Reasons to be Cheerful

Etienne Alexiou

Belay Capital

When I last published to Livewire in May 2018, the macro environment was distinctly negative for risk assets. The USD value of global money supply had been contracting sharply as central banks tightened liquidity along with the US Federal Reserve Bank raising the federal funds rate. Inflation expectations were elevated on the expectation of wage increases which was adding further pressure on risk free rates to rise globally.

Further, the US government had added fiscal stimulus via tax cuts which despite adding materially to government debt had a low multiplier to growth. The US were following a new trade and foreign policy path of actively seeking redress to trade deficits via tariffs on their major trading partners and renegotiating historical trade deals and defence pacts. This against a backdrop of equity markets trading at historically high valuations and having reached peak earnings growth and credit markets trading at tight spreads to government debt.

Where we have come from

In summing up our macro view in December and looking forward to 2019 we stated;

“Whilst we have been bearish financial and real asset markets for 12 months due to the rising cost of the USD partnered with the reduction in the USD value of global money supply, we are starting to see reasons to be cheerful.”

“The December China PMI print of 49.4 (weakest since February 2016) along with falling global PMI’s are counter-intuitively the first glimmer of positive news we have seen for some time. This because a contraction in manufacturing although reasonably common (occurring every 3-4 years) will normally cause an overreaction by central banks. Thus, whilst this manufacturing slowdown will continue for Q1 2019 it throws up the first light in the tunnel for global asset markets. Markets also overreact to a slowdown in manufacturing thus offering us the opportunity to monetise the move.”

“We are beginning 2019 with inflation expectations falling, much lower risk-free rates and more reasonable equity market valuation multiples than the average in 2018. We are also most of the way through the tightening in liquidity from the US Federal Reserve and the tapering in asset purchases from the ECB. The financial markets are now finding their new cruising altitude post the abundance of liquidity of the past few years. Structurally the market has been fundamentally altered during a time when it was working with the low volatility safety net of central bank QE. Further, we are in the middle of a manufacturing slowdown as evidenced by declining global PMI’s. However, the manufacturing cycle works more quickly than the broader economic cycle and central banks tend to (over)react historically.”

Where we are now

January proved to very interesting as we saw the ECB, Bank of China, and US Federal Reserve Bank all take steps towards loosening financial conditions either by signalling a more dovish stance or directly adding liquidity. The last time we saw a manufacturing recession in mid-2016 the central banks responded by keeping financial conditions overly accommodative throughout 2017. This set up the necessary financial conditions for risk assets to rally strongly throughout 2017.

The change in outlook by the major central banks in January 2019 was important to stabilize risk assets. We certainly do not believe that financial conditions will revert to the overly accommodative stance of 2017 in the near future. Thus, we are not likely to revisit the peak valuations of 2018, but the swift reaction of central banks in altering their outlook post the dramatic fall in global PMI’s in Q4'18 will ensure the risk-free rate remains low and financial conditions more supportive than those prevailing in H2'18.

Looking ahead

At this point, the probability of the manufacturing slow down and tightening in global liquidity of 2018 becoming a prolonged downturn and economic recession in 2019 has lessened. The balance of risks remains towards being very cautious regarding financial markets. Should the availability of credit tighten further the monetary response would be somewhat muted given the cash rate in Japan and Europe is already negative. The Keynesian fiscal response would also be very limited given the global level of government indebtedness. A recession would therefore be longer lasting than usual.

Governments have to a great extent brought forward growth by increasing debt to deliver on populist agendas or combat the rise of populism globally. From a societal perspective this has perpetuated the inter-generational and socio-economic ‘unfairness’ in wealth and income distribution. Furthermore, borrowing from future growth via increased debt lowers the probability for economic growth to return to previous decades high water marks which reduces the opportunity set for future generations to close the ‘unfairness’ gap in wealth and income disparity. The reason this is important for market outcomes as well as from a social and ethical perspective is it increases the chances for future policy responses to redress this gap. The central role of government is to provide public goods and allocate resources. The allocation of resources has clear implications for economic and financial market outcomes.

In the US we are beginning to hear about the platforms of the Democratic nominees which include Elizabeth Warren’s suggestion of a ‘wealth tax’ of 2% of assets over $50 million and 3% over $1 billion, or Alexandria Ocasio-Cortez’s policy platform for an increase in the top marginal income tax rate to 70% on incomes over $10 million. In Europe we having seen populist governments win in Italy and Hungary we have seen further social unrest particularly with France’s ‘yellow vest’ movement.

