Not having cash can be costly, but so can sitting on it - how not to make that mistake

As I reflect on the financial year just gone past it goes without saying that navigating markets through the challenges of COVID has certainly been an experience.

This is very much a once in a cycle event in that share prices have crashed and then recovered a large portion of their losses very quickly. For us, we’ve had good victories through managing our cash position very actively and shorting companies that we thought were going to be heavily impacted by the disruption caused by COVID-19.

But there was also a big lesson that I’m sure many investors can connect with right now. Do you back yourself to act and put money in the market or risk missing the boat by waiting around for certainty? I share my thoughts on that, along with insights on how we managed our portfolio and one of the stocks we’re most excited about right now in an investor update I did with our partner Winston Capital.

How did you manage your cash position through the year?

For background, we're a bottom-up fundamental manager. Everything we do is about the stock and its outlook. Top-down does come into it a little bit at the extremes, and it's been one of those times where we've certainly had an extreme event.

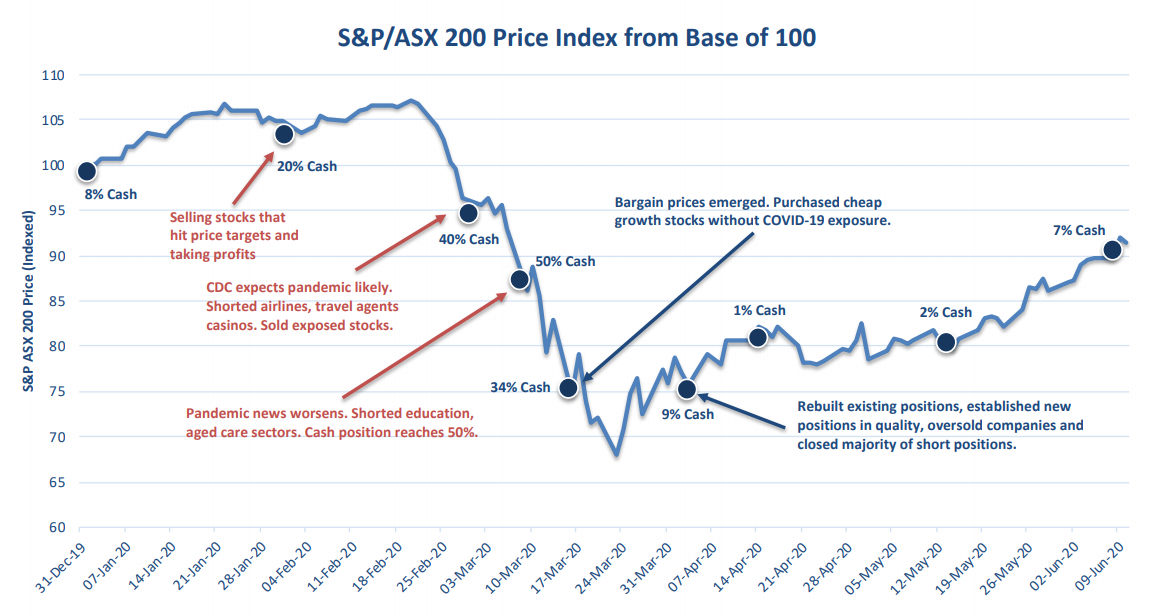

As we started the calendar year, our cash weighting was moving towards 20% by the end of January. As we started to sell some stock as the market had been pretty good. This chart shows the movements in our cash quite nicely. The blue line is the ASX 200, and it was rising. As you can see, it went up from a base of a hundred. And then it started to fall away as COVID came.

Click to enlarge

Normally, we wouldn't take any reaction at a stock level for something that's extraneous going on like that, unless we really thought it was going to affect the stock price. This was clearly a big thing that looked like it was really going to affect stock prices, but just like everybody else in the world that was looking at it, we couldn't really tell how bad it was going to be.

However, we were able to use some of the skills that we use in judging what companies say about how they're going, to read between the lines of what the World Health Organisation and the Centre for Disease Control in the United States were saying.

The moment that CDC said: "The risk assessment is low, but a global pandemic is likely, in which case our risk assessment would change", that was the trigger. We've seen that sort of behaviour in companies all the time. We knew where that was going and that led to us selling. And you can see how our cash level increased after that as we were selling stocks and shorting stocks.

Can you share what you did on the short side of the portfolio?

We shorted airlines, we shorted travel companies, and as it went on, we also shorted aged care, childcare stocks, and eventually then started to buy when prices were low enough.

In a sense, we actually had a pretty good experience through the whole COVID disaster, from the point of view of selling fairly early, not everything but enough. And then having plenty of cash to buy back into it. Even as stocks were still falling, they just looked absolutely like bargains. And since that time, the market's recovered quite strongly and we have been net sellers over time, as you can see from that chart.

You've made a lot of changes. Have you got a particular stock that excites you, and why?

A stock that's only gone into the portfolio more recently, as a result of COVID, has been Kathmandu (ASX:KMD). They are a bricks and mortar seller of adventure wear, clothes, boots, but also some adventure accessories like packs and so forth. But the real money's in the clothes and the vests and the jackets.

Now the interesting thing is they only had about 10% sales through online channels before COVID. That's really been accelerating now because of people being at home and not being able to get to the shops in the first instance. Also, more particularly, most of their sales are in Australia. People are at home and winter's been pretty cold this year, which means people are going to be wanting to buy more jackets. And then finally people haven't been at the office and they need more casual clothes.

