Seeking value in unloved sectors

We are true long-term investors. We often identify our best investment opportunities in businesses that are out of favour. Typically these genuine opportunities are found within industries that are going through severe cyclical change. It is here that share prices will often be at their most volatile. Prime Media has a market cap of $115m, at a share price of $0.305. Stock is currently trading on a P/E of 4x with a grossed up yield of 16% whilst only 35% of earnings are distributed to shareholders. Notwithstanding the headwinds, our view is that this represents value.

Being contrarian value investors, we seek value in unloved sectors and businesses. One such sector is traditional or ‘old’ media. The headwinds impacting on this sector are well known, and are reflected in share prices. Prime Media (ASX:PRT) is an Australian company operating in the regional free-to-air TV market.

The majority of programming on PRIME7 and GWN7 is supplied through an affiliation agreement with the Seven Network. In 2013, the parties signed a long-term affiliation agreement extending to 30 June 2019.

The Seven network has developed a strong schedule of programs that includes major sports such as AFL, V8 Supercars and the Olympics (Summer & Winter). Additionally, local content includes “Sunday Night”, “House Rules”, “Home and Away” and “My Kitchen Rules”. Prime has a solid competitive position in the regional free to air TV market and is well placed to continue deriving its high revenue share by leveraging off the quality of Seven’s programming.

Interim Result 2017 Financial Year

• Total Revenue: $130.7 million (+4.9%)

• EBITDA: $31.2 million (+7.1%)

• Statutory Profit: $17.4 million (+7.2%)

• Audience share: 41.9% steady

• Ad Revenue: up 7.6% (versus mkt decline of 0.3%)

• Net Debt: $55.4 million,down from $65.6 million

• Earnings / share: 4.8 cents

• Interim Div: 1.7 cents per share fully franked

• Pay-out Ratio: 35%

• Forecast Yield: 16% grossed up

A recent trading update (26th April 2017) highlighted that PRT’s total advertising revenue has increased 4.2% for the financial year to 31 March, compared to the market decline of 1.9% - largely as a result of the August 2016 Rio Olympic Games coverage.

Headwinds

1. Advertising Cycle (incl. retail)

The advertising cycle is at a low-ebb generally. Retail constitutes about 40% of all ad spending, and discretionary retail is under significant pressure as witnessed by many high-profile discretionary retailers under administration or bankrupt. Additionally, the impact of Amazon could further weaken existing retailers and advertisers. Regional economies have not recovered to the extent of metropolitan areas since the GFC. Regional areas are exposed to mining and agriculture, which continue experience pressure. Unemployment in regional areas is higher than metro.

2. Advertising Platforms

The options available to advertisers are growing, and free-to-air TV now competes with the digitisations of outdoor billboards and endless online sites.

3. Competition for viewers

The advent of online streaming services such as Netflix has heightened concern that free-to-air is in structural decline.

Combine the perceived migration of advertising to online platforms along with a broadly subdued advertising market, and free-to-air appears to be in a perfect storm. Steve Hasker, the Global President of the International TV ratings agency, Nielsen, when in Australia was certainly not as negative on free-to air as the broader market. Mr Hasker stated “If you ask any media buyer on Madison Avenue what is going on in TV, they will say ‘oh, digital video – it’s growing fast, whereas TV ratings are coming down’.” But understanding viewing trends was complicated because some TV networks like CBS and ESPN in the US had actually lifted their ratings in recent years and primetime and live sport ratings for TV “had held up well”.

The improvements in TV technology make the viewing experience far more appealing than computer monitors and phones. In fact famous US investor, Mark Cubin, has been accumulating TV networks due to this superior viewer experience.

Media Reach Rules - Value in a takeover scenario

Malcolm Turnbull has again re-ignited the debate around the abolition of the media-reach-rules, that prohibit the metropolitan free-to-air networks (Nine, Seven and Ten) merging with regional affiliates by limiting audience reach to 75%. It is anticipated that such changes would lead to a restructuring of the industry and allow television networks, radio stations and newspapers to compete on equal footing with un-regulated digital entrants to the marketplace such as Google and Netflix. Prime chief executive officer Ian Audsley says “We don’t just have international media companies coming over the top of us we also have domestic players at a time when we are chained to the past and our ability to reorganise in the most effective economic manner is hamstrung by outdated regulations.” If implemented, the proposed changes would be good news for Prime Media and all of the regional players in the market.

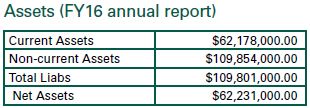

The old-fashioned ‘Benjamin Graham’ approach to uncovering value was to simply identify companies with current assets greater than total liabilities by the amount of the market cap. With increased company analysis this ‘arbitrage’ has narrowed, however, the following summary indicates value in the assets of PRT in a wind-up situation.

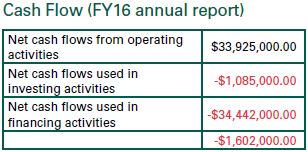

This cash-flow includes a dividend of $18,317,000. Net repayment of borrowings was $15,000,000. Net debt now stands at $55.4m, down from $65.6m at 30 June 16. Interest cover is a comfortable 17.8x.

We are true long-term investors. We often identify our best investment opportunities in businesses that are out of favour. Typically these genuine opportunities are found within industries that are going through severe cyclical change. It is here that share prices will often be at their most volatile. Prime are currently trading on a P/E of 4x with a grossed up yield of 16% whilst only 35% of earnings are distributed to shareholders. Notwithstanding the headwinds, our view is that this represents value.

Subscribe the our monthly newsletter here: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

1 topic

1 stock mentioned

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Comments

Comments

Sign In or Join Free to comment