Two beneficiaries of the $24bn infrastructure pipeline

Public infrastructure spending in Australia has a positive outlook for the medium-long term, with government announcements and global trends indicating that large public infrastructure companies will have a multitude of projects in the pipeline. Two of these beneficiaries are ASX-listed companies Boral (BLD) and Adelaide Brighton Cement (ABC).

In the most recent budget, the government announced a $24bn infrastructure pipeline over the next 10 years. This predominately consists of upgrades to transport on major regional roads and highways.

Figure 1 - 10 year national infrastructure plan ( 2018 budget)

This comes off the back of a growing global theme of urbanisation and the requirement for ongoing infrastructure development.

Australia is currently in the early stages of a strong infrastructure cycle in key east coast markets. The three key eastern seaboard states, VIC, NSW & QLD, are projected to benefit the most, with almost 80% of that allocated project budget.

Boral and Adelaide Brighton Cement

A key recipient of this year’s budget is building and infrastructure exposed stocks. Two of those stocks include Boral, Australia’s largest construction materials and building products supplier, and Adelaide Brighton Cement, one of the leading manufacturers and importers of cement.

With the increase in planned infrastructure spending on the east coast, BLD and ABC have increased operations and exposure in these areas to account for the excess demand in the future. This excess demand and further tightening of potential supply is resulting in companies being able to deliver better pricing outcomes. Boral has implemented two price increases in the last two years, with an expectation to continue this trend in the future. Similarly, Adelaide Brighton Cement has increased prices of cement by up to 50% due to these strong economic conditions.

With underlying demand and pricing trending higher, both companies should be well placed to grow their operating margins over the next several years.

Energy costs a headwind

However, higher energy costs remain a significant headwind for Australian industrial companies. Heightened attention to cost reduction and operational improvements is central to alleviating energy costs. For Boral, higher energy prices have had an estimated $20m effect for FY18. Nevertheless, the trajectory of price increases in construction materials are helping alleviate the cost pressures associated with higher energy prices.

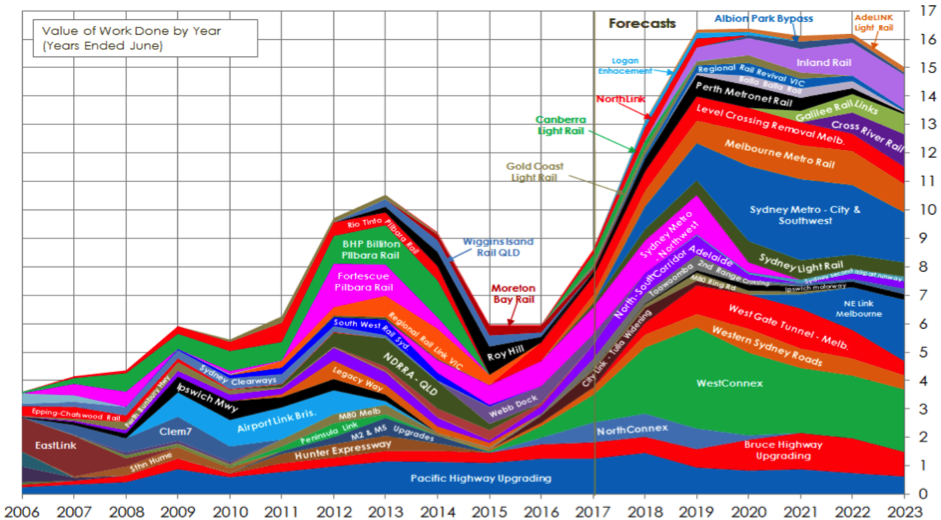

Figure 2 - Major transport infrastructure construction projects. Sourced Macromonitor construction materials forecast, February 2018 estimates. Presented at May 2018 Boral Investor Day.

The requirement for greater infrastructure spending by Federal and State Governments has become more urgent following only modest spending in 2015 and 2016. By contrast, the projected spend on infrastructure projects is forecast to reach c.$16bn by the end of 2019.

Vertical integration a key advantage for Boral

With these projects involving many different suppliers, it becomes increasingly important to have key competitive advantages over competitors. Boral’s vertical integration model provides control over the entire construction supply chain, from its upstream assets, such as quarries, providing low-cost inputs to its downstream concrete and asphalt networks.

Undoubtedly, Boral’s extensive geographic and operational national footprint is a key competitive advantage in terms of its ability to participate in the major national projects planned over the next decade.

Moreover, Boral’s international exposure to the thematic of infrastructure was bolstered by their acquisition of US building materials firm Headwaters in 2016. The company’s dominant North American exposure in Fly Ash (a supplementary material used in the production of concrete) is well placed to benefit from a growing need to replenish ageing infrastructure assets. The trend of increased US infrastructure spending is supported by a study of the American Society of Civil Engineers estimating that US$4.6 trillion is needed by 2025.

Adelaide Brighton well positioned

In Australia, Adelaide Brighton is also strategically well positioned to be a beneficiary of the extensive pipeline of infrastructure projects. Adelaide Brighton is the second largest supplier of cement and clicker products in Australia. In addition, the company is the largest producer of industrial lime in Australia. Critically, Adelaide Brighton’s competitive position is supported by its integrated network of production, manufacturing and distribution facilities.

The thematic of urbanisation is placing unprecedented demands on public infrastructure. Growing populations in our major cities is critically highlighting the need for ongoing infrastructure investment. Indeed, the fabric of Australia’s economic and social well being is inextricably linked to the quality of public infrastructure.

The recognition by governments to invest in large infrastructure projects is now being realised by an increasing number of announced projects. With the demand environment supportive for improving infrastructure spending over the course of the next decade, ABC and BLD are well positioned to be beneficiaries of this attractive thematic.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Marcus is the co-founder and CIO of Blackmore Capital. Marcus' career spans over 27+ years focussed on Large Cap Australian Equities including work as a research analyst at McIntosh/Merrill Lynch, Portfolio Manager at Cooper Investors, and CIO (Asia Pacific) for Canaccord Genuity.

2 stocks mentioned

Marcus is the co-founder and CIO of Blackmore Capital. Marcus' career spans over 27+ years focussed on Large Cap Australian Equities including work as a research analyst at McIntosh/Merrill Lynch, Portfolio Manager at Cooper Investors, and CIO...

Expertise

Marcus is the co-founder and CIO of Blackmore Capital. Marcus' career spans over 27+ years focussed on Large Cap Australian Equities including work as a research analyst at McIntosh/Merrill Lynch, Portfolio Manager at Cooper Investors, and CIO...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets