November Review: Equities ok, but Credit and Commodities get Crunched

November was mildly positive for equities with small gains in the US (0.1%) and China (0.9%), European (2.6%) and Japanese (3.5%) indices posted healthy gains leaving Australia (-1.4%) the odd one out. The action was once again in credit and commodities with high yields spreads blowing out again whilst investment grade fell somewhat less. Price falls in commodities were fierce with the Bloomberg commodity index down 7.2%, US oil dropping 10.2%, copper off 11.5%, US natural gas retreated 3.9% and iron ore fell 13.5%. Gold continued to decline this month by 6.7%, with the short term fears of US interest rate increases outweighing the long term fears that sovereign nations will continue to devalue their currencies by printing money.

In commodities the evidence of oversupply was apparent in several markets, and not just by the price movements. For oil, articles noted that storage tanks are nearly full and that tankers are stuck waiting near import terminals as there is limited remaining capacity to handle the oversupply. If global storage capacity is exhausted, then a free falling price is possible until production is dramatically scaled back. It’s a similar story for iron ore with one large steel producer putting the heavies on their suppliers for urgent price cuts of 10%, lifting to 30% over time. In the face of falling demand for steel the supply of iron ore is still ramping up. The Roy Hill mine is due to ship its first load in December and Vale’s S11D mine is ahead of schedule and below budget.

With all of the damage in commodity prices it is no surprise that the Baltic Dry index, which tracks the cost of shipping commodities, is at all-time lows. Containers shipping rates have also plunged with the Asia to Northern Europe route seeing a drop of 70% in three weeks. There is an excess of ships making the historical comparisons somewhat tricky, but it is still remarkable that record lows are being hit now when the seasonal lull for shipping is after Christmas.

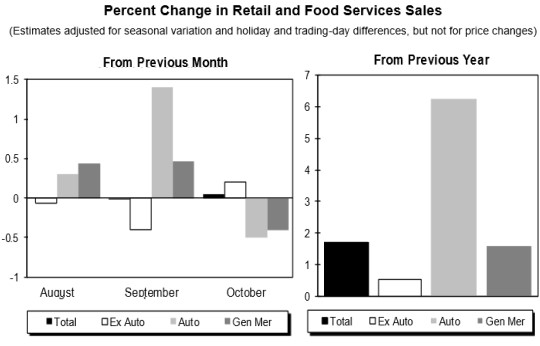

In the US retail sales are showing weakness with a number of highly indebted retailers now hoping for a Christmas miracle after weak black Friday sales. Retailers have responded to sluggish sales since August by starting Christmas sales early and cutting orders for new stock. Even Apple is cutting back component orders from its suppliers, signalling that iPhone sales aren’t hitting expectations. The graphs below show the break-up of retail sales with autos the clear outperformer and the ex-auto numbers ugly. The surge in outstanding US auto finance, particularly in the subprime segment, has inflated auto sales. Should the auto credit bubble pop, the last leg propping up US retail sales will be removed. In Australia retailers Dick Smith, Myer and Woolworths are struggling, with a weak economy and bad management common amongst all three.

Source: Wolf Street

In China the money chasing debt investments has shifted from bank loans and wealth management products to the bond market. The possibility of a credit bubble was highlighted this month by articles noting that 45% of new debt is used to pay interest on existing debt, most interest on existing debt is being accrued and not paid from cashflows, and that extend and pretend lending is keeping steel mills alive whilst they are massively unprofitable. One expert suggested that 300 million tons of excess steel production capacity should be bulldozed. Chinese aluminium and nickel producers have requested that their government buy up surplus metals in order to support prices, just as they have with equities where it is estimated that the government now owns 6% of stocks.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

1 topic

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management