Killing me softly with retail

Pat Barrett

UBS Asset Management

The retail sector has been impacted by a combination of cyclical and anticipated structural issues. Cyclically, retail sales have been under pressure due to higher living expenses (higher debt costs and utilities) which have grown faster than wages. Structurally the market is anticipating much weaker conditions given the arrival of Amazon and other disruptors. I highlight the word 'anticipation' because that's all it is, with Amazon years away from a full-service offer in Australia.

Investors should note that REITs are landlords to the retailers, who have signed long-term lease commitments, often with rental guarantees in place. These retailers are bound by contract and have to pay rent before they can pay themselves. The landlords work very closely with retailers to assess their situation and have dedicated teams to deal with potential insolvencies or trading difficulties.

We focus on the facts (earnings) and while we have lowered our growth expectations for retail landlords, the price falls for world class mall operators is extreme. From an earnings perspective, around 5/6ths of all mall leases automatically rollover each year with ~3.5% growth, which means that rents on those expiring tranches can fall ~17.5% for revenue to standstill.

While we do think Amazon and other ecommerce operators will increase market share, we think it will be at the expense of malls in secondary locations where retailers are ambivalent about their presence. Pleasingly the REITs generally own trophy centres with strong demographics (high incomes, asset rich, growing population) and have sold most of the underperformers in the past few years. By way of example the REITs own Chadstone, Fountain Gate, Emporium, Sydney, Bondi Junction, Chatswood, Chermside, Carindale, Marion, to name a few. Retailers want to have a presence in those markets, with many having flagship stores in those centres.

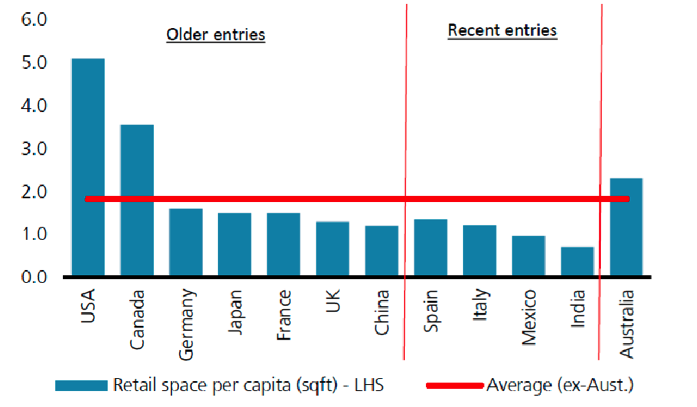

Much of the negative news flow emanates from the US where there have been multiple store closures. The starting point is that there is almost 2.5x as much retail space per person in the US vs Australia, with 5m2 per person in the US vs 2 m2 per person in Australia. Anecdotally around 1/3 of their malls are under pressure to close given poor demographics in struggling cities (high unemployment and population declines), another 1/3 are average and 1/3 are Class A malls (good quality). The US REITs have focused upon the top end malls which have performed much stronger than the bottom end malls. Despite the fact that Australia is blessed with population growth and less retail per person, many of the offshore based Fund Managers have simply chosen the thematic trade and sold mall owners everywhere!

Figure 3: Relative retail space per capita

Source: Urbis, ICSC, Japan Council of Shopping Centres, CRE Global Investors, Cushman & Wakefield, UBS estimates

While the local market will be impacted, we think it will withstand the pressures better than most markets given the tight planning laws here, the lack of comparative supply, the non-discretionary focus of most centres, the influx of international retailers, and the relative balance sheet strength of the AREITs. The backstop is buybacks, which I expect to be a focus during the reporting season in August. Most AREITs having ample capacity to fund a share repurchase and on my numbers those stocks trading below NTA, led by Vicinity (VCX), Investa Office (IOF), would find ~2% EPS accretion by undertaking a 5% buyback. Pricing has reached a point where three sell-side firms have lifted their recommendations on retail landlords to buy. They might not have their timing correct but the valuations do look enticing.

The AREIT sector is presently paying a 5.3% distribution yield with dividend growth of 4.0% expected in FY18, thus providing a forecast total return of around 9%. This compares to a cash rate of 1.5% and similarly modest offerings from cash management accounts. The sector benefits from low gearing, secure distributions and strong demand for institutional grade real estate from sovereign and pension funds. As mentioned buybacks will support pricing and if that fails, then expect more M&A.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Pat Barrett has twenty five years experience in the listed and direct property industries, most recently covering property securities, infrastructure and utilities analysis at UBS.

2 stocks mentioned

Pat Barrett

UBS Asset Management

Pat Barrett has twenty five years experience in the listed and direct property industries, most recently covering property securities, infrastructure and utilities analysis at UBS.

Expertise

Pat Barrett

UBS Asset Management

Pat Barrett has twenty five years experience in the listed and direct property industries, most recently covering property securities, infrastructure and utilities analysis at UBS.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management