Proceed with caution

The unprecedented pace of the financial market collapse and ensuing recovery has left investors questioning where the intrinsic value of risk assets really lies. While progress has been made in combating the COVID-19 pandemic and authorities have provided massive support for the economy and financial markets, we still cannot look at the pronounced rise in the S&P 500® Index since its March nadir and deduce that only sunny days are ahead.

Rather, to determine whether the recovery in asset prices is sustainable or is largely driven by transient factors, we need to apply other perspectives: what does history tell us about such rebounds? What hints do forward-looking indicators provide? And what are the conditions in the underlying economy that, ultimately, should dictate the value of equities and other asset classes.

When viewed through these lenses, the early-spring rally, in our view, appears tenuous.

Parallels to 2008

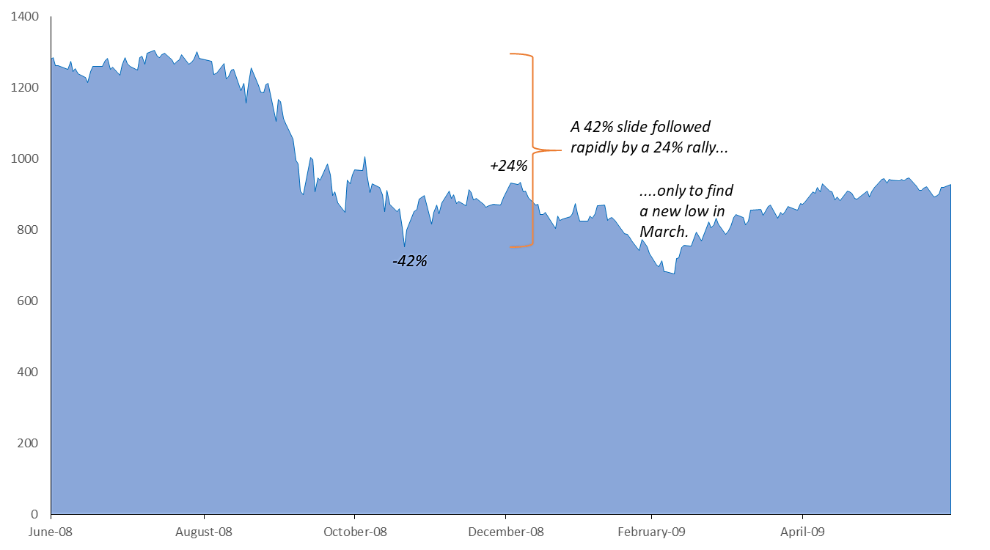

Short-lived bounces in stock prices even while markets establish new lows are not unheard of (see Exhibit 1). In late 2008, equities rallied in response to the US Federal Reserve’s (Fed) first round of quantitative easing and other programs aimed at supporting the economy. While investors welcomed these moves, it can be argued that some took their eye off the ball and did not fully grasp the harm being wrought on the real economy. Other parts of the market, however, tend to be relatively reliable forward indicators. At that time, two of these – corporate earnings revisions and options prices – continued to signal caution. Alas, as the magnitude of the housing crisis became apparent, the equities rally proved ephemeral and the market plunged to new lows in March 2019.

Exhibit 1: The S&P 500 rally in late 2008 proved short-lived

Source: Bloomberg, S&P 500 Index data from 30 June 2008 to 30 June 2009. Past performance is not a guide to future performance.

What is next?

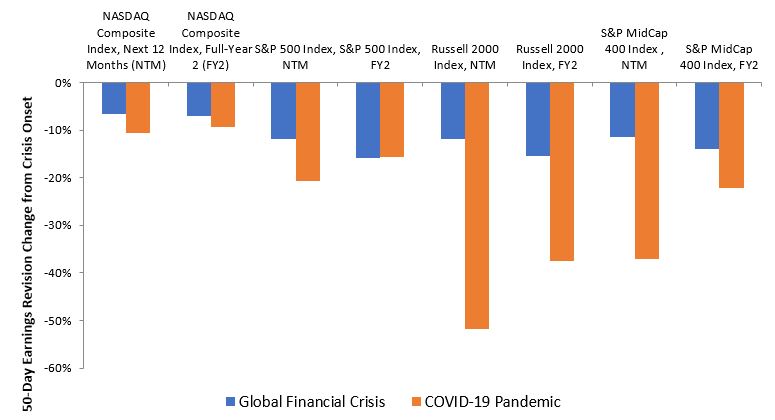

What do earnings revisions and options markets tell us now? Much like in 2008, they sound a more cautious tone than what is reflected in equity prices. Analysts’ earnings expectations can be powerful signals as they reflect the view of the experts who most closely follow individual companies and sectors. Since the beginning of the year, full-year 2020 earnings have been revised downward at a pace faster than during the depths of 2008 as analysts account for the near-shuttering of the global economy. It can be argued that the pandemic is a one-off crisis – implying it might be isolated to this year – but for the following year (in this case 2021) earnings revisions for major indices have been just as torrid as what was registered in 2008. This sends a dire message that the impact of the virus could have much longer-lasting consequences for the economy and corporate prospects.

