Our approach to maintaining durable income

The new environment of zero rates and higher credit market volatility calls for a new approach to durable income investing—one that can go anywhere, but remains anchored in bottom-up conviction.

When the yield on risk-free assets is close to or even below zero, investors tend to resort to old habits to maintain income. The first is to take more liquidity risk, earning a premium to own securities that seldom trade. The second is to deploy substantial leverage to boost their expected risk and return. And the third is simply to take more credit risk—chasing yield in the junkier parts of the market and hoping for the best.

For a number of reasons, these three approaches are especially problematic in the current environment. Instead, we advocate a fourth approach to maintaining durable income: flexibility to go anywhere in the global credit markets, informed by a relative value assessment of the best risk-adjusted return potential, underpinned by high-conviction, fundamental credit selection.

The turn away from Treasuries

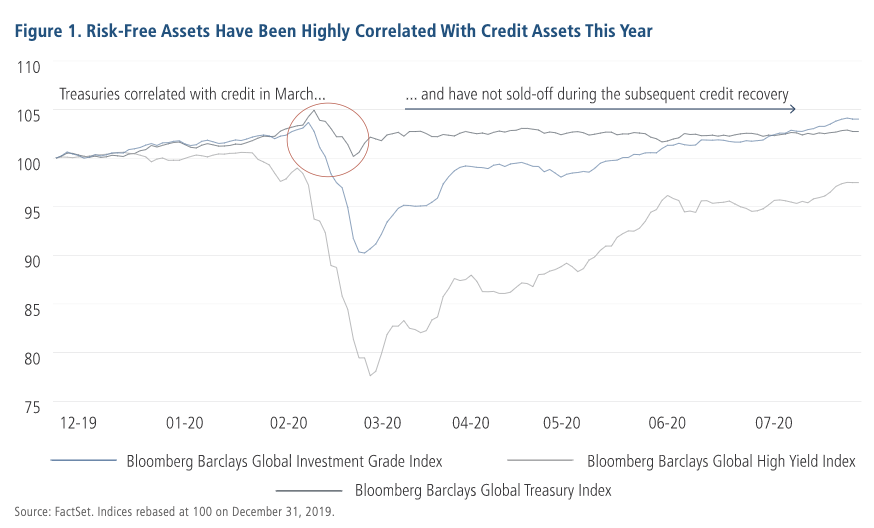

Over the past 10 years, it has become increasingly difficult to rely solely or substantially on core government bonds for durable income. The onset of the COVID-19 crisis has only compounded the problem. Furthermore, even the argument for holding government bonds for diversification is now much harder to sustain: price upside has become limited as yields have approached zero, which has diminished the potential for risk-free assets to generate returns that are negatively correlated with credit returns during periods of risk aversion.

During March this year, a liquidity crunch in Treasury markets led to a yield spike that correlated with the downside in risky assets. Since then, however, risk-free yields have dropped back close to record lows and stayed there, despite a strong recovery in credit markets (figure 1). That means no cushion has been built back in to enable them to act as a diversifier during the next bout of risk aversion.

As a result, while Treasuries still have a role to play for most investors, many have been turning more decisively to credit for their return-seeking and income-generating bond portfolios.

The usual solutions: giving up liquidity, adding leverage or chasing yield

But even in credit markets, for some years now tightening spreads have led to a stretch for illiquid assets, leveraged exposure and more and more credit risk.

Of the three, we at Neuberger Berman generally have most sympathy with adding illiquidity risk. We do not think that investors should hold illiquid securities in a simple race for yield, but we do think there are attractive opportunities in private debt and the less liquid parts of loan and structured credit markets. This can only be part of the answer to low market yields, however—and it is not an answer at all for investors that are allowed to invest only in liquid credit markets.

Adding leverage via credit derivatives, particularly in investment grade, has been another way to counter low yields and tight spreads. We think leverage is a useful tool for making marginal adjustments to risk exposures, with a view to maintaining balanced portfolios. We are skeptical about leaning heavily on it to boost returns or income, however, particularly now that yields have come so low. It is not uncommon to see diversified credit portfolios applying leverage of 400 – 600% in the current environment. That implies a lot of risk—and we would also argue that it is quite an inefficient way to get credit exposure. Leveraging credit default swap indices can work well when the market is not differentiating much between one credit and another, but now that the COVID-19 crisis has turned the cycle over, investors have become more discerning.

What about taking more credit risk? Can investors maintain income by holding lower-rated high yield bonds?

Back in March, at the height of the COVID-19 panic, high yield markets were pricing in a cumulative projected default rate in excess of 30%. Since then, the willingness of capital markets to provide businesses with liquidity to get them through the crisis, and unprecedented monetary and fiscal policy support, have warranted the lowering of our cumulative default outlooks for 2020 – 21.

Nonetheless, it’s clear we are no longer in the pre-crisis environment in which central banks supported a slow-but-steady economic expansion where the high yield default never seemed to climb above 2%. Not everyone is going to get to the other side of COVID-19 unscathed, companies are taking on more debt, and while central banks have stepped in, they are primarily focused on higher-quality credits.

An alternative: flexibility, relative value and dynamic allocations

We think that a reasonable alternative approach might have the following three objectives:

- Maintaining a target yield commensurate with a current, conservative high yield allocation

- Maintaining portfolio volatility commensurate with an investment grade allocation

- Investing within cheap sectors of the market when the opportunity arises, while managing the potential downside risk of individual market sectors

To achieve these three objectives, we believe it is important to have the flexibility to “go anywhere” in credit markets. Given market events and the general turn of the credit cycle, the best risk-adjusted yields can be available in any sector, and the best portfolio-level, risk-adjusted yield can be available in any blend of sectors.

