Rerating to continue after near-death experience

Ashley Services Group (ASX:ASH) listed in 2014 as an integrated vocational training provider and labour hire group. The emphasis was on the Training division but when that business collapsed under the well publicised VET funding scandals it kicked off a long period of restructuring and uncertainty.

But with new management, a booming Labour Hire division and the Training business restructured ASH looks like a company in the early phases of what could be a decent turn around story. Earnings are growing quickly, the company has multi-year tailwinds and the stock is trading on a mid-single digit earnings multiple with prospects of a healthy dividend.

Training

The entirety of the ASH share price decline can be attributed to the issues revolving around the Training division and whether or not its failure would take the company with it. To ASH’s credit, and perhaps to the surprise of the market, the restructure of the Training division has been successful and while it will never generate the kind of earnings it did a few years ago, it is now a stable and profitable contributor to the group.

In WA and QLD the Training businesses are profitable and funding contracts remain in place. One would expect this to continue. Victoria and NSW were where the issues existed. NSW is closed. Victoria is currently operating at a small loss but the company noted at the AGM that it has applied for funding that if received would result in the division returning to be a significant contributor to the group in 2018 and 2019.

Investment into compliance and administration in recent periods suggests they may have a chance of securing funding for Victoria. If they do it will be a catalyst to the share price as the market certainly isn’t pricing in any ongoing success for this division. But even without it I would expect Training to remain profitable.

