Q4 Outlook: The Wonderful Ball

Chad Slater

Ellerston Capital

When it comes to skiing, kids seem to feel no fear on the mountain – recklessly racing down the slopes, even doing jumps. Adults, on the other hand, seem to feel trepidation even after a much longer time skiing than a kid. This is generally put down to an adult’s fear and more importantly the knowledge of what it feels like to fall over and hurt yourself that is imbedded in the memory.

Often you learn quickly, until you have a bad fall. After that, the fear of the pain is enough to slow the learning curve and increases the time it takes to return to prior levels of confidence.

Markets are much the same: prior to a crash, risk-taking is everywhere and gains accrue swiftly, but afterwards, the gains are eked out at a much slower pace, until that cohort has been replaced somewhat by new kids who have just learnt tricks on the mountain, or the adult’s pain has finally diminished.

The recovery from the 2008 GFC has been extraordinarily long, reflecting the vast amount of damage it did to the psyche of many investors (and their balance sheets). But 10 years on, it finally feels like the bull market is getting into full swing – the assured confidence of “buy the dips” that comes late in the cycle. There are more people in the market who have no working experience of 2008 – you have to be about 33-35 now to have worked through 2008 – and for others, it’s now far enough away that the “fear of missing out” can overwhelm residual fears of loss.

A supportive backdrop

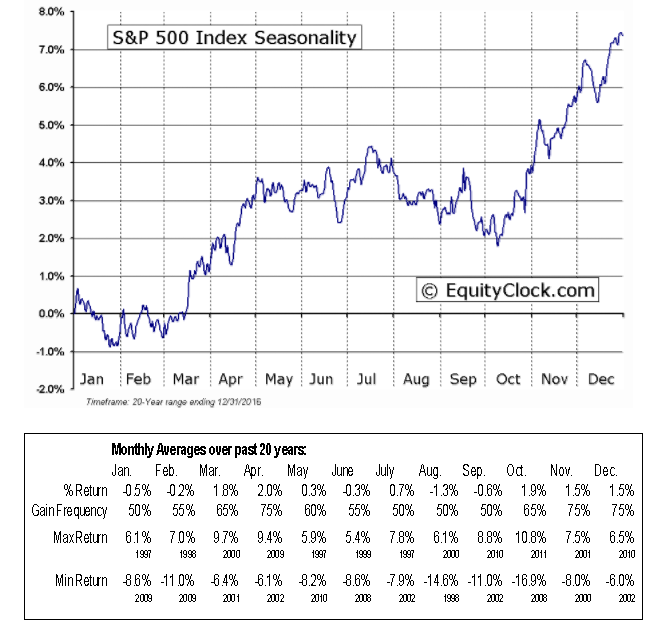

Which brings me to focus on the last quarter of the year. The first thing to note is that, seasonally, it’s a good time to invest in markets. Figure 1 below shows the normalised returns over the course of a year in US markets. As you can see, this part of the year is when the best returns are made. No one is fully sure why this happens – some have suggested that investors feel the need to “catch up”, but it exists nonetheless!

Figure 1 – Normalised returns in US markets over the course of a year

Source: EquityClock

Willing participants

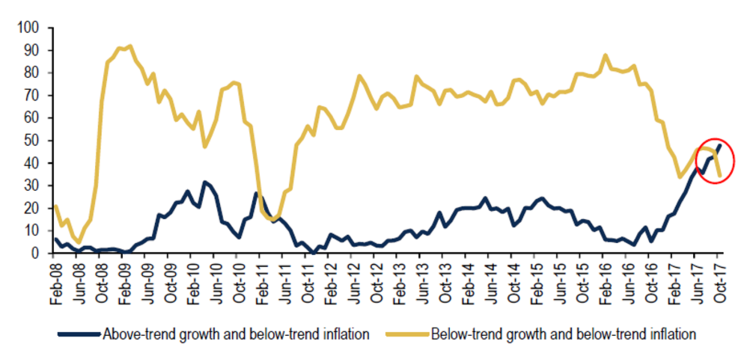

So, the backdrop is supportive to start with. But are the participants willing? Yes, it seems. Bank of America Merrill Lynch (BAML) conducts a survey of investors globally each month, the latest of which came out last week. For the first time in six years, the investors they surveyed are comfortable with “goldilocks” (Figure 2) – that is growth in the world economy, but not with too much inflation, i.e. they think it’s a great time to invest in risky assets.

Figure 2 – “Goldilocks” beats “secular stagnation” for the first time in six years

Source: BofA Merrill Lynch Global Fund Manager Survey

And the participants have the cash!

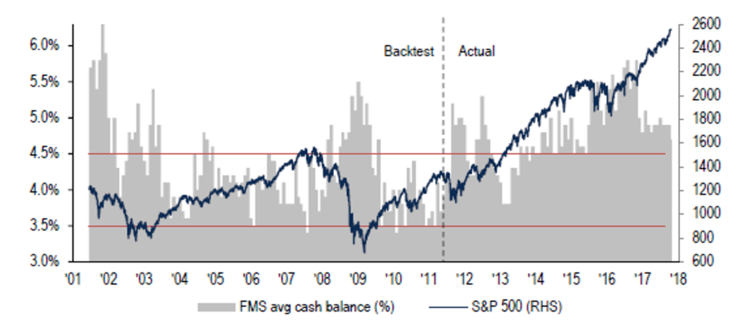

If they are willing, are they able? Yes, as well. The same survey also asked how much cash the managers are carrying. Whilst the level has fallen to 4.7% (Figure 3), with the average over the last 10 years being 4.5%, they still have “dry powder” to put to work in risk assets such as equities (as a reference, it fell to 3.5% just before the GFC).

Figure 3 – Global FMS average cash balance (in %)

Source: BofA Merrill Lynch Global Fund Manager Survey

Lastly, I hate using too many anecdotes, but the “shoe shine boy story” often does reflect the psyche of the populace and a few have started to look like 2006 again:

- At a wedding last weekend, the guest next to me had made over $1m on Bitcoin speculation. Every cycle of mania has its pin-up. Bitcoin is arguably this year’s pin-up.

- A financial planner told me how he’d had a client come in, who had sat in cash for nine years and now wanted to get into equities and “make some money”.

- Brokers are happy again. Business for stockbrokers is amazing when it’s good and awful when it’s bad. A recent broker’s function we attended felt like the “good ol’ days”. Less talk of redundancy, more talk of bonuses and poaching!

So should you sell everything now?

No. The “shoe-shine story” was apparently more than 12 months before the collapse. These stories tell you the quadrant of a clock, not the hour. With Global GDP data so strong and few central banks tightening in 2017, it’s a happy place for now (late 2018 on the other hand may be another matter).

So where do you go? European Equities; cyclicals; banks; Emerging Markets (EM); Japan; Hong Kong. These are all the markets that froth at the end of a cycle – some could go up 20-30% from here in a very short period of time (EM did 27% in 2006 and backed it up with 37% in 2007, even as other indicators were flashing red). That’s generally what happens at the end of a cycle.

Reduce your weighting to the USA and watch them go - and most importantly enjoy it - because the memories will be needed to sustain one through the next stage of the cycle.

“We are at a wonderful ball where the champagne sparkles in every glass and soft laughter falls upon the summer air. We know at some moment the black horsemen will come shattering through the terrace doors wreaking vengeance and scattering the survivors. Those who leave early are saved, but the ball is so splendid no one wants to leave while there is still time. So, everybody keeps asking – what time is it? But, none of the clocks have hands.”

“The Money Game” by Adam Smith (aka Jerome Goodman)

For further insights from Morphic Asset Management, please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chad co-founded Morphic Asset Management in 2012. As a stock picker Chad is also a generalist but has strong regional knowledge of Europe and the Americas. He has also been awarded the CFA Charter.

1 topic

Chad Slater

Co Head Global Equities (ex-Asia)

Ellerston Capital

Chad co-founded Morphic Asset Management in 2012. As a stock picker Chad is also a generalist but has strong regional knowledge of Europe and the Americas. He has also been awarded the CFA Charter.

Expertise

Chad Slater

Co Head Global Equities (ex-Asia)

Ellerston Capital

Chad co-founded Morphic Asset Management in 2012. As a stock picker Chad is also a generalist but has strong regional knowledge of Europe and the Americas. He has also been awarded the CFA Charter.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Funds

The 5 best-performing super funds of the year

Livewire Markets