Praemium (PPS): Reviewing the playbook

Next Level: PPS is entering its next phase with a burgeoning Australian business and with an International business set to achieve its first profitable month in FY18. We believe the robust growth the company is seeing, the move to profitability in the international business and the likely inclusion in the ASX300 index over the year ahead as key catalyst to see the continued positive re-rating of the stock.

Following the December quarter update we’ve upgraded our Price Target by 10% to $1.10 per share, believing the move to independence by financial advisers will further benefit companies like Praemium with its tailored offering and SMA products.

Further, PPS has been evolving its offering with the additional of model portfolios on its SMA platform which attracts higher fee generation for the firm. These funds hit $822m at the end of December, providing a meaningful new revenue source.

Quarterly highlights

- Total platform gross flows of $764m, 35.0% ahead of BPe $565.8m;

- Australian SMA Platform gross flows of $548m ahead of BPe $415.8m;

- International Platform gross flows of $216m, ahead of BPe $150.0m; and

- Smartim FUM closed at $822m, 3.0% ahead of our $798.1m estimate

Earnings revisions

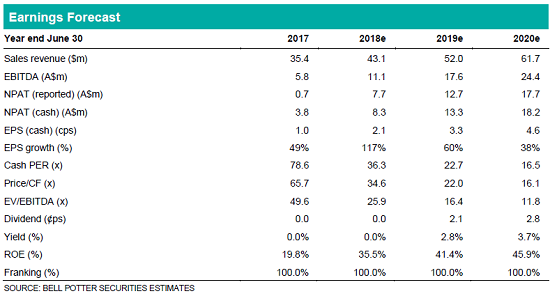

We have upgraded our estimates for underlying cash EPS by 0.5%, 5.8% and 6.6% in FY18, FY19, and FY20 respectively after the quarterly update. The earnings revisions are driven by the higher than expected closing FUA in the SMA platforms.

Following the changes we have upgrade our Price Target to $1.10 per share (previously $1.00 per share) and reiterate our Buy recommendation.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Bell Potter Securities is a leading Australian stockbroking, investment and financial advisory firm that provides a comprehensive offering of financial services to a diversified client base that includes individuals, institutions and corporations.

1 topic

1 stock mentioned

Stockbroker

Bell Potter Securities is a leading Australian stockbroking, investment and financial advisory firm that provides a comprehensive offering of financial services to a diversified client base that includes individuals, institutions and corporations.

Expertise

Stockbroker

Bell Potter Securities is a leading Australian stockbroking, investment and financial advisory firm that provides a comprehensive offering of financial services to a diversified client base that includes individuals, institutions and corporations.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management