Most stocks underperform, and why this is an argument for conservative active management

While equity index returns over time broadly match a normal distribution, returns from individual stocks are highly positively skewed. Skewness increases with the length of holding period - held for a decade two-thirds of stocks underperform the index. Search for the extreme winners? Our conclusion – avoid the losers.

The “normal” distribution is a reasonably good fit for actual equity market returns, as measured by an index. The distribution of outcomes is symmetrical. This means positive and negative outcomes of the same magnitude are equally like to occur. Where the normal distribution is imperfect is in the tails – extremely large positive and negative index outcomes happen far more frequently than the model would suggest.

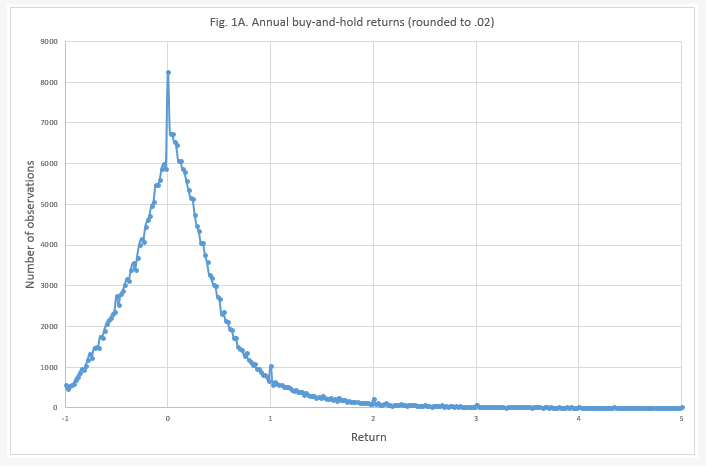

The distribution of individual stock returns is not normally distributed. In fact, the distribution is highly skewed.

Source: Hendrik Bessembinder, "Do Stocks Outperform Treasury Bill?", Journal of Financial Economics, May 2018 draft. US equity data over 1926-2006.

Source: Hendrik Bessembinder, "Do Stocks Outperform Treasury Bill?", Journal of Financial Economics, May 2018 draft. US equity data over 1926-2006.

This means that the outcome of the average stock, as measured by the median, is far less than the index return. Hendrik Bessembinder from Arizona State University has done some wonderfully insightful work on this topic. Using data for the entire US equity market over the 90-year period from 1926 to 2016 he shows that the median annual buy-and-hold return is 5.2% pa, dramatically short of the mean return of 14.7%. 55.6% of stocks underperform the index over a year. If you think that being a patient investor takes care of this problem, think again. Skewness increases with time. Assuming they are held for a decade, 64% of stocks underperform the index.

The fat tails and asymmetry in individual stock returns raises interesting questions, which we’re not here to answer, about equity risk premia when valuing stocks, and how to think about and measure risk. Remember, the standard deviation measure assumes the distribution of outcomes is normal. It is not.

Interestingly, skewness is far greater for small stocks. For the smallest decile of stocks only 42% generate return above zero over a decade compared to 81% for the largest decile.

Also notable from Bessembinder’s work is the superior returns from unlevered non-financial firms. The average annual buy-and-hold return for all non-financial firms without leverage was 27.2%, almost double the 14.7% pa return for the index.

Some commentators have concluded that skewness is an argument for indexing – if two-thirds of stocks underperform over an index the odds are stacked against you, so just buy the index. Others conclude that this is an argument for a strategy that tries to identify the outsized winners, the outliers at the extreme positive end of the skewed distribution.

A third point of view, and the one we endorse, is to a follow a conservative approach that focuses on avoiding the extreme losers, the fat negative tail of the distribution. Fortunately, these firms share some common characteristics – they tend to be highly financially leveraged, have poor returns on invested capital, have balance sheets that have grown aggressively, and trade on very high earnings multiples. Avoiding stocks like this will help you stay out of the “disaster zone” and go a long way to generating outperformance.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Stephen has been investing in global markets for over 30 years, making him one of Australia’s most experienced international investors.

He is the Founder and Chief Investment Officer of Aoris Investment Management, an independent, Sydney-based firm dedicated to a single strategy: a highly selective global equity portfolio.

Since its inception in March 2018 through to the end of April 2025, the Aoris strategy has ranked in the top 5% over 3 years, 5 years, and since inception, relative to a broad peer group of international equity funds (Morningstar). The firm currently manages just under $2 billion in assets.

Prior to founding Aoris in 2017, Stephen was Head of International Equities at Evans & Partners.

Stephen has been investing in global markets for over 30 years, making him one of Australia’s most experienced international investors. He is the Founder and Chief Investment Officer of Aoris Investment Management, an independent, Sydney-based...

Expertise

Stephen has been investing in global markets for over 30 years, making him one of Australia’s most experienced international investors. He is the Founder and Chief Investment Officer of Aoris Investment Management, an independent, Sydney-based...

Expertise

Comments

Comments

Sign In or Join Free to comment