You put all those things together and we're expecting very strong sales out of Kathmandu. We have seen some evidence of that. The company gave an update to talk about that about a month ago now. Those things don't happen in isolation.

We're expecting an absolute cracker result from Kathmandu in the coming reporting season.

Can you tell us about any stocks or sectors that haven't excited you?

Well, it was a bit of a shorter's field day. Aside from the obvious ones like Qantas and Flight Centre, we tried to short some stocks that had supply chains into and out of China, early on, and then more towards the end, it was more about those things where people congregated.

Aged care was obviously one where people were not wanting to send their relatives and so it was getting hit, and also all those extra expenses around protecting people from COVID. Childcare, likewise, people not sending their child, and also because they're at home, not wanting to send their child to those facilities.

As the pandemic went on, though, some of those stocks actually got to such a level that they became attractive and we closed those positions out. And in fact, then we started to buy. We ended up having a positive position in Qantas (ASX:QAN). We had a positive position in Webjet (ASX:WEB) at one point. They were both companies we made money out of. However, they were relatively short-term trades. There was only so much money to be made there with relative confidence. We didn't want to push it because, obviously, they are long-term challenged industries.

What's the key lesson that you've learnt from the current pandemic crisis?

I think there are lots of lessons that have been reinforced to us. One of the key things when we set this business up, is we wanted to give ourselves the flexibility in our mandate, if you like, that allowed us to react, in a commonsense way, to things that were going on around the world. I'll point out two things on that note:

- There's active and there's active - It's one thing to say you're being active, but if your cash weight can't be less than 5% at any point, because you always have to be fully invested for your clients, you are not really very active. It's all together another thing when you are an absolute return fund manager and can make a call about whether you want to be invested in the market or not. As long as we've got rigorous ways of assessing that, that's proved to work really, really well in extreme situations. So that's been a lesson. It's been a test and it does work.

- Waiting around for certainty - There's also having the confidence to realise that when you see something going on and you've got an insight, act on it. Don't wait. If you wait, yeah there's more certainty. You can always do with a bit more information, but if you wait, it'll play out and you will have missed your chance.

Now, we had a great insight into what was going on in COVID because the form of words used that we could identify that was really common, to the way people try to protect their careers and manage expectations in periods where they don't have full control over what they're allowed to say.

That was a great parallel insight we could have and we were able to act on that. So when it became a global pandemic, that gave health departments and politicians around the world a trigger to act, and boy, did the markets overreact.

Benefit at every stage of a cycle

Monash Investors Limited invest in a small number of compelling stocks that offer considerable upside and short expensive stocks that are at risk of falling. Want to learn more? Hit the 'contact' button to get in touch or visit their website for further information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Simon has over 30 years experience as an analyst and fund manager. He co-founded Monash Investors in 2012 - a long/short Australian equity manager with an absolute return focus.

........

This presentation has been prepared by Monash Investors Pty Limited ABN 67 153 180 333, AFSL 417 201 (“Monash Investors”) as authorised representatives of Winston Capital Partners Pty Ltd ABN 29 159 382 813, AFSL 469 556 (“Winston Capital”) for the provision of general financial product advice in relation to the Monash Absolute Investment Company Limited (“MA1) and the Monash Absolute Investment Fund ARSN 606 855 501 (“Fund”). Monash Investors is the investment manager of MA1 and the Fund and is for information purposes only.

The Trust Company (RE Services) Limited ABN 45 003 278 831, AFSL 235 150 (“Perpetual”) is responsible entity of, and issuer of units in, the Fund. The inception date of the Fund is 2nd July 2012.

The information provided in this document is general information only and does not constitute investment or other advice. The content of this document does not constitute an offer or solicitation to subscribe for units in MA1 or the Fund or an offer to buy or sell any financial product. Accordingly, reliance should not be placed on this document as the basis for making an investment, financial or other decision. This information does not take into account your investment objectives, particular needs or financial situation. Monash Investors, Winston Capital and Perpetual do not accept liability for any inaccurate, incomplete or omitted information of any kind or any losses caused by using this information.

Any investment decision in connection with the Fund should only be made based on the information contained in the disclosure document for the Fund. A product disclosure statement (“PDS”) issued by Perpetual dated 12 September 2017 is available for the Fund. You should obtain and consider the PDS for the Fund before deciding whether to acquire, or continue to hold, an interest in the Fund. Initial Applications for units in the Fund can only be made pursuant to the application form attached to the PDS.

Performance figures assume reinvestment of income. Past performance is not a reliable indicator of future performance. Comparisons are provided for information purposes only and are not a direct comparison against benchmarks or indices that have the same characteristics as the Fund.

Monash Investors, Winston Capital and Perpetual do not guarantee repayment of capital or any particular rate of return from the Fund and do not give any representation or warranty as to the reliability, completeness or accuracy of the information contained in this document. All opinions and estimates included in this document constitute judgments of Monash Investors as at the date of this document are subject to change without notice. Perpetual is not responsible for this document.

3 topics

4 stocks mentioned

1 contributor mentioned

Simon has over 30 years experience as an analyst and fund manager. He co-founded Monash Investors in 2012 - a long/short Australian equity manager with an absolute return focus.

Expertise

Simon has over 30 years experience as an analyst and fund manager. He co-founded Monash Investors in 2012 - a long/short Australian equity manager with an absolute return focus.

Expertise

Comments

Comments

Sign In or Join Free to comment