Analyst consensus earnings revisions from 1 September 2008, preceding the Lehman bankruptcy, and from 1 March 2020, just before the global spread of the COVID-19 pandemic show the comparative impact of these recent crises (Exhibit 2).

Exhibit 2: Earnings revisions have been worse in 2020

Source: Bloomberg, as at 30 April 2020. Past performance is not a guide to future performance

Similarly, options markets see more downside than upside for riskier assets. As these instruments are often deployed by sophisticated investors to manage portfolio risk, the signals reflected in their relative bullishness and bearishness can provide hints on the direction of asset prices over the near- to mid-term.

The pivotal consumer

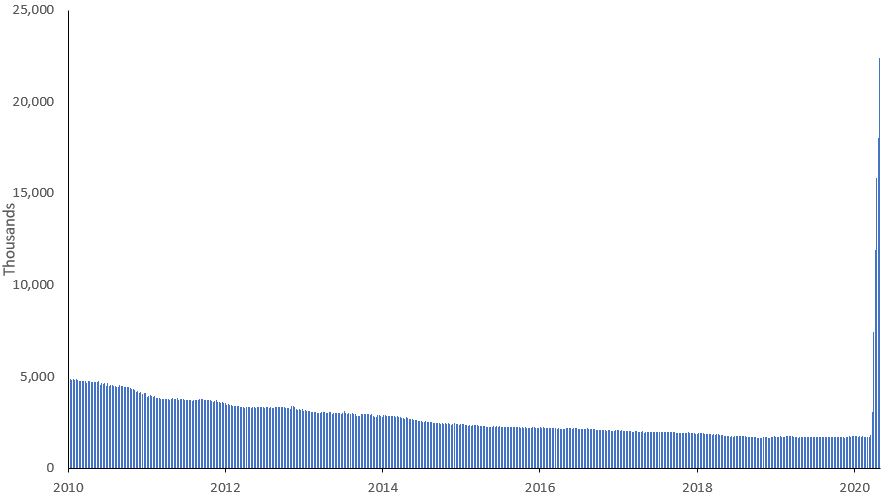

We believe that the prevailing economic conditions back up this wary view. What started as a public health crisis quickly morphed into a financial shock and now has become an economic crisis. Since late March, weekly initial jobless claims have averaged 4.8 million compared to 306,000 over the previous decade. Continuous claims stand at nearly 23 million. April’s change in nonfarm payrolls of a staggering 20.5 million was unlike anything experienced before (Exhibit 3).

Exhibit 3: Weekly continuous jobless claims have multiplied

Source: Bloomberg, as at 7 May 2020.

Not all of these lost positions will come back. This is especially true in industries such as retail, travel and hospitality that have been acutely affected by COVID-19. Many small businesses – a key source of employment – will disappear due to lack of liquidity. Individuals fortunate enough to remain employed, may seek to boost their savings after having had their finances severely stretched. As John Maynard Keynes reflected nearly a century ago, household savings may be beneficial to the individual, but bad for aggregate economic growth.

Rising joblessness and potentially newfound thrift matters considerably in a country like the US where personal consumption accounts for roughly 70% of GDP. And still undetermined are the inevitable changes in consumer behavior brought about by the pandemic that will further impact corporate earnings.

