Playing Russian roulette with oil prices

Prior to the OPEC’s meeting with Russia on 6 March 2020, hopes were high that the endorsement of the proposed deeper production cuts of 1.5mbpd, on top of the ~2mbpd cuts already in place, would simply be a fait accompli. However, Russia’s decision not to participate and Saudi Arabia’s decision to open the spigot and offer massive discounts on its production sent shocks through commodity and equity markets globally. What should have been an agreement to offset the (hopefully) short-term impacts on oil demand from the COVID-19 outbreak has seen an effective 3.5mbpd surplus added to the market. This is a high-stakes game of brinkmanship between powerful oil nations, with very little certainty as to how it will play out and the timeframe when we may see a resolution.

How did we get here?

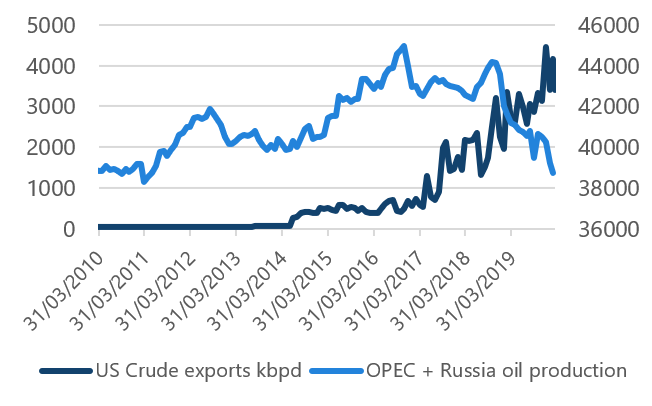

Historically, OPEC’s role was to coordinate and unify petroleum policies of its Member Countries to ensure the stabilisation of oil markets and provide income stability for member producers. Given its position as the world’s second largest exporter (next to Saudi Arabia), in 2016 Russia was brought on board to provide further clout to the organisation. This was after failing to join in cuts in 2014, which led to the last oil price collapse. Russia continues to be a participant in OPEC+, which has provided price stability for the world’s producers. During the same period, US production growth surged, particularly from its unconventional shale basins, which has allowed the US to become energy self-sufficient and a net exporter of crude and petroleum products.

One could argue this energy independence was gained at the cost of, or at least with the assistance of, OPEC+ market share and revenues. In our view, it appears Russia’s decision not to participate in further cuts is at least, in part, aimed at ensuring the US producers share the role of delivering market balance. When combined with a number of high profile Russian individuals and entities being the subject of a number of US sanctions, Russia’s actions could also be designed to gain some political leverage to push for a lifting of sanctions.

