Positioning for a recovery

Anthony Doyle

Firetrail Investments

Global investment markets are currently grappling with the far-reaching ramifications of Covid-19. Unsurprisingly, capital markets have been volatile, reflecting the uncertainty that surrounds the outlook for households and businesses. Governments have been quick to stimulate their economies, while central banks have taken unprecedented actions to prevent the current recession from turning into a depression. Volatility, uncertainty, and unprecedented are the words that will define 2020 in investors’ minds.

Given the nature of the current crisis, it is useful to remind ourselves of some of the lessons from the past. This is important when constructing and positioning a diversified portfolio of assets, a challenge that most financial advisers face daily. Reminding ourselves of the fundamentals of portfolio construction can help investors position portfolios appropriately in times of crisis and volatility.

Exploit a long-run time horizon

Investors with a long-horizon do not need short-term liquidity, giving them an edge during market sell-offs. As markets fall, long-run investors have often generated excellent returns by buying quality distressed assets across major asset classes.

Additionally, if the market rewards illiquid assets with a higher risk premium, it makes sense that investors over-allocate to such assets, as it is unlikely that they will need to sell during bouts of market volatility. Pockets of traditional asset classes like corporate bonds, small-cap equity, and emerging market equity offer the opportunity for long-run investors to generate superior returns over time.

Whilst many would like to describe themselves as long-term investors, this time horizon can shorten very quickly. During financial and economic turmoil, both institutional and individual investment horizons tend to shorten due to immediate cash flow needs or because of psychological factors. The last thing that any investor wants to do is sell an asset into a volatile an illiquid market, where bid-offer spreads can widen materially, and asset prices can fall well below fair value.

The free lunch

Diversification is the rare free lunch available for all investors: it can reduce portfolio volatility without reducing its return. A key challenge to achieving diversification is reducing the dominance of equity risk in a balanced portfolio. Even if diversification tends to fail in crises (as correlations spike across asset classes), it can still be useful in the long run. This matters more for long-run investors who face less liquidation pressure during market drawdowns.

Most portfolios have positive exposures to the equity market and to economic growth. This directional risk is difficult to diversify away, making those assets with a negative correlation to equities a valuable addition. Despite yields being at all-time lows, cash and high-quality government bonds and gold can play an important role to play in most portfolios.

Diversification of course has limitations, one of which is the tendency for correlations to approach one during crises. Many good fund managers distinguish themselves by managing downside risk instead of just relying on diversification. A strong risk management framework and avoidance of large drawdowns is key in generating good long-run compounded returns.

