Leading brands at good value

Remaining true to our core value management style has seen the fund invest in a variety of well run, high quality and attractively priced companies. We keep an eye on all quality stocks, even those we’ve previously divested; after all, you never know when a company’s valuation will fail to reflect its earnings capacity, growth potential or a significant change in the competitor landscape.

One such example is Whirlpool (NYSE:WHR), the world’s leading manufacturer of major home appliances with the number one or two market position in key regions. It owns a portfolio of well-known brands including Whirlpool, Kitchen Aid and Maytag, and invests substantial research and development (R&D) to develop innovative appliances connected to smart technology such as Google Nest and Amazon.

As past shareholders and visitors to Whirlpool’s Michigan headquarters, we know the company well. We recently identified an opportunity to buy back into the stock at a very cheap valuation. The stock was trading on a forward earnings multiple of less than 7x, below its global peers Haier and Electrolux, and well below its long-term historical average of 11x.

This discount is partially due to integration issues they have experienced following the acquisition of Indesit, a substantial player in the European white goods market, issues we believe to be temporary. In December we had a one-on-one conversation with the CEO to focus on the strategic plan for Europe, which includes restructuring, rebuilding retail volume and asset sales. Market sentiment has been weak due to its exposure to the North American housing market, however analysis of historical earnings suggests the business isn’t as cyclical as people fear – earnings fell 30% during 2008 before rebounding the following year.

In its home market, Whirlpool brands occupy a 30% market share position and are well known by consumers for quality and American-based manufacturing. In a market challenged by inflationary conditions (tariffs, raw material and transport inflation), it operates at a relative cost advantage; this enables industry-leading operating margins of 12%, almost double those of its peers.

They generate significant free cash flow at 3-5% of sales per annum, and we expect the business to deliver ~US$600 million in 2018. The company has a long history of generous buybacks and dividend payments, and this year, cash flow will be further supported by some non-core asset sales. It’s most unusual for such a strongly branded goods manufacturer to trade at such a low earnings multiple and we are happy to be once again be shareholders of this leading brand.

A new opportunity presents

As a manager that looks for long-term investment potential, we often find ourselves watching particular stocks for a number of years before we become investors. A classic example is Nintendo (7974:JP), a company we’ve followed for some years, including several visits to Nintendo HQ in Kyoto; this is the first time we’ve believed there’s a sound investment opportunity.

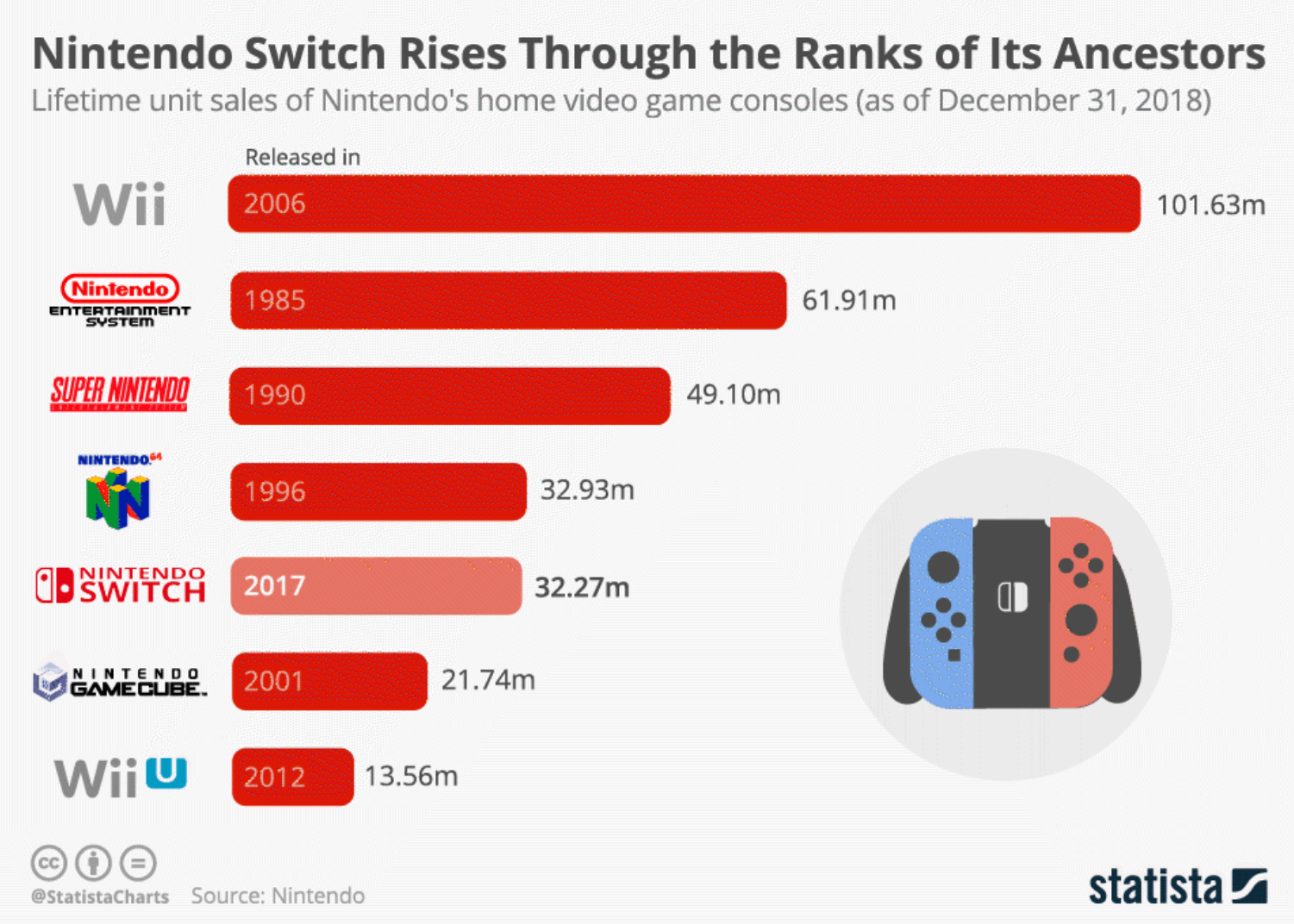

Nintendo has had mixed results with its past game console launches. The Wii launched in November 2006 and was a remarkable success, selling over 100 million units over its lifetime. Its successor, the Wii U which launched in November 2012, was a commercial failure, selling just over 13 million units. The key question for the market has been whether its latest console – the Switch, launched in March 2017 – looks more like the Wii or more like the Wii U?

Figure one: Lifetime Nintendo game console sales

According to Statista, in the first nine months of Nintendo’s financial year, which ends 31 March, they sold 14.49 million units of the Switch. It’s now aiming to sell at least 17 million by the end of March.

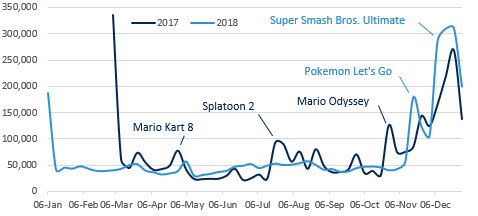

Sales increased toward the end of 2018 with the release of platform-exclusive games; after all, nobody buys a console in isolation, you always buy it with a particular game in mind. The release of Super Mario Party (5.3 million units), Pokémon: Let’s Go, Pikachu! (10 million units) and Super Smash Bos Ultimate (12.08 million units) helped them achieve total software sales of more than 50 million units for the three months ending 31 December 2018.

Weekly retail data from Japan further illustrates this point – Switch hardware sales were weak earlier in the year due to a lack of game launches, but broke records in November and December with the launch of these games (figure two).

Figure two: Nintendo switch unit sales in Japan by week (Kadokawa)

Source: Citi, Dengeki online

With a strong line-up of games in 2019, we believe the Switch’s momentum will continue to build; this will drive double digit earnings growth for several years. This is not being priced into the stock.

We’re also attracted to the optionality in the stock – beyond strong Switch sales, they could surprise from its continued expansion into mobile, its potential entry into China, and from better monetisation of its IP through movies and theme parks – Nintendo World is expected to open in Tokyo in time for the 2020 Summer Olympics.

Perpetual’s team has been researching Nintendo’s games with their kids over the summer holidays. Their conclusion is that the unique functionality of the console is a winner. It’s portable like a game boy, with the benefits of the motion sensors of a Wii and the ability to play like a traditional console. Mario Odyssey and Mario Kart Deluxe are proving popular; the team looks forward to some strong software sales in 2019!

Never miss an update

Stay up to date with the latest news from Perpetual by hitting the 'follow' button below and you'll be notified every time I post a wire.

Want to learn more about Perpetual's Global Fund? Hit the 'contact' button to get in touch with us.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Garry is an experienced global investor, managing global equities portfolios at Profeta Investments and Perpetual Investments for over twenty years. He is the founder of Profeta Investments.

Profeta Investments is a global asset management firm focused on delivering high absolute returns. We focus on investing in quality businesses through different phases of their maturity. We manage a high conviction portfolio taking a long term view. We focus on growing companies with strong balance sheets where management teams are aligned with shareholders. For more information visit www.profetainvest.com

Garry is an experienced global investor, managing global equities portfolios at Profeta Investments and Perpetual Investments for over twenty years. He is the founder of Profeta Investments. Profeta Investments is a global asset management firm...

Expertise

Garry is an experienced global investor, managing global equities portfolios at Profeta Investments and Perpetual Investments for over twenty years. He is the founder of Profeta Investments. Profeta Investments is a global asset management firm...

Expertise

Comments

Comments

Sign In or Join Free to comment