One high quality small cap we like

Livewire reached out to us on the topic of small caps, specifically the outlook, what our strategic approach is in current market conditions, and what opportunities we are seeing today.

Q: What market conditions would small caps need to resume their previous outperformance, and what are your expectations here?

We have learnt over the years that predicting market conditions is a precarious task, and that stock fundamentals will ultimately provide the best long-term guide to performance. Sentiment towards small caps over the past five months has certainly been impacted in part by the large number of companies that have failed to meet expectations and/or had significant operational issues. When we look at a broad spectrum of ASX listed smaller companies we believe only a small portion are very well positioned to out-perform long term by virtue of excellent management teams, robust business models, market tailwinds and low market understanding/expectations. This group of high quality smaller companies represents less than 5% of the smaller companies’ universe in our opinion.

The main condition necessary for a resumption of a general smaller companies’ bull market is an increase in general market risk appetite, which could in part be driven by strong earnings growth from smaller companies. However, at a macro level we note that a weakening AUD has until recently provided a multi-year tailwind for many smaller companies which have been growing internationally. A strengthening AUD will continue to place pressure on the earnings of smaller companies which rely upon offshore growth.

Looking forward, we believe the broader smaller companies market backdrop is likely to remain similar to the past few months since there are many smaller companies currently on high valuation multiples despite having largely unproven business models and uncertain earnings outlooks.

Q: What are some of the ‘red flags’ you use to avoid small caps susceptible to a sudden de-rating?

We are long-term investors so we aim to look through all market noise and to only focus upon the fundamentals. As a result, we only have two main red flags we look out for.

Firstly, a change in business fundamentals such as a change in management or the loss of a previously sustainable competitive advantage are red flags for us which may lead us to change our view on a stock.

Secondly, as value investors, a company’s valuation will always factor into our view on a stock. When market valuations and expectations are high the greater is the prospect of a de-rating if a company fails to meet these lofty expectations. DMX Capital Partners’ portfolio generally comprises stocks trading at only 8 to 12 times FY17 earnings, so stock expectations are generally low across the fund. If one of our stocks were to trade on a significantly higher valuation which left no margin for error, we may change our view. Across the broader ASX smaller companies’ universe we are currently seeing many stocks on valuations which are unsustainably high in our opinion, and we’ll be avoiding these stocks as a result.

Can you identify a small cap opportunity you like today, and explain why it presents a good opportunity?

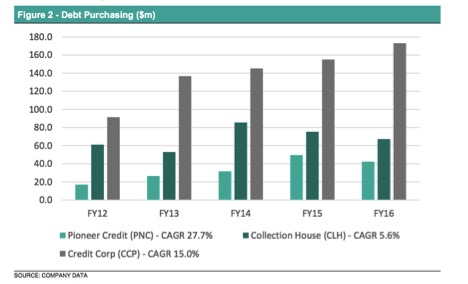

Pioneer Credit (ASX:PNC) is a high conviction DMX Capital Partners portfolio holding worth highlighting.

With a 10% market share Pioneer is the smallest of the ASX listed debt purchasers, after Credit Corp (ASX:CCP) and Collection House (ASX:CLH). The company purchases debt ledgers, often for less than 20c in the dollar, from other financial institutions. The company’s objective is to recover these debts at a significantly higher rate than they purchased them for, thus generating a profit in the process.

Our conviction in PNC is high because the stock meets our two main investment criteria:

High quality: We view the company as high quality with a solid and aligned management team, a well-defined growth strategy, a strong balance sheet and shareholder friendly dividend policies.

Significantly under-valued: PNC has provided guidance for its FY17 profit of at least $10.5m which puts the stock on a PE of just 9.5x FY17 earnings – a large discount to its two listed peers, CCP and CLH. We believe the combination of having a low profile in the investment community, trading on a low earnings multiple, and having a growing earnings profile offers substantial valuation upside.

We look forward to continued earnings growth and share price appreciation in the years ahead.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

DMX Asset Management Limited is an investment manager focussing on nano and micro-cap value opportunities on the ASX.

3 stocks mentioned

DMX Asset Management Limited is an investment manager focussing on nano and micro-cap value opportunities on the ASX.

Expertise

DMX Asset Management Limited is an investment manager focussing on nano and micro-cap value opportunities on the ASX.

Expertise

Comments

Comments

Sign In or Join Free to comment