Risk-free is return-free

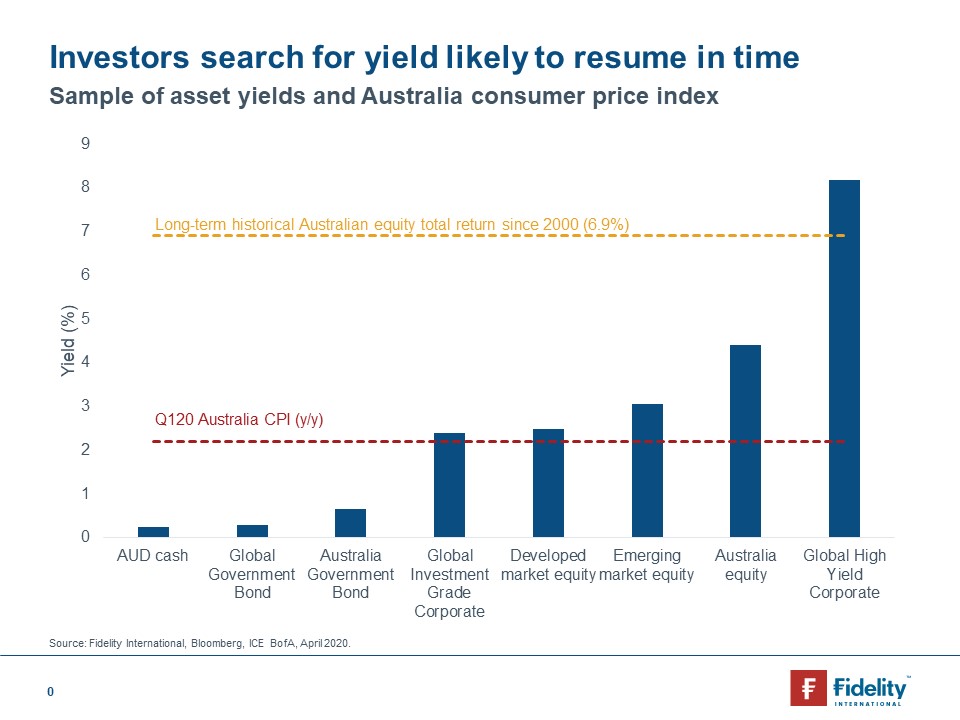

Developed market central banks have taken the actions that they have with a defined monetary policy transmission mechanism in mind. One of the channels of monetary policy is the asset prices and wealth channel, with lower interest rates and quantitative easing expected to spur demand for higher risk assets. Risk-free assets like cash and government bonds no longer generate a positive inflation-adjusted yield and are return-free. Long-run investors can position for “the portfolio rebalancing effect” that is likely to dominate investment flows in the next decade.

Expected portfolio returns can be improved by increasing the weight of the most volatile asset class. The classic approach is to raise the weight of “high-risk, high-return” equities and reduce the weight of “low-risk, low-return” assets such as cash and government bonds. Taking more risk in this way, and getting rewarded for it, is an easy way to boost long-run returns for investors.

Minimising costs can come at a cost

Passive investing minimises trading costs. However, some costs are worth paying. For example, buying an equity index fund costs more than investing in a bank deposit, but the equity risk premium should make the cost worthwhile in the long-run. In general, investors should allocate more to active products the less they believe in market efficiency. Minimising costs is not always smart; being cost-effective and avoiding wasteful expense is.

The importance of being selective

Market outperformance - through the compounding of returns - can help investors increase their ability to achieve their financial goals. Excess returns can be an important driver of wealth creation, and actively managed funds offer the opportunity to outperform the market. Even seemingly small amounts of excess return can lead to significantly better outcomes.

Over the intermediate term, asset performance is often driven largely by cyclical factors tied to the state of the economy, such as corporate earnings, interest rates, and inflation. The business cycle, which encompasses the cyclical fluctuations in an economy over many months or a few years, can therefore be a critical determinant of market returns. In the current environment, investors are placing a premium on less economically sensitive sectors like consumer staples, healthcare and utilities.

Many discretionary sectors such as hotels, cruise lines, airlines, restaurants have shut down almost completely. Many of these companies have a big fixed cost base and are priced as at risk of default. However, not all are the same and some will have enough liquidity, no imminent debt calls and experienced management teams. These will be able to survive and possibly thrive after this crisis, which will see at least a part of the competition eliminated.

Once the dust settles, companies that can survive the current crisis and are oversold, will recover sharply. The road ahead is unlikely to be smooth, but long-term investors can embrace the volatility and look for new opportunities that arise from it, while continuing to ask themselves whether the companies in which they invest have the right characteristics to endure this difficult period. Active investing, combined with rigorous bottom-up research, can help to identify those companies that will be winners in the long-run.

As volatility looks set to continue in the coming weeks and months, protection in the form of safe-haven assets and portfolio diversification will be increasingly important for investors. Due to central bank action, riskier asset classes like equities appear likely to attract increasing inflows over the coming decade. The traditional methods of portfolio construction - a long-run horizon, diversification, cost-control, and active investing - remain the best approach to generating sustainable long-run returns.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

2 topics

Anthony Doyle

Firetrail Investments

Expertise

Anthony Doyle

Firetrail Investments

Expertise

Comments

Comments

Sign In or Join Free to comment