The willingness of the majority of the population to continue to put up with declining living standards, in direct contrast to expectations promoted by successive governments and the community of improving living standards, is likely to lead to societies becoming more combative over what they regard as their entitlements and the responsibilities of governments and corporates. The global populist vote stands at its highest level since 1938 and the resulting political backdrop of some extreme left- and right-wing policy is likely to continue for some time into the future.

Closer to home

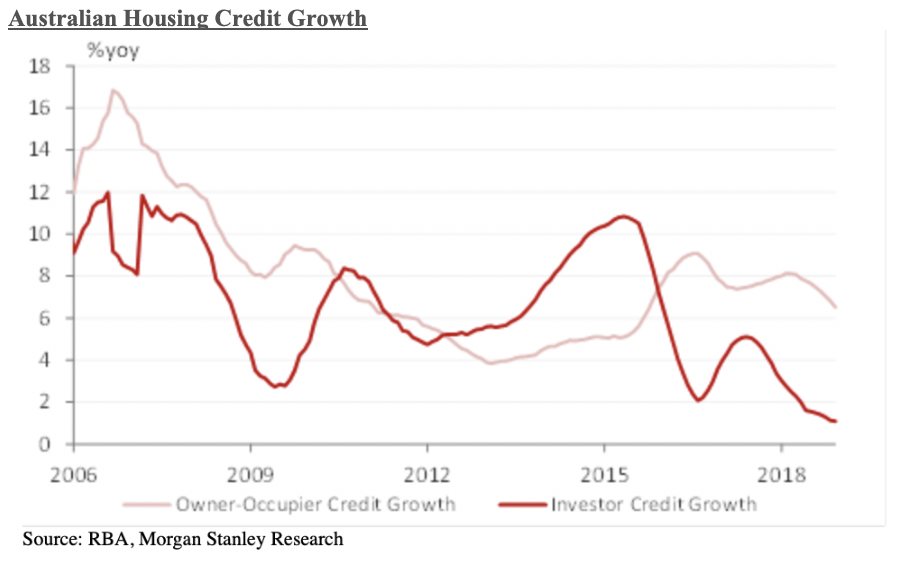

The outlook in Australia has evolved in a more concerning direction whilst the rest of the world has begun so show glimmers of hope. The big four banks have cut their funding budgets from circa AUD 130 billion to AUD 100 billion for 2019. This tightening in the forecast availability of credit by the big four banks and the upcoming federal election will ensure economic activity remains soft for H1 2019. Further, falling house prices have a significant impact on household consumption and some households are overly indebted. The outlook further depends on exogenous factors and with US, European, and Chinese growth all weaker than the average for 2018 the balance of risks is to the downside for Australian growth.

Australia has avoided a recession for 27 years, which is a wonderful achievement and testament to the diversity of the economy. Australia avoided the last great global recession of 2009 due to the very large fiscal spend of foreign governments, particularly China’s commitment to infrastructure and property construction which fueled a ‘once in a generation’ commodity boom.

As we have previously discussed, the global economy is now operating without the safety net of a meaningful fiscal response to an economic downturn. The more normal relationship of the Australian economy being a high beta to world growth (relying on exogenous growth to fuel domestic growth) is much more likely to be the case going forward. We thus expect Australia to be a global underperformer economically for 2019.

And finally, why we’re cheerful

In all, the fall in many major economies PMI’s through December has counter-intuitively given us our first reason to be cheerful in 12 months. This due to the fact that markets and most importantly central banks overreact to manufacturing downturns. Whilst we must be cognisant of the skew to downside risk given the limited potential for fiscal and monetary response to a broader economic downturn, financial conditions are now more accommodative than in Q4 2018. Although tighter lending standards in Australia and the US continue to be of concern (particular the budgeted credit tightening in Australia) we continue to see financial conditions and asset valuation as more supportive than in 2018.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Etienne is co-founder and Chief Investment Officer of Belay Capital.

Etienne Alexiou

Chief Investment Officer

Belay Capital

Etienne is co-founder and Chief Investment Officer of Belay Capital.

Expertise

Etienne Alexiou

Chief Investment Officer

Belay Capital

Etienne is co-founder and Chief Investment Officer of Belay Capital.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management