Risk of value traps increasing

COVID-19 has been profound and pervasive. We have seen massive shock waves impact our way of life, the economy, company business models, credit markets and liquidity. Most businesses have been significantly negatively impacted, a few lucky ones have benefitted. COVID-19 is probably as close as it comes to a black swan event. Not surprisingly volatility moved above the Global Financial Crisis (GFC) levels and the price reaction has been the most savage since 1987. So far central banks and governments are acting to mitigate some of the financial fall out and we can expect further support in months to come. Ultimately we will move through this crisis but volatility is likely to persist for the foreseeable future.

Uncertainty in earnings increases the risk of value traps

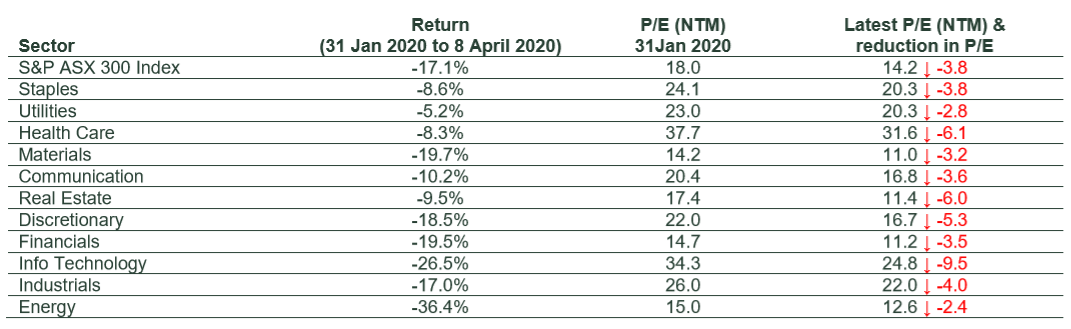

Very few business models would have contemplated or positioned for the COVID-19 scenario that has unfolded across the world. As Figure 1 below highlights the most cyclical companies have been impacted the most but even defensive sectors have not gone unscathed. For example defensive grocery businesses that have benefitted from increased sales have been hurt by increasing costs and some supply disruptions. Some defensive Health Care companies have seen downgrades due to a reduction in elective surgery or due to changes in regular doctor patient relationships.

With so many business models under stress there is a huge amount of uncertainty.

Companies themselves are unsure about their earnings as evidenced by the broad-based suspension of company guidance. Investment analysts are reviewing company models and updating their expectations for earnings but recognise the increased risk to these forecasts. Many analysts are waiting for greater visibility before updating their expectations for earnings – leaving many estimates stale. The same is true of expected dividends and buybacks.

In Figure 1 below we highlight the valuation changes from the end of January to the 8th of April 2020. At face value the earnings multiples are more compelling but how much confidence do we have in those valuations? The “cheaper companies” are currently at a much greater risk of being a value trap if those earnings or dividends or cashflows continue to deteriorate in the coming months.

Figure 1: Earnings multiples are lower but how certain are we in the earnings?

Source: Thomson Reuters, State Street Global Advisors as at 8 April 2020. P/E = Price to Earnings Ratio NTM = Next Twelve Months Past performance is not a reliable indicator of future performance. This information should not be a recommendation to buy or sell any security or sector shown. It is not known whether the sectors shown will be profitable in the future.

Significant earnings decline, debt concerns and dividends at risk

With the large and unforeseen negative shocks to company earnings many companies are exposed form a credit perspective. In recent weeks we have seen a number of companies raise additional capital to shore up their balance sheets.

We can likely expect more capital raisings in coming months. With earnings under stress and debt obligations looming it is natural to expect dividends to be under pressure as well.

