TOL - 17th Dec, 2020

Learning from the market

Amit Lodha

Fidelity International

Friedrich Nietzsche told us, ‘The future influences the present just as much as the past.’ Events that haven’t happened yet have a great influence upon the world we see today. When it comes to current market valuations, Nietzsche’s contention looks compelling.

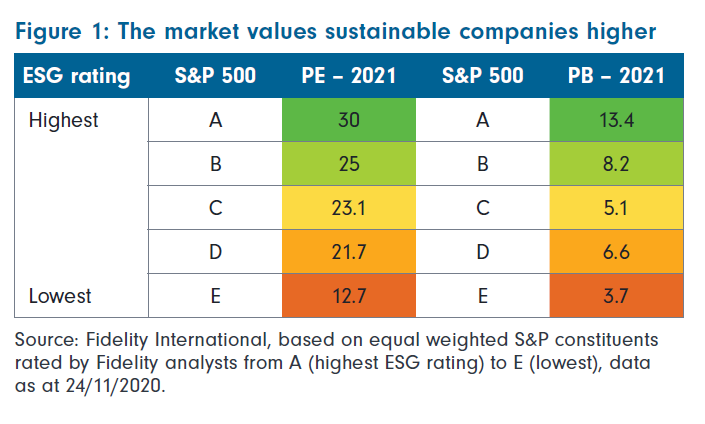

We broke down the S&P 500 using Fidelity’s proprietary ESG ratings (A–E) and measured the price-to-earnings and price-to-book of companies within each rating bracket. This revealed an incredibly linear relationship between companies with a positive ESG rating and their valuation multiples.

As ESG ratings improve from E to A, companies are demonstrating sounder sustainability practices. In the process, the market lowers its cost of capital (applies a greater multiple to the valuation). This is the essence of ESG investing – applying qualitative factors to an assessment of a company or, in other words, counting what cannot be counted. The result is a relationship between high ESG ratings and low cost of capital (high multiples) with near-perfect symmetry. To unpick this connection is to understand what effect the future has on us today, and Nietzsche’s words start to ring true.

What does price tell us?

A market in its truest form is a place for buyers and sellers to come together – it could be a village farmers’ market or the US stock market. When a buyer and seller agree to trade, the information we can use as investors is included in the price of that agreement. If a multiple is applied to the market price, this tells us what the buyer expects to receive in future earnings.

Take Tesla and Moderna as examples: both are trading on lofty multiples of near-term earnings. This is the market’s way of telling us we need more renewable transport and a coronavirus vaccine. Similarly, Figure 1 is evidence of a forward-looking market that is indicating the world is better off with more of these well-run, sustainable companies. We need more As and fewer Es, and price acts as the carrot and stick to help us get there. The future is casting an influence on the present.

As investors, we should be aware of what multiples signal about the world’s current and future demands. In addition, we should understand when industry structures can change. In 2002, Blackberry and Nokia traded at high multiples and largely deserved those valuations. Today, even the most die-hard value investors wouldn’t expect them to return to those levels. Active management is about combining a view of valuations with the possibility of wider sector change.

Purpose-led growth

In a world of uncertainty and volatility, the desire for value investing and picking winners comes to the fore. The multiple of a company is inversely related to its cost of capital and, for value investors, there are returns to be made where multiples are low and the cost of capital is high. At this point, we need to be vigilant and ask ourselves what the price is implying about the company. If a low multiple is a signpost that the world could be better off without this company, then we need a compelling reason why the world is wrong to justify investing.

The energy sector demonstrates the extent that the market view can change. Historically, energy has been a medium cost of capital industry with the consensus that we need more of it. The need to rapidly decarbonise and the threat of global warming has reversed that sentiment, particularly in the oil and gas industry where there is a high cost of capital and low multiples – a consensus we need less of it.

A low multiple can look an attractive short-term opportunity for value investors, and this is when I remind myself that you rent value, whereas you invest in growth. Investors can exploit companies on low multiples for a bargain and move on once the valuation rises. But I look for companies that will sustainably grow. If my investment thesis is intact, I will continue holding while remaining watchful of new competitors that a lower cost of capital always attracts; for example, the recent flood of newly launched electric vehicle start-ups and Tesla clones. Even when holding for long periods, our process ensures we re-evaluate the thesis continuously.

As we move into the recovery phase of the pandemic with an economic slowdown looming large, I’d argue for those companies that are priced at higher multiples for good reasons. This is not value investing, nor is it growth investing. I’d describe it as purpose-led investing – the market is inviting more of what the world needs.

Knowing when to listen

Often the market is correct, and the multiple will reflect the current and future value that a company offers. But sometimes the market gets it wrong.

When we invested in Recruit Holdings* during its 2014 IPO, it was trading at a low multiple and its crown jewel business, Indeed, was loss-making. The company had a quality management team, growing earnings, and a disciplined approach to capital allocation that meant they were using their opportunities to sustain and grow cash flows at high incremental returns on investment. We felt the market underestimated the management team’s ability to create value. Six years later, while the market has corrected much of the earlier mis-valuation, the potential for long-term compounding remains higher than ever – in an economy of rising unemployment, solutions that match job seekers and employers are essential.

Whether a company is on a high or low multiple, our job as investors is to be right in either scenario. We seek to invest in good companies that can get better, or in good companies misunderstood by the market as bad. Ultimately, we must be confident in a company’s ability to create value in a future society through constant innovation and improvement.

For some, growth investing is about growth for growth’s sake and value investing about cheapness only. But I believe growth should be on a sustainable basis. This means combining valuation with the fundamentals, management quality, market opportunity and the long-term needs of the world around us. We continue to employ this integrated process in the Fidelity Global Equities Fund, so that we can both listen to what the market is telling us and know when to ignore it.

The market is always there to teach us, and if we treat it as a temple of learning, we will learn. But if we search for a quick buck and use the market like a casino, then the experience will be like a casino: the house always wins.

Never miss an insight

Stay up to date with our latest thought pieces by hitting the follow button below and you'll be notified every time I publish a wire.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Amit Lodha has been Portfolio Manager of the Fidelity Global Equities Fund since 2010 and has over 16 years of investment experience. He is a qualified accountant from the Institute of Chartered Accountants (India) and a CFA charterholder.

3 topics

Amit Lodha

Portfolio Manager, Global Equities

Fidelity International

Amit Lodha has been Portfolio Manager of the Fidelity Global Equities Fund since 2010 and has over 16 years of investment experience. He is a qualified accountant from the Institute of Chartered Accountants (India) and a CFA charterholder.

Expertise

Amit Lodha

Portfolio Manager, Global Equities

Fidelity International

Amit Lodha has been Portfolio Manager of the Fidelity Global Equities Fund since 2010 and has over 16 years of investment experience. He is a qualified accountant from the Institute of Chartered Accountants (India) and a CFA charterholder.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management