility in global markets and a dividend of US$0.37/share.

Catalysts and Outlook

1Q18 should deliver another good result for the Group reassuring investors of the benefits to the merged JHG, however material catalysts to the stock may take longer to eventuate. However, some potential nearer term catalysts for the Group going forward:

- Announcement of a share buyback at the 2Q18 result

- Lower AUD

- Major shareholder Dai-Ichi (currently 12.5% of the company) moving up the register

- Achievement of cost synergies which we view is not really currently priced into the stock

- Improving investment performance

Longer term we see upside to:

- Positive flows driven by cross selling and further penetration of the Japanese market

- Launching new investment products

We expect JHG’s business environment to improve after the recent volatility in global markets. We are also expecting a stable to improving operating margin and nearly 15% CAGR in earnings over the next 2 years at a minimum. JHG stands out as good value in the large cap wealth space offering investors exposure to earnings in the US and Europe.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

1 topic

1 stock mentioned

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Comments

Comments

Sign In or Join Free to comment