Labour Hire

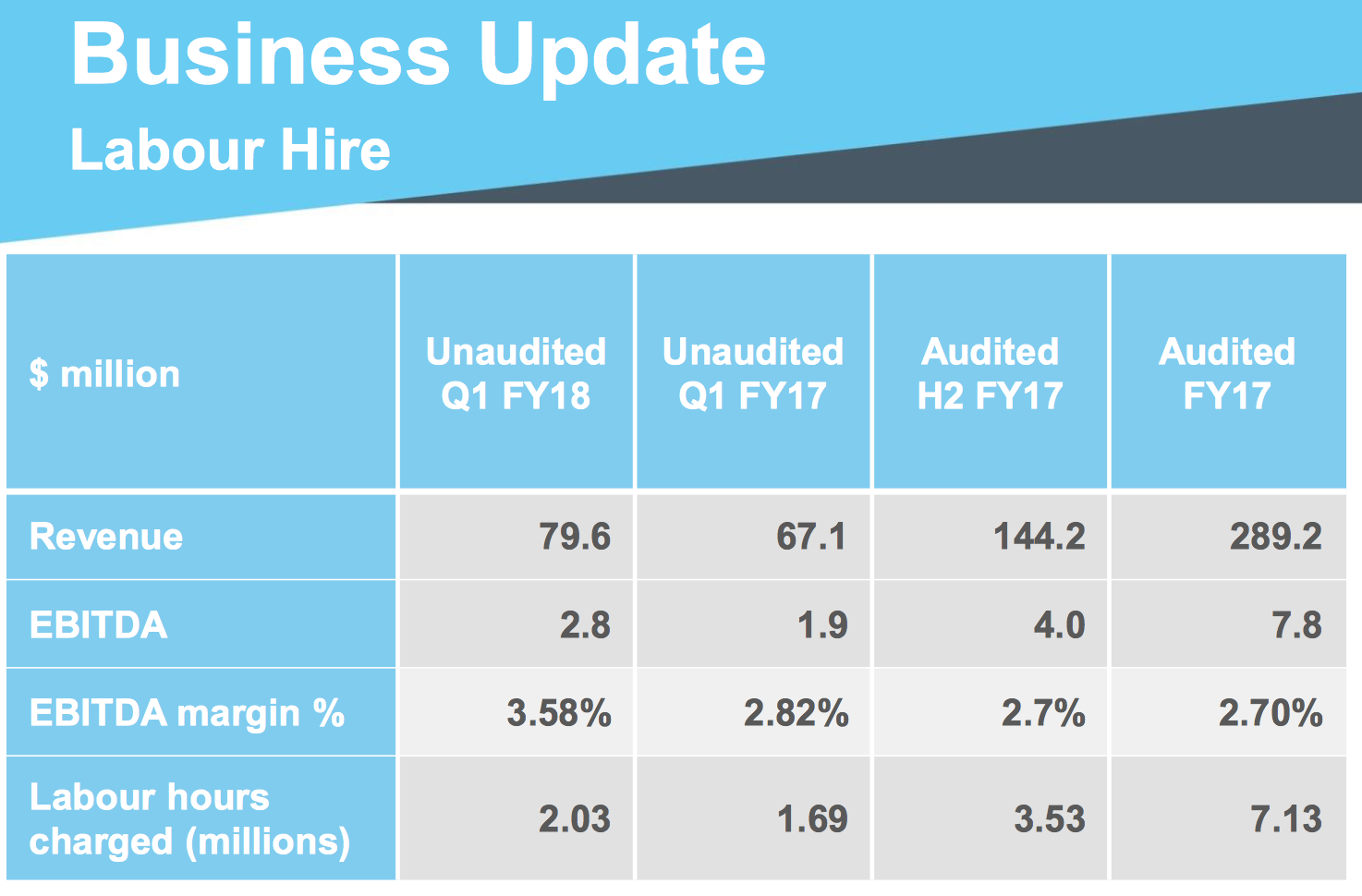

The real focus for the company going forward is its highly profitable Labour Hire business. This division consists of Action Workforce (supply chain, logistics), Concept Engineering (infrastructure, construction) and Blackadder Recruitment (white collar, executive search). All up it generates about $300m revenue and $10m+ EBITDA based on the 1Q18 run-rate.

Action Workforce, the bulk of revenue, is growing the top line at just under 20% off the back of good growth in supply chain and logistics and by winning share off competitors. This is a high volume/low margin business but Action’s customer retention rates are solid and the pipeline of new customers is strong.

Concept Engineering generates most of its work through infrastructure projects in Victoria and NSW. The market is generally in consensus that we are in the early stages of an infrastructure boom, at least on the East Coast, and Concept are well positioned to benefit from this. The growth is already coming through with 70% revenue growth last year and ~30% in 1Q18. Higher margins in this business will trend overall margins higher as Concept grows its share.

Blackadder is much smaller and is not currently a material contributor to the group but it is profitable and with new management there may be some upside.

Throughout all the drama with the Training division Labour Hire not only remained profitable but continued to grow. That growth began to accelerate in 2H17 and is yet to show any signs of slowing. 1Q18 saw EBITDA of $2.8m, up 50% over the prior period with operating leverage starting to flow through (revenue up ~20% yet costs were slightly down). 1H18 results should be positive given that 1Q18 saw impressive growth and the current quarter (2Q18) is seasonally the strongest.