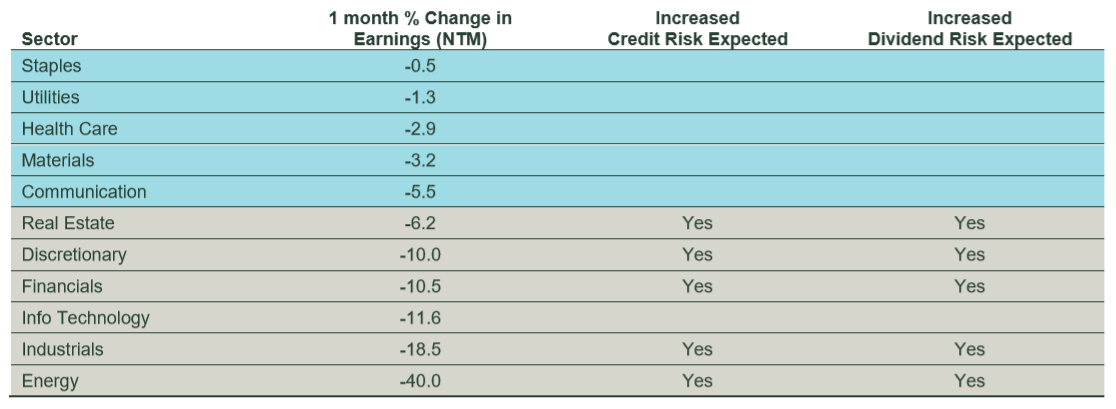

Buybacks will be down in 2020 as well. In Figure 2 below we highlight the recent trends in company downgrades across the major ASX sectors as well where we expect increased credit risk, and dividend risk.

Figure 2: Significantly lower earnings will likely result in lower dividends

Source: Thomson Reuters, State Street Global Advisors as at 9 March 2020. NTM = Next Twelve Months Past performance is not a reliable indicator of future performance. This information should not be a recommendation to buy or sell any security or sector shown. It is not known whether the sectors shown will be profitable in the future.

The most impacted sectors

The obvious industries like restaurants, airlines, tourism and leisure, discretionary retail have all been significantly impacted directly by the isolation measures but are expected to be further impacted by the worsening economic conditions. Slower economic growth, high unemployment, lower property prices all impair household budgets and balance sheets. The same forces are having a negative impact on property trusts, especially those in the retail space. If the shops can’t earn income then they are not well placed to pay the rent. The commercial side is not unscathed either. What will demand for commercial look like in an economic slowdown and if the working from home experiment becomes more mainstream?

Not surprisingly the Banks are also in an unfortunate position. A sharp slowdown in economic growth and increase in unemployment will impact business and consumers and their ability to repay debts. The Banks will see impairment charges rise which will impact earnings and capital and future dividends. Industrial companies are naturally cyclical and will be especially hurt if we do not see a “V” shaped recovery. Energy of course has been adversely affected with the combined impact of both over supply and a large decline in demand knocking crude oil prices by more than 50%.

The high cost producers or those with more leveraged balance sheets will be the most at risk.

Portfolio positioning and performance

It is in these times of uncertainty that we appreciate a more conservative approach to investing. Our focus on quality, less expensive names, those with expected improvements in profitability and lower expected risk as well as portfolio diversification will likely help us navigate these uncertain times. The portfolio has been overweight in more defensive businesses which we feel are better placed to weather the more difficult market environment ahead.

The State Street Australian Equity Fund outperformed its benchmark during March. From a sector perspective, having a lower than benchmark weight to Financials was the key contributor (not holding the major banks). Stock picking within Communication Services (Spark NZ and Telstra) having a lower exposure to Energy also contributed. On the other hand, having a higher relative exposure to Real Estate detracted. Throughout the crisis thus far, our portfolio has provided a level of downside protection that falls within our expectations. We are confident that the investment process we have built over the long-term will weather the current storm, as it has in many other significant market events.

Learn more about risk aware investing

Stay up to date with our latest thoughts by clicking follow below and you'll be notified every time we post content on Livewire.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

Featuring

Bruce Apted,

State Street Global Advisors

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

2 stocks mentioned

Head of Portfolio Management – Australia, Active Quantitative Equity

State Street Global Advisors

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

Comments

Comments

Sign In or Join Free to comment