To take the most obvious recent example, in April and May this year, a high single-digit income and total return profile was possible even in an investment grade-only portfolio. At that time, AA rated issuers were coming to market to shore up their balance sheets with long-dated borrowing: 30-year bonds with 15 years’ credit duration that would normally trade with a 100-basis-point spread were selling at 200 basis points over Treasuries—from that starting point, a gradual return to normal spreads would generate a double-digit return even before coupons were factored in.

For us, that means a flexible credit portfolio for durable income would have wide ranges of potential allocations to the five main credit sectors: between 10% and 80% in global investment grade credit; between 10% and 80% in global high yield bonds or loans; up to 30% in emerging markets, mainly investment grade hard-currency sovereign and corporate bonds; up to 30% in securitised credit, such as asset-backed securities (ABS), credit risk transfers (CRTs) and collateralised loan obligations (CLOs). The flexibility can also extend to geography (with perhaps up to 50% in non-U.S. markets), as well as duration and curve positioning.

In our view, taking advantage of this flexibility requires two things:

- The first is a genuinely “apples-to-apples” framework for comparing credit risk pricing across different sectors, regions and rating bands. As an asset manager with many years of multi-sector credit experience, Neuberger Berman has developed a tried-and-tested methodology for doing just that.

- The second, particularly now that macroeconomic uncertainty is exceptionally high and credit market liquidity is fragmented following banking-system reforms, is a dynamic approach to allocation.

In April 2020, a flexible strategy such as the one described above would likely have been meaningfully tilted to investment grade credit, with perhaps 60% in this sector, 40% of which could have been concentrated in high-rated, long-duration bonds—delivering spread duration as long as eight years or more. The remainder might have been shared 30% in high yield bonds and 5% each in emerging markets and securitised credit.

By July 2020, following rapid spread-tightening, it would likely have rotated meaningfully into BB rated high yield bonds and started adding ABS, particularly those eligible for the Federal Reserve’s new Term Asset Backed Securities Loan Facility (TALF).

When conditions call for a more aggressive asset allocation, we could see this flexible strategy investing 40% or more in B rated credit as part of its full 70 – 80% allocation to non-investment grade, and the full 25 – 30% in emerging markets. This would still allow it to hold 20 – 25% of its assets in investment grade, diversified across corporate bonds, emerging markets, hybrids, structured credit and loans.

Conclusion: A new approach to durable income investing

In summary, we believe the transition from low rates, tight spreads and low volatility to an environment of even lower rates but much higher credit market volatility calls for a new approach to durable income investing. This new approach focuses on credit, and prioritises both flexibility and bottom-up fundamentals.

The focus on credit is necessary to generate the total returns that income investors are used to and require. The flexibility to “go anywhere” in credit markets enables investors to seek out the most attractive risk-adjusted income and yield, through the cycle and during the periods of market stress and dislocation that can be unusually rich in opportunity. And the emphasis on fundamental analysis can help to prevent flexibility from turning into uncontrolled “bets” on the outlook for credit, strike a balance between quality and yield in the portfolio, and provide the basis upon which “apples-to-apples” relative value assessments can be made.

With these guidelines, we believe it is possible to generate through-cycle returns comparable to those of high yield or emerging markets debt, but with investment grade levels of volatility.

A client-led partnership

As a private, independent, employee-owned investment manager, Neuberger Berman is structurally aligned with the long-term interests of our clients. Click 'FOLLOW' below for more of our insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Adam Grotzinger, CFA, Managing Director, joined the firm in 2015. Adam is a Senior Fixed Income Portfolio Manager based in Chicago. Prior to joining Neuberger Berman, Adam worked in the Fixed Income teams at Franklin Templeton in Singapore, London and California. Adam graduated cum laude from the University of Vermont with a BS in International Business and a minor in Political Science. He is a Chartered Financial Analyst (CFA) Charterholder and member of the Chicago CFA society.

........

This material is provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Information is obtained from sources deemed reliable, but there is no representation or warranty as to its accuracy, completeness or reliability. All information is current as of the date of this material and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole. Neuberger Berman products and services may not be available in all jurisdictions or to all client types. Investing entails risks, including possible loss of principal. Investments in hedge funds and private equity are speculative and involve a higher degree of risk than more traditional investments. Investments in hedge funds and private equity are intended for sophisticated investors only. Indexes are unmanaged and are not available for direct investment. Past performance is no guarantee of future results.

Firm data, including employee and assets under management figures, reflect collective data for the various affiliated investment advisers that are subsidiaries of Neuberger Berman Group LLC (the “firm”). Firm history and timelines include the history and business expansions of all firm subsidiaries, including predecessor entities and acquisition entities. Investment professionals referenced include portfolio managers, research analysts/associates, traders, and product specialists and team-dedicated economists/strategists.

This material is being issued on a limited basis through various global subsidiaries and affiliates of Neuberger Berman Group LLC. Please visit www.nb.com/disclosure-global-communications for the specific entities and jurisdictional limitations and restrictions.

The “Neuberger Berman” name and logo are registered service marks of Neuberger Berman Group LLC.

Adam Grotzinger, CFA, Managing Director, joined the firm in 2015. Adam is a Senior Fixed Income Portfolio Manager based in Chicago. Prior to joining Neuberger Berman, Adam worked in the Fixed Income teams at Franklin Templeton in Singapore, London...

Expertise

Adam Grotzinger, CFA, Managing Director, joined the firm in 2015. Adam is a Senior Fixed Income Portfolio Manager based in Chicago. Prior to joining Neuberger Berman, Adam worked in the Fixed Income teams at Franklin Templeton in Singapore, London...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management