NZ equity returns for the next decade?

The New Zealand Equity Market had a stellar 2019, up over 30%, so we revisited our NZ equity return estimates to see how the outlook might have changed.

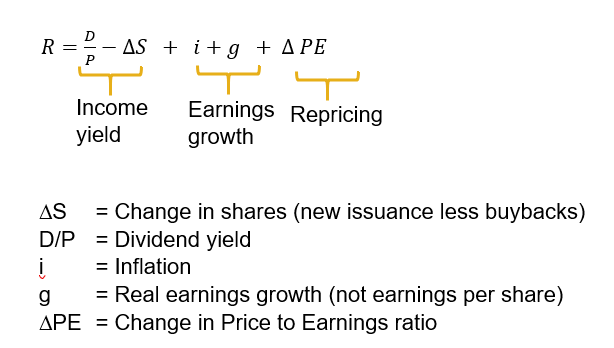

We use the Grinold and Kroner model to break down future returns based on the following equation:

Our return estimates below are “real” returns, the net return after inflation. If you would like a nominal return (including inflation) simply add on your desired inflation number.

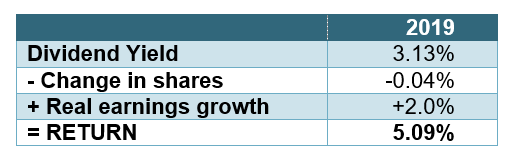

Since last year, the dividend yield of the New Zealand Equity Market has fallen to 3.1%. Real earnings growth and share capital assumptions are pretty much unchanged.

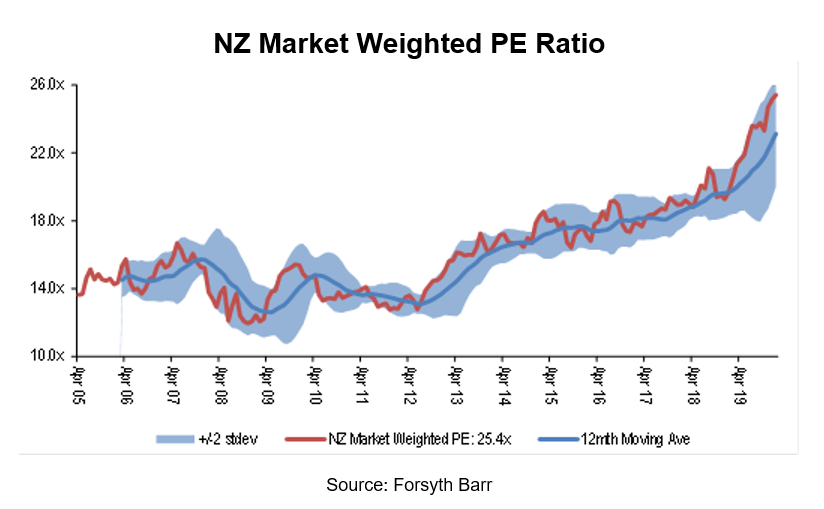

The biggest change is due to the strong performance of the equity market, which has stretched the forward PE ratio for NZX index to 25.4x. This may be a record for the local market. The average since 2005 is 16.2 and if you had data for much longer period it would likely be a bit lower still.

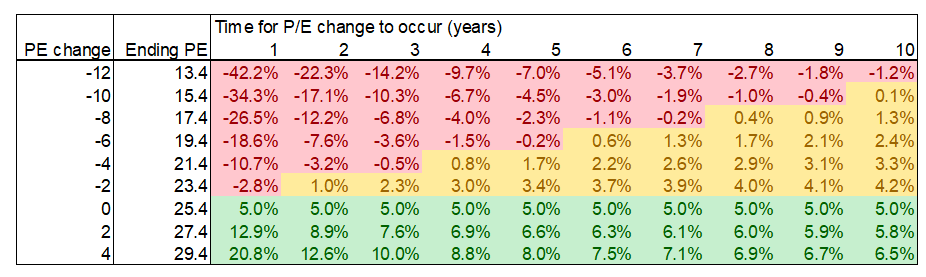

The following table allows the reader to pick an ending PE ratio and a timeframe for the change to occur to get the annual real return over that period. For example, if you think the PE ratio will drop by 8 points to 17.4 (still above the long-term average) over 7 years you get annual real return of -0.2%.

The shaded red real returns are less than 0%. Yellow is between 0% and 5%. Green is a real return above 5% per annum.

This is not to say we can’t have another strong year in 2020 for NZ equities, but each additional year of above normal returns makes any return to a more “normalised” PE more painful.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

........

Castle Point has taken all reasonable care in the preparation of these articles, however accepts no responsibility for any errors or omissions contained within. Past performance is not necessarily an indication of future performance. Opinions expressed in these articles are our view as at the date of issue and may change

3 topics

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

Expertise

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management