Financials

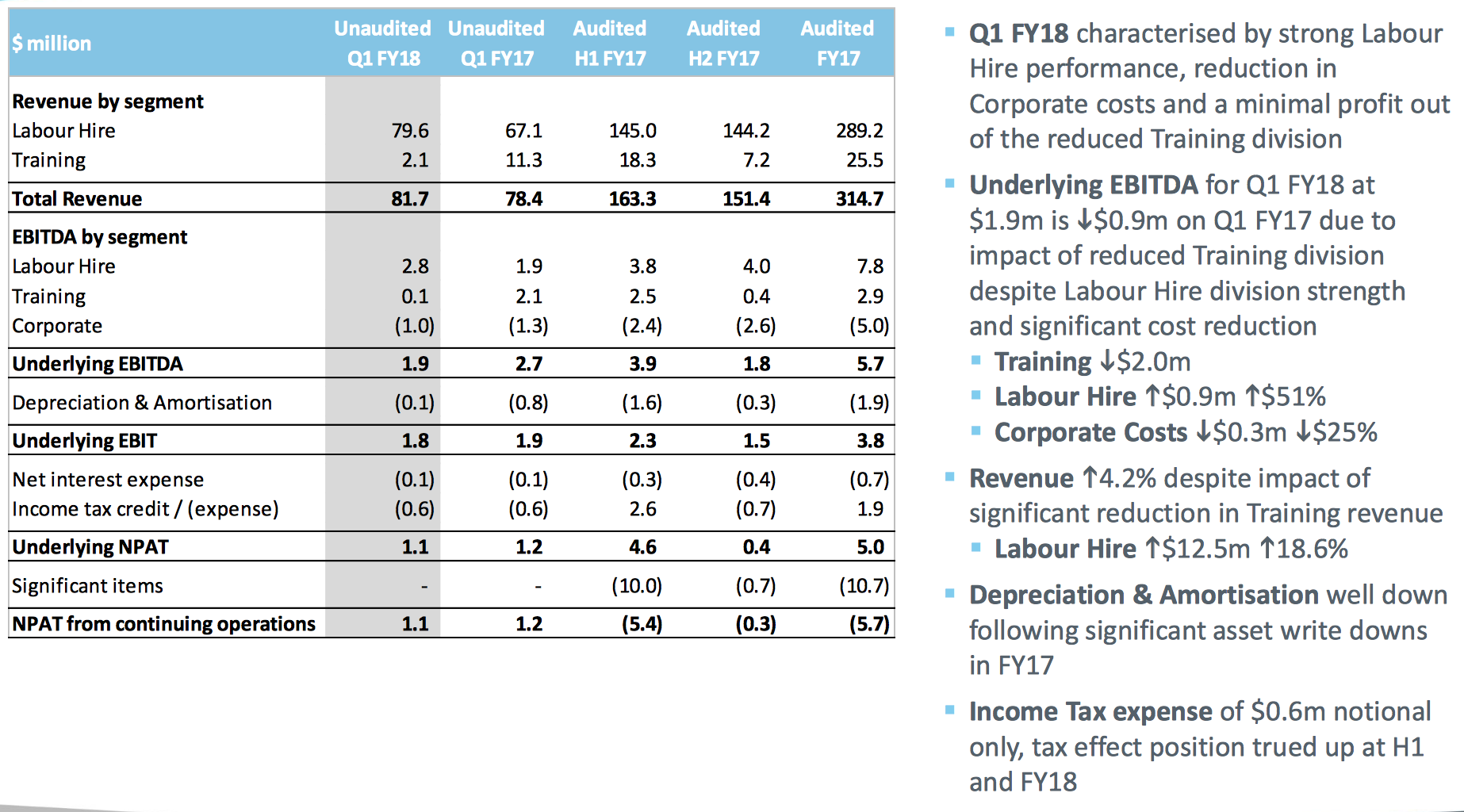

The 1Q18 results were presented at the company’s recent AGM and are displayed below.

Training should remain steady throughout the rest of the year unless the company receives funding in Victoria, in which case I’d expect a gradual ramp up from the start of calendar 2018.

Labour Hire appears likely to continue its momentum. While the nature of the business is highly competitive with tight margins there are tailwinds and operating leverage. Efficiencies should continue to play out with the recent investment in payroll, billing and rostering, most of which was completed in 1Q18 and should help facilitate limited increases in the cost base despite the rapid top line growth.

While the first half is seasonally stronger than the second the rate of growth should mean the difference isn’t too material. For example last year the split was 50/50 simply because the business was growing so quickly.

Corporate costs have come down materially and should remain stable.

While 1Q18 NPAT was reported as $1.1m the tax expense was notional assuming a 30% tax rate. But the company has sufficient tax losses to mean they won’t be paying much tax in FY18 and will probably revert to paying the full tax rate at some point in FY19. So cash earnings are likely to be materially higher than the reported NPAT for the quarter.

Net cash is sitting at ~$2m and with a $5m funding facility in place through a company associated with the MD and largest shareholder that should be sufficient to manage this period of growth for Labour Hire in what can be a fairly capital intensive business. Expansion of this facility, or re-engagement with the banks, would be a positive.

Reflecting the company’s optimism moving forward is the fact they have told the market that dividends are likely to be reinstated in FY18. While a specific payout ratio hasn’t been provided it is quite plausible that the yield will be in the high single digits, unfranked.

Assuming a general continuation of the above trends NPAT should come in at c.$5.5m, depending on tax. That would put ASH on a P/E of 5-6x for FY18.

Class Action

One of the clouds hanging over ASH has been an ongoing class action that arose out of the chaotic share price decline post listing. The key accusation revolves around the level of detail ASH provided in their prospectus regarding the removal of the ‘Tools for your Trade’ program ($5,500 for an apprentice to purchase tools) and the impact it would have on one of the businesses ASH was acquiring (Integracom). Some time after listing ASH noted that Integracom enrolments were below forecasts and blamed it partly on the impact of the removal of this program.

Without going into detail I would note that ASH appear to have a decent defence. They did disclose in the prospectus that the Tools for your Trade program had ended and that the program was replaced by a seemingly attractive $20k loan scheme. The issues around Integracom weren’t the primary driver of the share price decline with that accolade belonging to the unsustainable business models and reliance on government funding. The prospectus was clear that the majority of revenue was derived from government in one way or another and that the number one risk was any change to these funding models.

The above is largely secondary to the fact that any liability would presumably be covered by an insurer, although the details are impossible to know until after the fact. Almost all of these cases settle but with three other defendants dragged in to the matter it is unlikely to be resolved anytime soon. I would expect that as the market realises that the class action may pose less of a risk to ASH than first anticipated the share price will react positively. And of course any news on a resolution favourable to ASH would be a very powerful catalyst.

The risk around the class action is not zero, but it is likely less than what the current price appears to be factoring in.