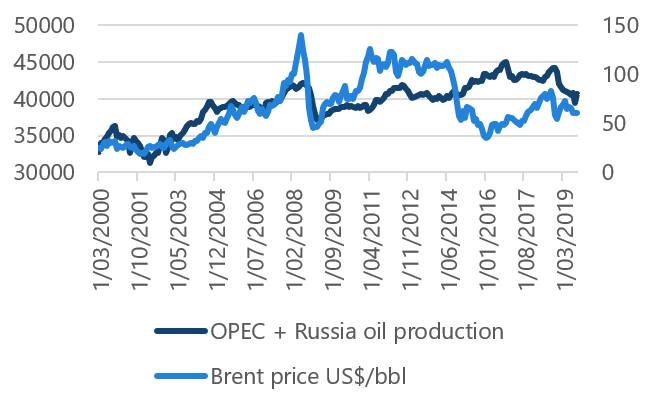

Chart 1 - OPEC+ production vs oil price

Chart 2 - OPEC+ production vs US oil exports

Source: Bloomberg, Nikko AM

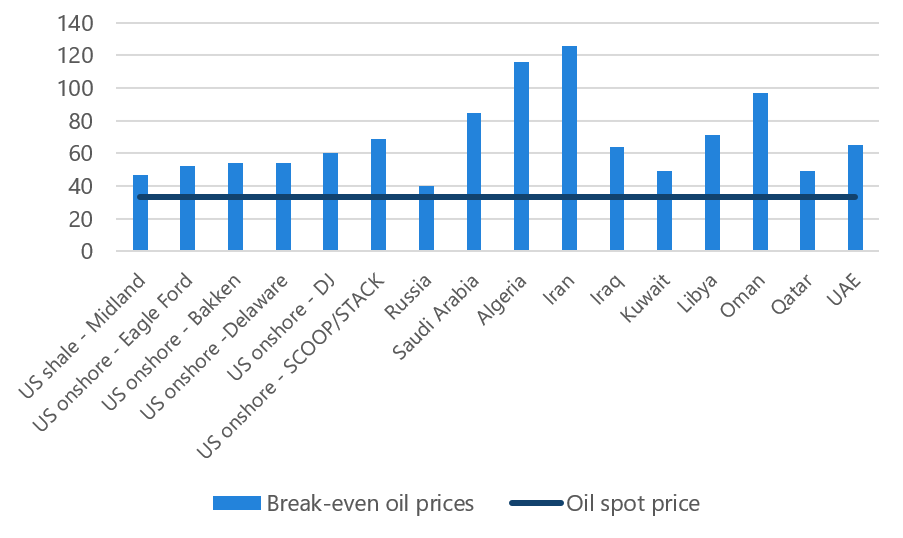

From a high level, and without fully understanding the minutiae of modern geopolitics, one could understand Russia’s goals here. What is more difficult to understand is Saudi Arabia’s aggressive intention to reverse OPEC’s set course and lift production. Saudi Arabia, and indeed many of its OPEC partners, requires significantly higher oil prices to ensure balanced budgets (fiscal break-evens) than Russia. While Russia is likely to be uncomfortable at current oil prices, with a fiscal break-even of $40 – 50/bbl, the Saudi’s could be burning through over US$120bn/yr (~15% of GDP) of its reserves given the IMF estimates its fiscal break-even is in excess of US$80/bbl. The US shale break-even varies between oil fields, but within the Permian — the source of much of recent growth — it is around US$45/bbl (Midland) to US$50/bbl (Delaware).

Chart 3 - Break-even oil prices vs SPOT

Source: Bloomberg, IMF, Nikko AM

It is very difficult to know how the current situation will play out, but we do see three possible near-term scenarios:

- OPEC+ reconvenes and agrees to maintain the previous level of cuts. This could ease the current fear of significant oversupply, with renewed confidence that at least 2mbpd would stay out of the market during the uncertain period of COVID-19 induced demand weakness. No doubt the broader market would remain skeptical of compliance and closely monitor OPEC+ output.

- OPEC+ reconvenes and agrees to the extended cuts. In our view, this is an optimistic scenario in light of current circumstances. We doubt Russia’s intent was to see oil fall to current levels, but rather avoid artificial oil price strength given US shale growth was set to slow over 2020. A number of broker analysts suggest 2020 exit growth rates could be around 0.6 to 1mbpd vs the 1.2mbpd growth seen over 2019. Note: this was before the collapse in oil.

- Russia and Saudi Arabia follow through on threats to lift production. Under this scenario, we believe oil prices would remain under significant pressure for an extended period of time and that it’s likely we would see a material reduction in output from the US — either voluntarily or through bankruptcy. The US onshore oil industry has US$40bn in debt falling due in 2020, and $200bn over the next four years. Macquarie Research estimates that at US$35/bbl Brent, the US onshore rig count would fall from ~700 to 300. This would result in zero growth from US onshore, which should reduce global supply by around 0.6-1mbpd; offsetting a substantial portion of the predicted 1.5mbpd demand lost due to COVID-19.

