June Market Commentary: Ten Years on What Have We Learnt?

Risk assets were mixed in June with equities, credit and commodities all seeing ups and downs. Equities in the China (5.0%), Japan (2.0%) and the US (0.5%) did well, European equities (-3.2%) were down and Australian equities were flat. Investment grade credit saw small gains whilst high yield credit had small losses, mostly driven by the drop in the oil price. For commodities, it was iron ore (14.0%) and copper (4.9%) doing well, with US oil (-4.1%), gold (-2.2%) and US natural gas (-1.0%) falling.

This month is the ten year anniversary of the beginning of the credit crisis in June 2007. Whilst things got a lot worse over the next 21 months into the lows of March 2009, asset prices have risen a long way since then. If you want to understand why asset prices have done so well since then there’s three drivers you need to grasp.

Firstly, governments responded to reduced private sector demand by stepping up stimulus spending. That’s slowed a little in more recent years but government debt to GDP now is way above where it was 10 years ago and is still rising. In a normal market that growth in debt would have seen the interest rates paid by governments increase but that hasn’t happened.

The second key driver and the reason that interest rates have fallen so far is the actions of central banks. By sending reserve rates to zero and below, and by printing far more money than was needed to cover the increase in government debt, central banks killed the normal incentives to save and invest. Why bother engaging in productive business activities when it is far easier to speculate through borrowing money and buying existing assets.

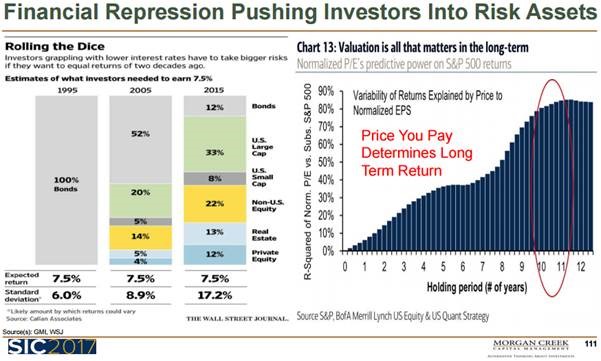

Thirdly, yield chasing by investors has allowed global debt levels to increase. The combination of low rates and lack of supply of government debt (see no.2) saw investors pushed out to riskier asset classes. This enabled the boom in high yield debt, emerging market debt and consumer debt at interest rates well below historical levels. Companies have used additional debt to buy back their own stock and buyout competitors pushing stock prices up. Consumers used the additional debt to push up property prices and fund consumer spending. The graphic below from Morgan Creek shows how investors have had to change their portfolios to meet return targets.

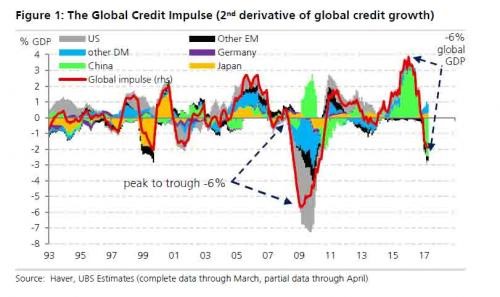

Those drivers have worked well for eight years, but each of the three drivers is now at risk of reversing. Government debt in some countries is at levels where it is tough to see the country ever repaying their debts. In many cases, the outright debt levels can appear reasonable but the addition of pension deficits means effective debt levels are unsustainable. Central banks are starting to raise rates and reduce money printing in the US and are talking about going in that direction in Europe. Finally, the stimulus provided by credit growth is now becoming a headwind as repayments reduce future consumption. The graph below from UBS shows how global credit is now growing at a slower rate than it has, pointing to economic growth rates being lower than they have been.