Re-rate To Continue

The company is emerging as a focused labour hire provider to two sectors of the economy experiencing solid growth with the outlook for more to come. Training is stabilised with some prospect for upside pending news on funding. The balance sheet is relatively sturdy and healthy dividends are on the way. Much of the stock overhang has been removed when Viburnum Funds went substantial and they now own just over 7%. The largest shareholder by a long margin is the MD.

There are two recent listings that provide some basis for relative valuation - People Infrastructure (ASX:PPE) and The GO2 People (ASX:GO2). The former trades on ~12x and the latter on 20x (trailing). That makes ASH’s earnings multiple of 5-6x look compelling particularly since you could argue it has better growth prospects than both of the aforementioned companies. A re-rate to 9-10x would see ASH trading at 30-35c.

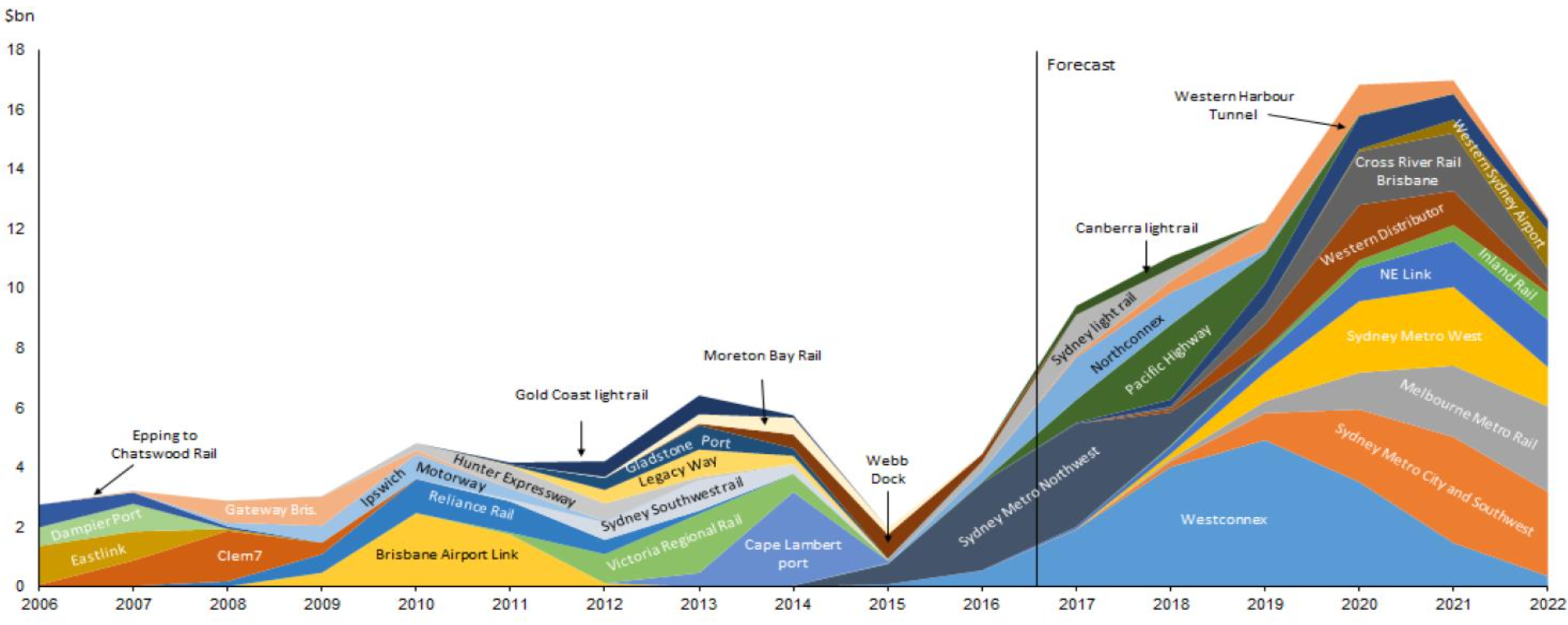

The chart below from Deloitte Access Economics has been used in just about every article explaining the outlook for the construction sector and infrastructure spending, so I apologise for bringing it back once more, but it gives you an idea of where ASH sits in terms of its exposure to the coming growth and the tailwinds at its back over the next few years. It is not surprising that many companies exposed to this growth are hitting 52 week highs.

Disclosure: I hold shares in ASH.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund.

Previously worked for Pie Funds and Bligh Capital.

1 stock mentioned

HD Capital Partners

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund. Previously worked for Pie Funds and Bligh Capital.

Expertise

HD Capital Partners

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund. Previously worked for Pie Funds and Bligh Capital.

Expertise

Comments

Comments

Sign In or Join Free to comment