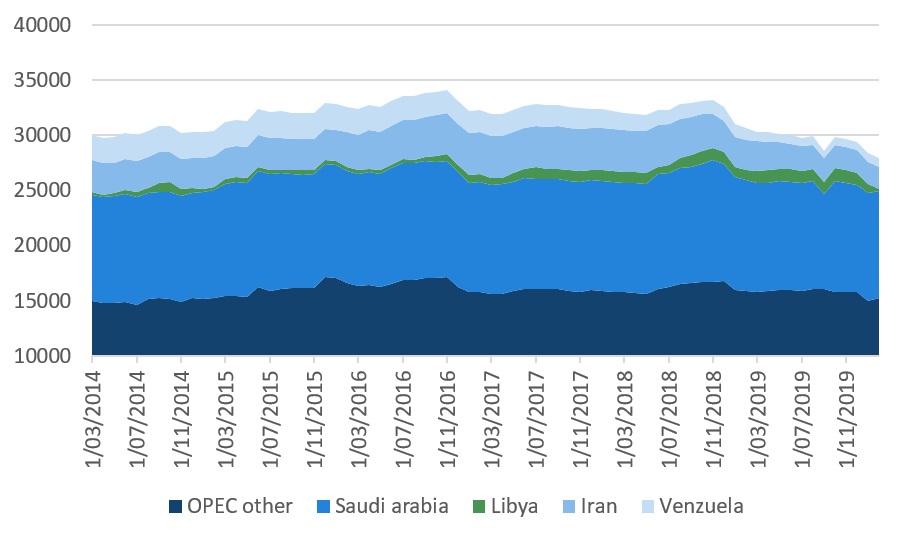

While the supply/demand situation currently looks dire, we should still be cognisant that Libya and Iran are both constrained to the tune of ~3mbpd with no clear path to resuming normal exports — a fact that appears to have been lost given the attention on the larger OPEC+ players.

Chart 4 - OPEC production

Source: Bloomberg

Over the long-term, we believe there are a number of factors to warrant higher oil prices:

1. Global decline rates ex-US shale have stabilised at ~5%, but the growing contribution of unconventional volumes to the world’s oil mix will likely see aggregate decline rates move higher if investment in shale is muted, and existing shale production is allowed to decline without replacement.

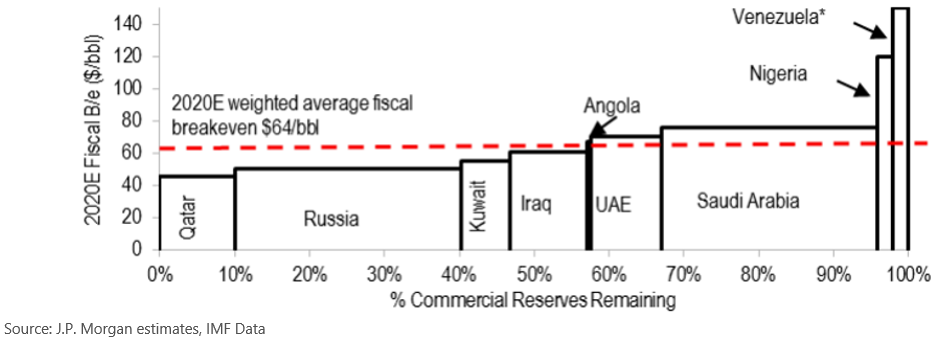

2. OPEC fiscal breakevens imply an average US$64/bbl, as shown in Chart 5. Clearly Saudi Arabia, along with Nigeria and Venezuela, are the swing producers, and while the Saudis are clearly not behaving in this fashion at present, over the long-term the country may need to return to its market stabilisation policies to remain profitable.

Chart 5 - Updated 2020 fiscal breakevens for selected OPEC+ members – 2020E weighted average $64/bbl vs spot Brent at c$55/bbl