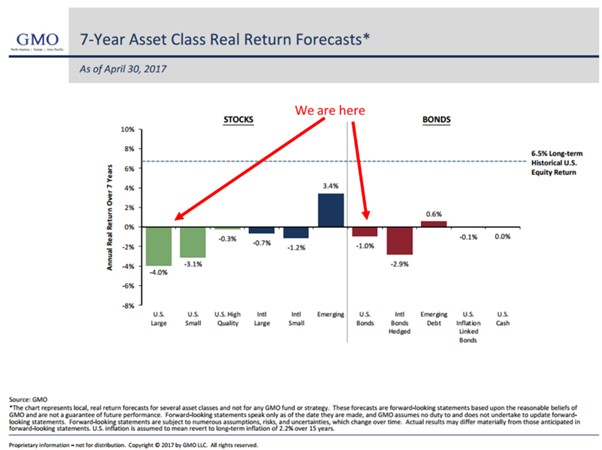

For investors, the gap between what is expected and what is likely to occur is widening. A recent survey by Legg Mason found that investors expect 8.6% annual returns, which is about what historical returns have been. The updated return forecast from GMO below shows there’s nowhere to go to get this.

If nothing else it is fun to chronicle the irrational exuberance that current markets bring. Crypto currencies have boomed this year but experienced wild volatility this month. The second biggest crypto currency, Ethereum, has been called a bigger bubble than tulips after rising 3500% in six months. The CAPE ratio of the S&P 500 above 30, a level only surpassed in the lead up to the great depression and the tech wreck, is quite tame by comparison.

In credit new money is pouring into leveraged loans and private debt at a time when covenants are falling away in the US, Asia and Europe. Edward Altman sees high yield conditions as bad as they were in 2007 but Bloomberg has five reasons not to be worried about high yield debt. Emerging market credit spreads are the lowest since 2007 and weaker countries are growing their share of the outstanding debt. Does risky debt + low margins = credit bubble?

I can’t finish this section without highlighting some positive economic news during the month. The US is seeing strong growth in income tax withheld this year, although it has started to trend down. German business confidence is at the highest level in 26 years. Britain has recorded its best factory orders in nearly 30 years. It’s not all bad out there!

China

The near term outlook for China is cloudy, with some conflict amongst the economic readings. The government crackdown on debt is having impact, Goldman Sachs is calling a sharp drop in credit. Short term bond issuance and shadow bank lending are plummeting. Defaults are now expected in the second half of the year on local government financing. The government has stepped in and bought one year bonds in order to provide liquidity to a worried banking system. Whilst May economic readings were generally steady, the sentiment gauges are weaker.

The debt crackdown has expanded to include large corporations that have been on an acquisition binge in recent years. The regulators are asking questions about overseas borrowing used to fund the purchases of overseas assets. The Chairman of insurer Anbang has been detained. Anbang is a large issuer of wealth management products and the banks that sold those products to their largely retail customers have been instructed to stop selling Anbang’s products.

Anbang’s revenues and product issuance have plunged, creating fears the underlying borrowers may not be able to refinance when their existing debts mature. Anbang has been likened to Lehman Brothers and AIG; it is tempting for pessimists to see this as the beginning of the end for China’s boom. However, it is also possible that its borrowers will refinance with other shadow lenders or the government will bail everyone out and this episode will soon be forgotten.

China has scored another win on its path to global integration, MSCI is adding Chinese stocks to its emerging markets indices. The decision was somewhat controversial, Bloomberg has six things international investors need to watch when investing in Chinese shares. The government has given the green light for global credit rating agencies to begin operating in a more fulsome way from July. I’m looking forward to the rating comparisons. For example, if a global rating agency says CCC but a Chinese rating agency says AA will Chinese investors care? Another reminder of the relatively shallow development in China’s finance sector is corporates encouraging employees to buy shares with a guarantee from the company to cover any losses. That looks like a good trade until the company goes broke.