Few market catalysts on the horizon

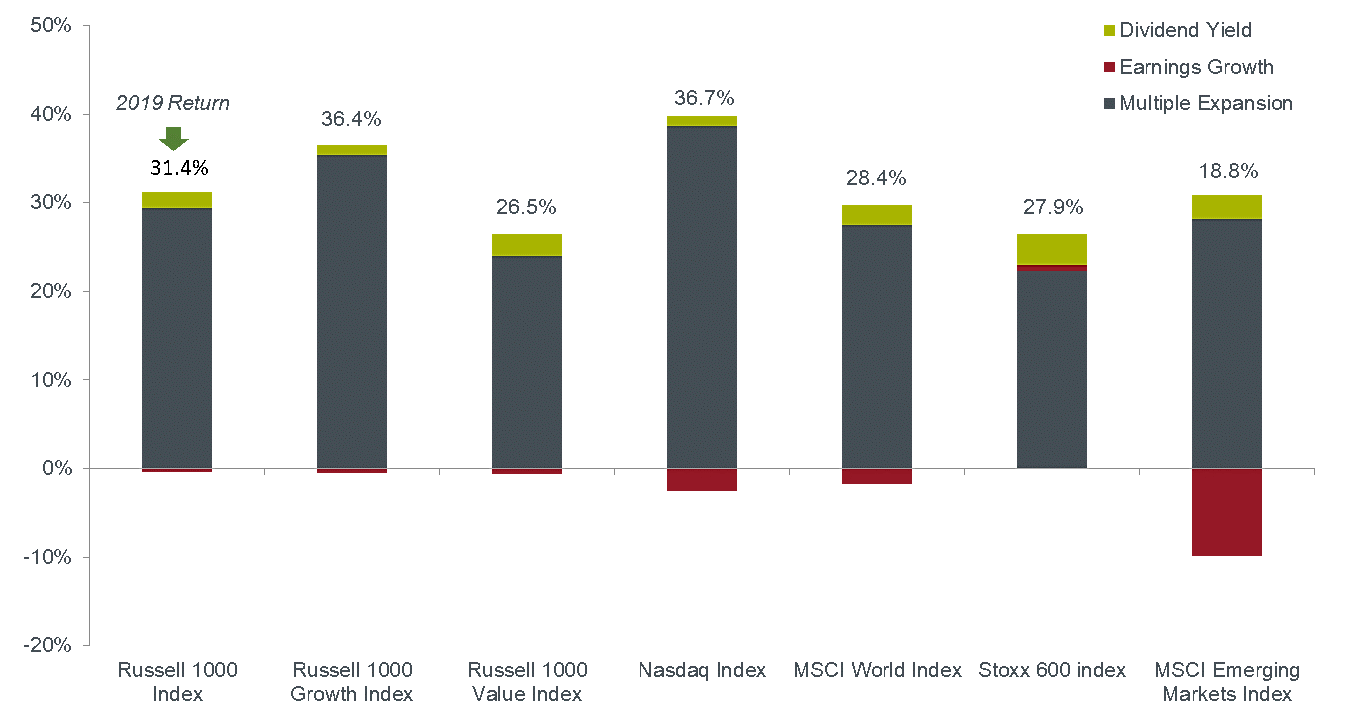

Lest we forget, US stocks achieved record highs only in February. Driving the latter stages of the decade-long rally was P/E expansion and share buybacks. The latter is likely over, especially for companies that have gone hat-in-hand to the government for support. As evidenced by the torrent of earnings downgrades, robust corporate performance is also likely out of the equation.

Much of 2019’s equity market gains were driven by multiple expansion as investors priced in continuing share buybacks and a reduction in the trade impasse (Exhibit 4).

Exhibit 4: 2019 equity index total return decomposition

Source: Bloomberg. Past performance is not a guide to future performance.

That leaves multiple expansion as the sole candidate for rising markets. We are doubtful the justification for higher multiples exists. Price/earnings ratios tend to rise with lower interest rates, which we have in place thanks to the Fed. But we also know that they fall as risk premiums increase and growth rates decline. While companies capable of generating secular growth are likely to continue to command a premium, and rock-bottom interest rates lowers the cost of capital for corporations, we find it a hard sell that unemployment resetting at a higher level, skittish consumers and increased savings will not force investors to dial back the optimism that has fueled the equities rally. The resulting decline in earnings growth along with an historic level of uncertainty, in our view, will ultimately cause investors to command risk premiums on stocks greater than what is presently priced into the market.

When considering this backdrop, the expansion of forward P/E ratios across a range of indices by more than 50% since late March becomes all the more difficult to swallow.

Learn more

As Global Head of Asset Allocation, I will keep you updated on how we are taking advantage of the most compelling opportunities across the globe. Hit the follow button to be the first to receive my latest insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Ashwin is responsible for defining short- and long-term approaches to asset allocation. He also co-manages the Adaptive Allocation strategy and co-managed the Diversified Alternatives strategy from 2016 until 2019. Prior to joining Janus in 2014, he worked at Alliance Bernstein and Platinum Grove Asset Management.

Ashwin earned a bachelor of science degree in chemical engineering and mathematics and a master of science degree in chemical engineering, all from the Massachusetts Institute of Technology. He also holds a PhD in finance from the University of California – Berkeley, Haas School of Business. He has 19 years of financial industry experience.

........

This information is issued by Janus Henderson Investors (Australia) Institutional Funds Management Limited (AFSL 444266, ABN 16 165 119 531). The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson Investors (Australia) Institutional Funds Management Limited believe that the information is correct at the date of this document, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson Investors (Australia) Institutional Funds Management Limited to any end users for any action taken on the basis of this information. All opinions and estimates in this information are subject to change without notice. Janus Henderson Investors (Australia) Institutional Funds Management Limited is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect.

Ashwin is responsible for defining short- and long-term approaches to asset allocation. He also co-manages the Adaptive Allocation strategy and co-managed the Diversified Alternatives strategy from 2016 until 2019. Prior to joining Janus in 2014,...

Expertise

Ashwin is responsible for defining short- and long-term approaches to asset allocation. He also co-manages the Adaptive Allocation strategy and co-managed the Diversified Alternatives strategy from 2016 until 2019. Prior to joining Janus in 2014,...

Expertise

Comments

Comments

Sign In or Join Free to comment