Source: J.P. Morgan estimates, IMF Data

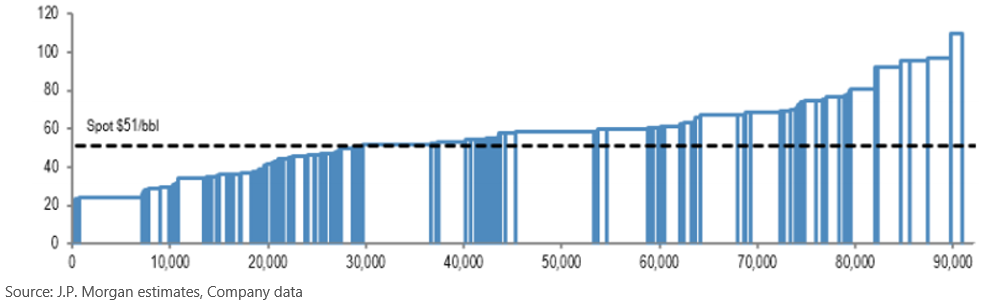

3. New projects need higher prices to warrant investment: at spot prices almost all new projects assessed by J.P. Morgan are out of the money. Prices of ~US$60/bbl are needed to bring 50% of these projects on line to replace decline.

Chart 6 - Global projects cost curve (15% IRR): ~50% projects breakeven on the current strip

Source: J.P. Morgan estimates, Company data

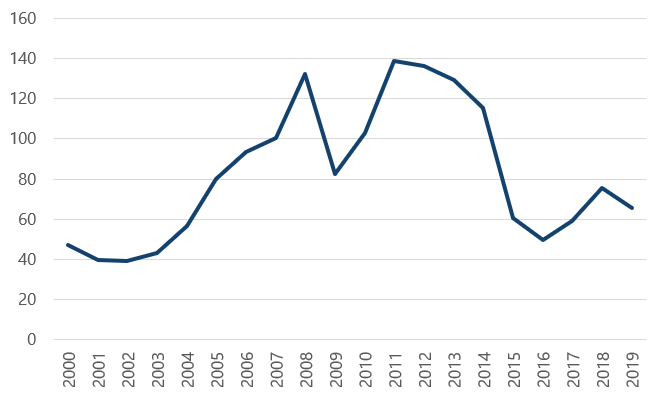

4. While economic conditions have changed over this time period, it’s worth noting the oil price has averaged ~US$82/bbl in 2020 real terms over the past 20 years.

Chart 7 - 2020 real oil price

Source: Bloomberg, MST Marquee

Conclusion

The collapse of the agreements by OPEC+ has placed us in a situation very few had expected. Prior to the events of the week commencing 2 March, broker consensus was that oil prices were roughly flat at US$60/bbl over the medium term. Our investment time horizon is more long-term in nature, but for comfort we frequently review balance sheet strength under a number of downside scenarios to ensure there are ample buffers to protect against periods of commodity price weakness.

The largest decline in oil price since the 1991 Gulf War has caught us, and the market, by surprise. Oil Search is the most levered of the larger oil names, and has therefore seen the brunt of the market’s selling pressure. We believe the balance sheet risks can be managed in the near-term. The market is heavily discounting the value of its share of the foundation PNG LNG project, and ascribing no value whatsoever to expansion opportunities.

The market appears to have entered a period of panic selling, but we expect to see a number of value opportunities arise in the aftermath. As Warren Buffet once said, “Be greedy when others are fearful.”

Written by Brad Potter and Stefan Hansen

Learn more

Click the 'follow' button below to be the first to read our latest value investing insights, including where we are finding the most compelling opportunities on the ASX.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Brad joined the business in 2002. He has 28 years’ experience primarily in the funds management and stockbroking industry, and has overall responsibility for managing the Australian equities team, process and portfolios. Prior to joining, Brad was Director, Corporate Finance with Westpac, a Senior Resource Analyst with Ord Minnett and in his early career, a geologist working with a number of resource companies. Brad has portfolio management responsibilities for the Tyndall Australian Share Wholesale Fund and Tyndall CVA Plus Strategy. He has analyst responsibilities for Banks.

1 stock mentioned

Tyndall AM

Brad joined the business in 2002. He has 28 years’ experience primarily in the funds management and stockbroking industry, and has overall responsibility for managing the Australian equities team, process and portfolios. Prior to joining, Brad was...

Expertise

Tyndall AM

Brad joined the business in 2002. He has 28 years’ experience primarily in the funds management and stockbroking industry, and has overall responsibility for managing the Australian equities team, process and portfolios. Prior to joining, Brad was...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets