Raw material inflation: Picking the winners and losers

Costs are rising. Raw material inflation is coming through the supply-chain across industrial stocks. As a result, earnings pressures are emerging in many companies with exposure to raw materials. We have seen this in companies with exposure to oil (such as transportation, rubber or plastics) and pulp (i.e. Paper and building materials). Share prices have fallen as a result of downgraded earnings.

This article takes a closer look at some of the companies impacted by rising raw material costs, as well as where we are seeing the risks and opportunities. We conclude that now may be the time to invest in companies that have been oversold due to cost inflation concerns, particularly those that are able to pass rising costs through to their customers.

The losers

The Australian equity market has seen a number of companies downgrade FY19 earnings due to rising raw material costs. In October, James Hardie downgraded earnings after reporting 2Q19 results. FY19 profit guidance was reduced by approximately 6% citing increases in key input costs such as pulp, freight and cement. The share price subsequently declined 15%.

In our view, the James Hardie share price decline is an opportunity to buy a high-quality business, with solid growth, at a compelling valuation. Over the medium-term, we expect input costs to revert, while James Hardie should be able to deliver strong earnings growth underpinned by high single digit revenue growth through a combination of market and share growth in the US housing market.

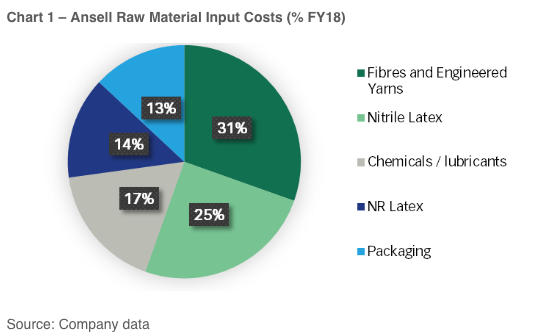

Ansell is another company negatively impacted by rising raw material costs. Ansell manufactures and sells gloves and other protective rubber and latex products in the healthcare and industrial sectors. The key raw material inputs for Ansell are highlighted in Chart 1.

Rising raw material costs are a major headwind for Ansell’s earnings. Key raw material inputs including Fibres and Yarns (for example, Cotton) and Nitrile Latex have seen significant price rises over the year, up 13% and 27% respectively. In August, the company’s management downgraded FY19 earnings guidance by approximately 7%, resulting in a 9% fall in the share price. The Ansell downgrade highlights the impact higher raw material prices can have on profit margins, particularly for companies unable to increase prices and pass these costs onto their customers.

What happens next? Picking the future winners

Some companies are better placed than others. There are companies in favourable industry structures that are able to pass rising costs onto their customers. Below we highlight two companies that we believe meet the above criteria.

Qantas Airways

Since July 2018, Qantas has fallen by approximately 11% on the back of rising cost concerns, in particular higher oil prices. There is no doubt that higher oil prices impact Qantas’ earnings. However, what makes Qantas unique is its ability to pass these higher costs through to customers. Over the past year, we estimate Qantas has increased its domestic airfares by 7%. At the same time management are continuing to deliver cost out initiatives to offset the impact of higher fuel costs.

As the domestic market leader in a rational duopoly we believe Qantas is well placed to raise ticket prices to offset the impact of higher future oil prices. At current valuations, trading on a price to earnings multiple of 9.4x vs global peers at 12x – in a more favourable industry structure – Qantas continues to represent a compelling high conviction investment in portfolios for our clients.

Amcor Ltd

Amcor is the global leader in flexible consumer packaging. One of the key raw material inputs into Amcor’s flexible packaging business is resin (plastic), which reached new highs in April 2018. However, Amcor has contractual raw material inflation pass through to its underlying customers. Over the short term, there is a lag of approximately 3-months to recover raw material cost increases. However, over the medium-term, Amcor is well placed to pass almost 100% of raw material cost inflation through to its underlying customers.

In August, Amcor announced the acquisition its largest competitor Bemis for US$6bn. Bemis enhances Amcor’s position by giving it a strong position in North America in addition to Amcor’s existing European and emerging market positions. The acquisition truly establishes Amcor as the global leader in packaging, able to offer global solutions. With a solid track record of generating value from acquisitions, good organic growth and a compelling valuation, Amcor is a high conviction position in the Firetrail portfolios that is well placed to navigate the current market environment.

Conclusion

Companies with exposure to raw material inflation will continue to see earnings pressure into FY19. As stock pickers, the key question we are asking ourselves is who are the winners and losers impacted by rising raw material costs?

In our view, investors should be wary of companies in highly competitive markets with a non-differentiated product, which may not be able to pass rising raw material costs on. Companies in market leading positions such as Qantas and Amcor who are able to pass higher costs onto their underlying customers will fare better in this environment. Businesses with strong earnings growth such as James Hardie, which has been sold-off heavily also represents a compelling long-term opportunity for our investors.

Want to learn more?

For further insights from the team at website.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Managing Director at Firetrail Investments as well as Portfolio Manager for the Firetrail High Conviction Fund and the Firetrail Absolute Return Fund. 34+ years’ experience investing in equity markets.

4 stocks mentioned

Managing Director at Firetrail Investments as well as Portfolio Manager for the Firetrail High Conviction Fund and the Firetrail Absolute Return Fund. 34+ years’ experience investing in equity markets.

Expertise

Managing Director at Firetrail Investments as well as Portfolio Manager for the Firetrail High Conviction Fund and the Firetrail Absolute Return Fund. 34+ years’ experience investing in equity markets.

Expertise

Comments

Comments

Sign In or Join Free to comment