Emerging Markets

After recently defaulting on its debts, Puerto Rico is now looking for investors to join them in public private partnerships on infrastructure assets. This month its proposed restructure of the debt of its electricity provider was rejected by the control board as being too debtor friendly. The electricity provider looks set to go through bankruptcy as well. Given that, investing in other infrastructure assets is very much a buyer beware situation. Puerto Rico also serves as a reminder just how expensive bankruptcy is having already spent $154 million on advisers. If you add in what the debt holders have spent it could be more than double that already with a deal a long way away.

If the oil price remains down there will be significant financial ramifications for the Middle East and other emerging markets that earn much of their revenue from oil. Many government budgets are based on an oil price well above current levels. Defaulting on debts would be a much more politically palatable decision than heavy cuts to government welfare or increasing taxes. A gas producer in the UAE is claiming that its sukuk bonds are non-compliant and therefore must be restructured with the interest rate halved.

Argentina’s issue of a century bond was made possible by yield chasing and an “I’ll be gone, you’ll be gone” attitude. The yield of 7.9% is only 4.9% higher than the US 30 year government bond, implying investors need at least 15 years of payments plus some recovery on a default to beat the safer alternative. As Argentina has defaulted four times in the last 35 years that looks like a pretty poor gamble.

Banking Bad

The bail-in of Banco Popular and the bailout of two Italian banks was the standout development this month and I’ve written an article on it here. Much less well covered was the decision by Bremer Landesbank to stop paying dividends on its preference shares/AT1 securities and the debt for equity swap at Co-op bank.

The US Federal Reserve conducted another round of bank stress testing and this time everyone passed. However, the Fed’s tests are getting easier. The Europeans are getting tougher on their stress tests after starting from a very low point. The key takeaway from the US tests is that corporate and credit card debt are expected to do the most damage to bank balance sheets in a recession. For European banks, some are unprofitable and arguably insolvent without cheap ECB funding. On the subject of stress testing, we should stress test governments as well.

The Bank of England has decided to lift the countercyclical capital buffer from 0% to 1% over 17 months. With UK household debt growing at over 10% per year they should be lifting it further. India’s central bank has had enough of delays and is forcing twelve large distressed companies into bankruptcy. The online lender Sofi is applying to be a bank. The cheapest funding for marketplace lenders is from securitisation or bank deposits so this is a path others are likely to follow.

Funds Management

In the ongoing active versus passive debate there’s a few points that always seem to get forgotten. Firstly, very few investors care much about active versus passive, what they really care about is the fees they pay. Second, there’s no such thing as purely passive as you have to pick which index you want to follow. An example of the first point is the huge flows to ETFs this year, mostly to funds with fees 20bps or less. The downside of the increasing use of ETFs is that whilst they might be very liquid themselves, they take liquidity away from the underlying stocks. Along similar lines people are asking whether smart beta or quant funds could cause an LTCM style sell-off? Also worth considering is whether investors are better off spending their time picking fund managers for alpha or investment styles for beta.

Whilst the headlines are mostly on the potential growth of robo advisers, US based Creative Planning has grown into a behemoth adviser by providing independent advice with old fashioned customer service. An academic study found that hedge funds with more investment by the managers get better returns. The hedge funds that investors should really worry about are the ones where the key individual also runs a family office for their own funds. (Why don’t they eat their own cooking?) Worth noting is the five red flags we can take from Bernie Madoff’s scam.

Government Debt and Pension Problems

Illinois was downgraded to BBB- by S&P and Moody’s with the expectation it will be downgraded to sub-investment grade in the near term. The biggest buyers of the debt say they won’t have to sell if it is downgraded further, but there was a substantial blowout in the credit spread this month. Illinois has lots of debt, a bigger pension deficit and gridlock in its parliament that has resulted in no budget being passed for two years. Unpaid bills are topping $15 billion with a long list of services being cut as only mandatory spending is approved. The Governor has commented that “we’re like a banana republic” and “we can’t manage our money”. Elsewhere in US government debt, San Bernardino has exited bankruptcy with its debt slashed, but high wages and unfunded pensions remain.

