Quantitative Un-Easiness

Perhaps simply ‘queasiness’ is more fitting. Certainly that’s an apt feeling among investors having stomached sharp falls in risk asset prices in the last quarter of 2018, again bringing into focus the question of asset allocation as investors consider the path ahead. While many of the surprise falls reversed, at least in part, through January this year, it’s important to consider what may have driven the sharp declines and the question is whether they are symptomatic of a more prolonged malaise or a temporary setback. While this is impossible to answer with any degree of certainty it’s hard to ignore the secular shift in the comparable risk/reward metrics of major asset groups, driven by changes in macroeconomic dynamics and an ever fluid political backdrop.

Equity markets have rewarded investors almost without missing a heartbeat in the entire post-GFC environment, buoyed by central bank monetary stimulus. The combination of a stable tiller and cheap money is an intoxicating mix. But now, perhaps if the initial US experience is anything to go by, we’re seeing for the first time in a long while the impact of having ‘the training wheels off’, of borrowing costs moving back to a more normalized level, on a jittery equity market.

What we are faced with today is a shifting set of relative market dynamics combined with a much less certain political landscape, with neither being especially ‘equity friendly’.

One thing that is arguably different now as 2019 begins and we contemplate asset allocation going forward is the risk premia or simply the forecast return spread between cash and bonds, and equities. The ~1% cash rate environment of the past decade is utopia for equities; dividend yields of 4% or 5% easily making them the darling of any asset allocators tool kit. But now that cash rates in the US have exceeded 2% the cost of doing business has changed markedly and the equity dividend yield return spread is less attractive. And that’s before we factor in the tailwind that a rising rate environment ultimately brings to sovereign and credit yields. Sure, there can be some pain to wear on the way up if you leave your duration exposure unhedged, but the forward-looking returns from those asset classes today look a whole lot more appealing. US 10-year treasuries continue to oscillate around the 3% mark, and investment grade credit yields sit comfortably above 4% at the medium-to-long end of the curve.

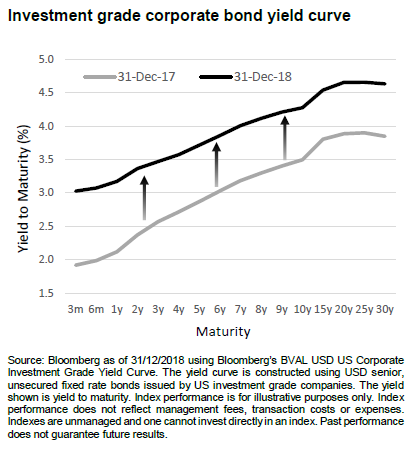

It is said ‘every cloud has a silver lining’, and the chart below clearly illustrates the forward-looking benefit that the combination of sporadically widening spreads and rising rates - which characterized much of 2018 - provides to bond investors; higher yields across the maturity curve with no discernible elevation in an already modest level of default risk. Suddenly an equity dividend yield of even 5% doesn’t feel quite as rich. And almost certainly not on a risk- or volatility-adjusted basis…

All this, and not even a mention of the specific but wide-ranging instances of political instability brought about by populism and anti-globalism and protectionism, a number of which individually have the power to materially disrupt global trade and harmony; an increasingly embattled Trump continuing to top the list.

After all the noise of 2018, those carrying the most defensive strategic asset allocations emerged victorious - a worthy reminder that through cycles there will always be periods where it pays to bias your objectives towards preserving money just as much as growing it. Regardless of whether risk asset volatility of the past couple of months proves to be temporary, or more sustained, higher cash and bond yields certainly signal a harder environment for equities to maintain the strong competitive edge that they have enjoyed over the past decade.

However, our responsibility as investors to those that entrust their money to us means that we cannot sit idly by. This environment has developed as one where optimal balancing between prudent defence and sensible return-seeking becomes paramount. Kapstream portfolios today are finely tuned to maximize returns potential while being insulated against observable and uncertain risks. In a practical sense this means:

- Gently extending duration in domestic (AU) rates where we continue to believe the RBA are a long way from considering hikes, and maintaining a negligible exposure to US interest rates, where there is wide divergence of opinion between continued hikes, and pausing;

- Continuing to avoid material EUR bond and currency exposure, where volatility and uncertainty persists;

- Maintaining a shorter overall maturity profile, which has proven beneficial in insulating portfolios from continued widening of spreads and resultant price falls that stem from this; and

- Increasing AUD-denominated bond exposures to exploit wider domestic spreads, and also being less susceptible the impact of further unforeseen spread widening (US and EUR credit spread losses have been far greater).

The likelihood is that this remains an environment where a strong constitution is important. Take a few deep breaths, and to borrow from Nat King Cole, while there may be trouble ahead, we must face the music and dance. But perhaps from the edge of the dance floor, and ready for a swift exit should the music stop abruptly.

Further insights

For more insights from Kapstream Capital, visit our website

--------------------------------------------

Disclaimer

Unless otherwise specified, any information contained in this publication is current as at the date of this report and is provided by Fidante Partners Limited (ABN 94 002 835 592, AFSL 234668) the issuer of the Kapstream Absolute Return Income Fund (ARSN 124 152 790) (Fund). Kapstream Capital Pty Limited (ABN 19 122 076 117, AFSL 308870) is the investment manager of the Fund. It should be regarded as general information only rather than advice. It has been prepared without taking account of any person’s objectives, financial situation or needs. Because of that, each person should, before acting on any such information, consider its appropriateness, having regard to their objectives, financial situation and needs. Each person should obtain the relevant Product Disclosure Statement (PDS) relating to the Fund and consider that PDS before making any decision about the Fund. A copy of the PDS can be obtained from your financial adviser, our Investor Services team on 13 51 53, or on our website (VIEW LINK). If you acquire or hold the product, we and/or a Fidante Partners related company will receive fees and other benefits which are generally disclosed in the PDS or other disclosure document for the product. Neither Fidante Partners nor a Fidante Partners related company and our respective employees receive any specific remuneration for any advice provided to you. However, financial advisers (including some Fidante Partners related companies) may receive fees or commissions if they provide advice to you or arrange for you to invest in the Fund. Kapstream Capital, some or all Fidante Partners related companies and directors of those companies may benefit from fees, commissions and other benefits received by another group company.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Founded in 2006, Kapstream offers investors an alternative approach to fixed income, combining capital preservation techniques with unconstrained portfolio management skills in the pursuit of stable, absolute returns.

Kapstream

Founded in 2006, Kapstream offers investors an alternative approach to fixed income, combining capital preservation techniques with unconstrained portfolio management skills in the pursuit of stable, absolute returns.

Expertise

Kapstream

Founded in 2006, Kapstream offers investors an alternative approach to fixed income, combining capital preservation techniques with unconstrained portfolio management skills in the pursuit of stable, absolute returns.

Expertise

Comments

Comments

Sign In or Join Free to comment