Quality is always important… but now it’s critical

It’s safe to say the Australian economy is currently experiencing a recovery as businesses continue to re-open following the worst of the COVID crisis. Despite this, there remains a significant amount of uncertainty in the world and as long-term investors, it's difficult to determine what the sustainable level of demand will look like once the impacts of government stimulus, rent relief and interest deferrals come to an end.

The recurring theme, that we’re hearing from the companies we speak to as part of our in-depth research process, is uncertainty. The IML research team has spoken to management teams from over a hundred companies over the past few months to try to understand the impact on their business of the current situation, and what their companies’ prospects are for the future. Nearly every company is looking to manage costs via reducing the number of employees, limiting marketing spend and/or reducing their capex.

Given this uncertainty, we do see some risks in the outlook for the future. We obviously do not know exactly what the future holds but if these risks eventuate, we believe investing in good quality companies is going to be absolutely critical in the years ahead.

Defining quality

Quality means different things to different people. At IML we have defined quality in the same way since the company was founded by our Investment Director Anton Tagliaferro in 1998.

Firstly, we look for companies that have a strong competitive advantage, which means they are industry leaders and are generally number one or two in their category. We invest in companies with recurring, predictable earnings, run by capable and experienced management teams and we obviously want to invest in companies that can grow their earnings over the next three to five years. Of course, we want to be able to buy these companies at a reasonable price.

These are – and will always be - the attributes we look for when we invest in companies on behalf of our clients.

Quality in the COVID environment

There’s no doubt our focus on quality is heightened when looking for opportunities in the current environment. With so much uncertainty around the economic outlook, we are also looking at our long-standing quality attributes through the lens of the COVID crisis.

We want to invest in industry leaders, and this is really important on a number of fronts. If the demand environment is weaker, or competition becomes more intense, it is likely to lead to price falls in certain industries. Industry leaders are usually able to withstand the short-term impacts of lower demand, or potentially lower prices due to their scale and higher margins which gives them more flexibility to hold onto customers. Industry leaders also have the capability to withstand the storm whereas smaller players with less scale and lower margins are unlikely to have the capacity to lower prices for an extended period of time in order to retain customers.

Over the past few months, another thing we have noted across many industries and sectors is a significant drop in customer churn rates meaning that at this stage many customers are less likely to switch to new products or services.

For example, the telecommunications industry’s churn rate is at a record low, and churn rates across electricity and insurance are also at very low levels. One of our conclusions from this is that customers are uncertain and sticking to products they know well – what this also means is that businesses that require new customers each year to make profits are more at risk.

Thus, businesses with predictable, recurring earning streams from existing customers seem to be a lower risk prospect in the current uncertain world.

Another insight we have gained is that almost all consumers and companies are going over their budgets forensically to see which expenses are justified. Therefore, the greatest risk lies with companies providing a good or a service that is non-essential or something that could be substituted for a cheaper option. So our focus is on companies that provide an essential product or service – such as telecommunications, supermarkets selling food and liquor or companies that provide critical infrastructure that is still viable in the period ahead. We believe that these companies offer a much lower risk to investors if the demand environment does not strengthen to the extent that many are expecting in the medium term.

We are also looking for companies that can grow their earnings because of their own specific initiatives, irrespective of the headwinds weighing on a business from future economic growth. We like to invest in companies that have strong cost out or restructuring programs, companies we feel confident that can gain market share over time, or companies which have some contracted growth. These companies potentially will have quite a different earnings profile from others that are very reliant on the economy to grow their earnings.

Experienced management teams with a good track record are generally well versed and equipped to deal with cyclical downturns. We like to invest in companies with management teams that can refer back to past experiences and hopefully call upon some corporate memory of how to deal with recessionary periods. We spend a huge amount of time talking to each company’s management teams and what we really want to see is management that are preparing the company for a number of different environments or scenarios. Companies that are forward looking and on the ball tend to pick up market share, and they are more likely to come out of the crisis in better shape. Unfortunately, those that are on the back foot and reactionary are more likely to lose market share, which may be very hard to get back in the longer term. This is how we are assessing management teams in the current environment.

Quality companies shine through in a weaker economic environment

Two businesses that meet all our criteria from a quality standpoint are Coles and AusNet.

Coles

As the second largest supermarket player in Australia, Coles is quite a simple business with its earnings made up 90% from its supermarkets and 10% from liquor sales. It's a business with a very strong balance sheet with very little debt and fantastic cash flows. Coles also has negative working capital, which means its customers pay upfront for goods and services, and the company can pay its suppliers a bit later. The benefit of this – especially in the current economy – is that Coles has no risk of bad debts. The management team are relatively new, but are very experienced, and we believe that they are making some very positive changes to the business, which we think can deliver growth over the next three to five years.

In our view, Coles can achieve growth in the next few years as it is coming off quite a low base in regards to its margins and its operating potential.

Under previous management the company’s margins had been going backwards and as of last year were at almost a 10-year low. Coles margins are 150 basis points below Woolworth's margins, which - given the sales productivity of Coles and Woolworths are almost identical – means that the margin gap is largely due to Coles’ operational inefficiencies. Given new management are all over this, we see significant potential for Coles to improve its margins over the next few years, if management executes their strategy well.

Another aspect that we believe will deliver growth is an ambitious cost out programme of over a billion dollars, which involves several elements. One of the key elements is to redesign, consolidate and automate the company’s supply chain. At the moment Coles has five Distribution Centres (DCs’s), in both New South Wales and Queensland which are sub scale, and which is at capacity in Queensland. Coles current DC’s are very expensive to run as they are not automated so they require a lot of manual input. Over the next five years, Coles plans to consolidate a number of these sites into fewer highly automated warehouses. This will remove significant costs from the business over the next three to five years. As one of the non-discretionary sectors, as mentioned above, our view is that demand for supermarkets will remain quite solid no matter what the economy does.

So in our view Coles offers good demand growth despite the potential weak economy, as well as company specific growth drivers. On top of that, the company is paying a solid fully franked dividend, which we think will also grow over time.

AusNet

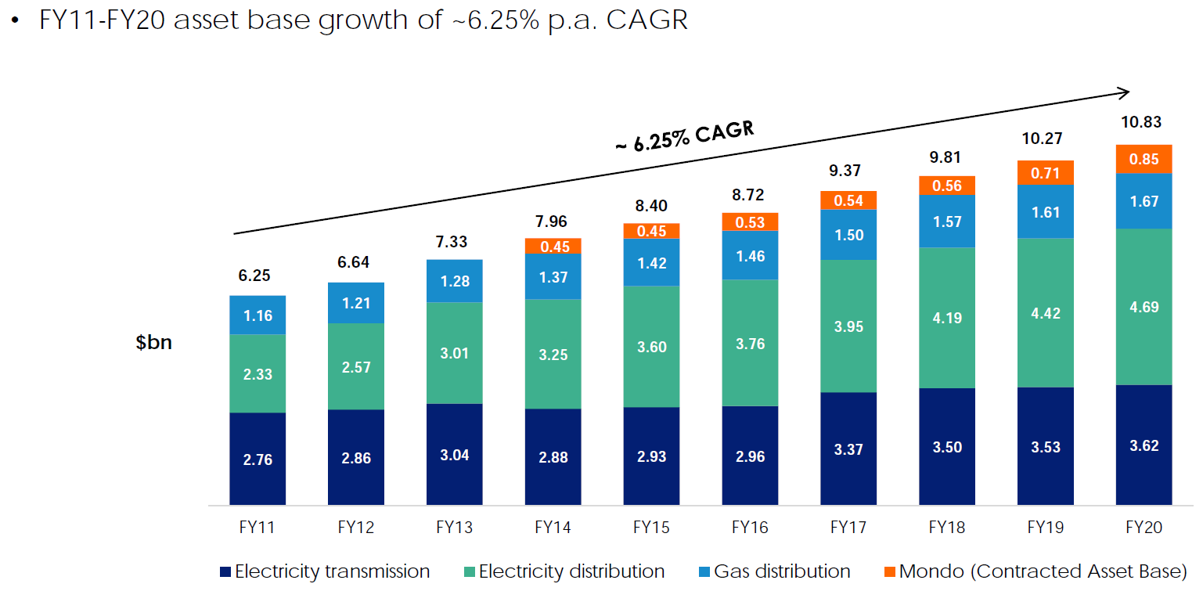

AusNet is a regulated utility which owns electricity and gas distribution assets as well as transmission networks in Victoria and South Australia. These are regulated monopoly assets, so AusNet’s earnings are highly predictable. In addition, the demand outlook for these assets is quite strong, as chart 1 shows AusNet’s asset base has been growing at about 6% per annum.

Source: IML & AusNet FY 2020 Results presentation as at 12 May 2020

This growth is driven by a number of factors, including population growth and the investment in renewable energy that's being made by governments and private companies. These renewables need to be connected to the grid via AusNet and this aspect is growing the demand for the company’s regulated asset base.

Although current demand for electricity is fairly strong, Ausnet actually has no demand risk as its earnings actually aren't reliant on demand.

The government guarantees a level of earnings based on the investment AusNet has, making it one of the safest earning streams in the Australian sharemarket.

AusNet also have a very high quality management team and a strong balance sheet making it, in our view, a very attractive investment in the current environment. In addition, the company is now paying a yield of over 5%, which is 50% franked, and we see this yield growing about 2-3% per annum over the next three to five years.

Conclusion

While sharemarkets have continued to rally very sharply from their March lows, in our view stock-picking is really going to be key in an environment where demand going forward could be weaker as the economy recovers from the COVID 19 shock it has suffered recently. IML’s portfolios are invested in a number of quality companies, such as Coles and AusNet as well as companies such as Telstra, Amcor, Brambles and Orica. These companies have been around for a long time and we believe that their businesses can deliver strong recurring earnings through the economic cycle. We think that these types of companies will weather any future economic down periods well and could in fact come out stronger out on the other side as many weaker competitors fall by the wayside.

Never miss an update

Be the first to receive our latest insights as soon as they are posted on Livewire by hitting the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Since joining IML in 2010, Daniel has been part of the team which won Large Cap Fund Manager of the year in 2012 & 2015. In 2013 he was given Portfolio Management responsibilities within the firm, managing a growing portion of the IML Australian Share Fund.

Featuring

Daniel Moore,

IML

Since joining IML in 2010, Daniel has been part of the team which won Large Cap Fund Manager of the year in 2012 & 2015. In 2013 he was given Portfolio Management responsibilities within the firm, managing a growing portion of the IML Australian Share Fund.

........

While the information contained in this article has been prepared with all reasonable care, Investors Mutual Limited (AFSL 229988) accepts no responsibility or liability for any errors, omissions or misstatements however caused. This information is not personal advice. This advice is general in nature and has been prepared without taking account of your objectives, financial situation or needs. The fact that shares in a particular company may have been mentioned should not be interpreted as a recommendation to buy, sell or hold that stock.

6 stocks mentioned

Since joining IML in 2010, Daniel has been part of the team which won Large Cap Fund Manager of the year in 2012 & 2015. In 2013 he was given Portfolio Management responsibilities within the firm, managing a growing portion of the IML Australian...

Expertise

Comments

Comments

Sign In or Join Free to comment