In pension fund news, China has a pension funding problem but few are estimating how big it is. Changes to the Dallas police pension fund have been approved by the Texas legislature including increasing the retirement age and reducing guaranteed returns. However, it is estimated to take 46 years to get back to a fully funded position and that is with everything going right. I expect we’ll hear more about this fund in the medium term. The problem for Dallas and almost all pension plans is the overestimation of future returns. Moody’s ran a scenario where investment returns were -5% for one year, with the outcome that underfunding increase by 25% of current payroll.

Media Worth Consuming

A CNN producer says the Trump/Russia narrative is all a beat up and three CNN reporters resigned over a fake Trump/Russia story. Trump tweets asking why Hillary hasn’t been charged for widely known evidence whilst he is being invested on speculation. Hillary has 24 things to blame for her loss and she isn’t one of them. Trump wonders why people don’t trust him, perhaps his long history of lying is coming back to bite him.

Virginia’s governor repeatedly says 93 million Americans die a day from gun violence before being corrected by journalists. Brazil’s carwash scandal could be the largest corruption case in history at $5 billion. Translating the list of demands Saudi Arabia has for Qatar. Saudi Arabia’s meddling in Indonesia is just another example of how it creates trouble around the world. More people would like to migrate to Australia than live here. Ben Bernanke thought subprime was contained, now Janet Yellen thinks we won’t see another banking crisis in her lifetime.

The knives are out for Tesla and Elon Musk including calling Musk a crony capitalist extraordinaire. China is building far more batteries than Tesla and GM is building their batteries cheaper than Tesla. Resale prices are expected to fall for older models once the model 3 is released. Discounts for new buyers have jumped as inventory is too high. Tesla insurance premiums have gone up as they are more frequently involved in accidents and the repairs are more expensive. The adage that 90% of VC backed start-ups fail is a myth, it is more like 60%. Alarmist climate change predictions keep being deferred.

20% of Norway’s working age population is on unemployment or sickness benefits. An Austrian steel plant is run by 14 workers. Getting teens into work cuts crime rates. Seattle’s minimum wage increase saw hours worked fall 9.4% and left low skill workers earning less. Cheaper housing is a better way to help low income people than higher minimum wages.

The US is encouraging the wrong type of entrepreneurship – rent seeking and crony capitalism. Full employment is a reality in 73 US counties which have official unemployment rates of 2% or less. Maine is laying off unemployment counsellors as its unemployment rate hits a 32 year low. Some employers there are whining about not being able to get temporary workers from overseas who are cheaper than locals. Denmark is struggling to attract high skill migrants when its unemployment rate is low. Over the last 150 years hours worked per person has declined despite huge improvements in the standard of living, but gains are trailing off.

Social media has enabled the shouting class to be heard. Canada passes a law criminalizing the use of wrong gender pronouns. Most financial models are wrong, but if you are expecting perfection you’ve forgotten that models are meant for scenario analysis. A second property in Manhattan’s billionaires row has been repossessed with $35m owing. UK borrowers with negative equity become “mortgage prisoners”, they can’t sell and can’t refinance.

Gangs of killer whales are picking off the catch of commercial fishing boats. A cynic’s translation of investment management clichés. How Burger King was turned around by a CEO who walked around. Why men die earlier. The whistleblower in the Caterpillar $2 billion tax fraud case is looking at a $300-600m payout if the case succeeds.

A fake but hilarious ad for the Uber CEO vacancy. Poland cracked down on VAT under collection and its budget deficit has almost completely disappeared. A New York casino won’t payout on a $43 million jackpot, claiming the machine malfunctioned. Angry Chinese investors feed a donkey to tigers at a zoo. An academic gets his dog on seven editorial boards to show how rubbish some academic journals are. Spring looks pretty good underwater in Antarctica. Overnight success is a myth. A French General regularly used a fighter jet to travel to his holiday home.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment