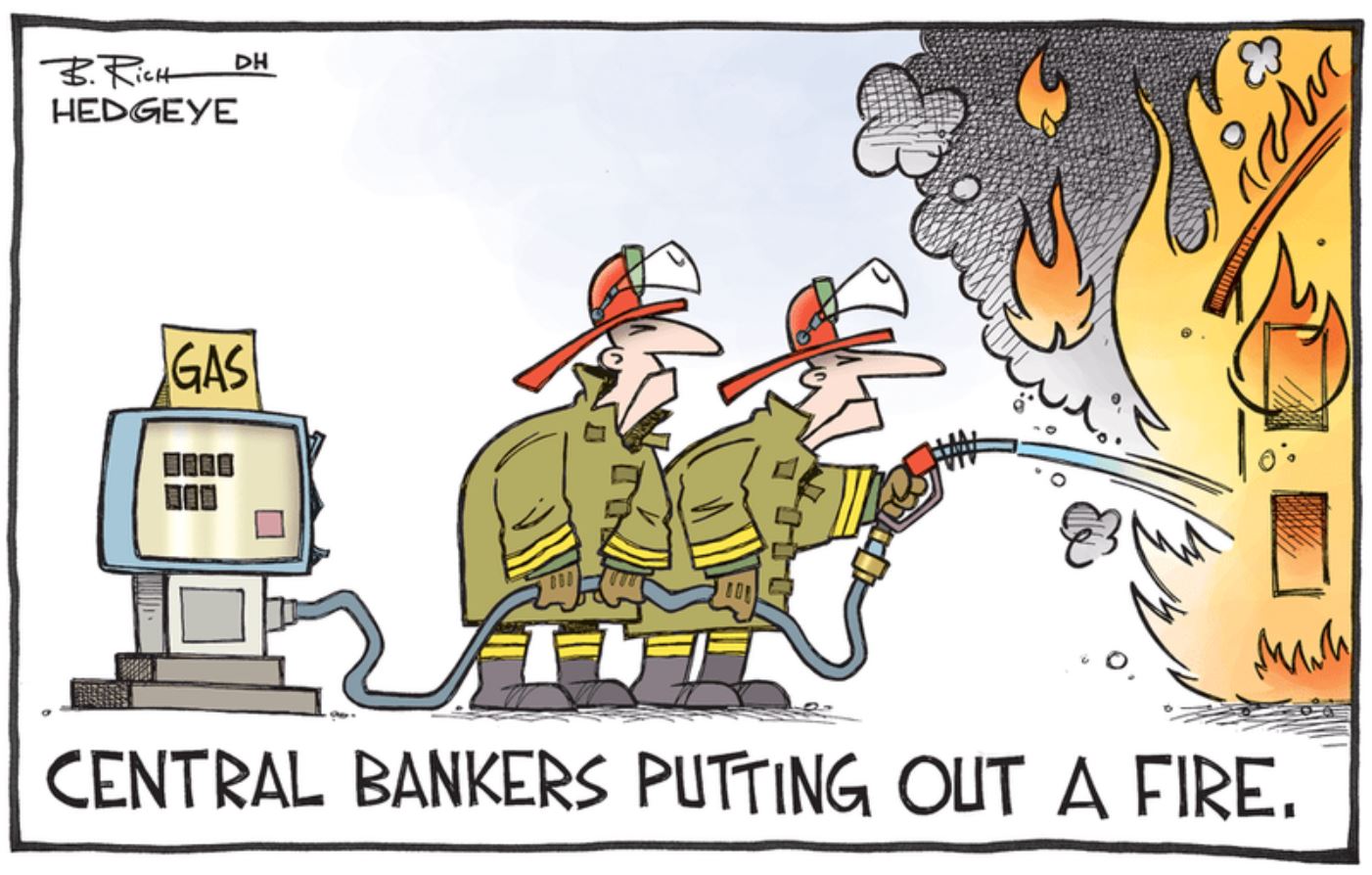

Road to reflation started with stimulus and likely to end with currency debasement

Local market had a negative day on low turnover as global investors were selling into AUDUSD weakness. Macro asset allocation trade from bonds to equities seems to coming to an end after Blue Wave. US 10 year bond yield is now 1.12% and above Aussie 10 year bond yield while AUDUSD has fallen from above 78 cents to below 77 cents. Energy was the only positive sector and Utilities was flat while the rest were in the red. Tech was hit the hardest while Staples, Industrials and Health Care were the next batch on the hit list. US 30 year bond yield is now delivering better yield that S&P 500 and above inflation. Reflation genie is out and the economy need stimulus. More stimulus means more inflation. The economy and the markets are like drug addicts waiting for the next hit…expect a temper tantrum if there are any delays!

US corporates have been reading the tea leaves of change in the economy for longer than markets like to give them credit. Self interest and survival are strong motivation for change. The first sign of US corporate deleveraging cycle has been triggered. After decade of money printing to provide a cheap way for them to deleverage, it was nothing short of a global pandemic recession to deliver the change. Markets will soon move from stimulus hope to higher taxes and regulations in a reflationary environment. We would expect that the deleverage cycle will start to pick up steam with reflation. US corporate growth cycle has been all about leverage and that cycle looks to be turning.

History suggests all road to reflation starts with short term stimulus boost in a crisis. The inability of the leaders of the time to deliver strong reform and evolve the economy after the recovery cycle means that it becomes an endless stimulus binge that leads to currency debasement with asset bubbles. As with all ponzi schemes, it works till it doesn’t. Everything looks good while you have strong economic growth and debt growth. Then you start to see structural economic problems drive the economy to a weak state and that leaves it susceptible to getting knocked down by a left field event like a pandemic. Sounds familiar…Japan has been there for decades, Europe is well set up for decades of grinding low growth pain while US is in denial that it has entered a reflation sandpit. The reflation sandpit is the bear trap for equity markets. The solution is simple…massive wealth redistribution and massive reform…but executing it will hurt vested interest groups and the markets in the short term. Pandemic waves, unvetted tax cuts and unvetted stimulus handouts have been like a steroid boost for inequality. “Blue Wave” political pressure will have US deliver substantial money printing to support the economy through the cycle. The fiscal reality will deliver higher tax on wall street and wealthy to pay for handout on main street. US must reflate their way out of debt and there will be winners and losers. Recent history is not a good indicator of future winners and losers in the US economic cycle!!!

US market last close > US market had another macro move from bonds to equities day to squeeze out a weak positive day. All indices started slightly positive and then fell into decent negative area as nonfarm payrolls confirmed fading recovery before pump in the last hour pulled it back to positive finish. Nonfarm was expected 50k up but was 140k down... in line with ADP data drop... that makes first negative data since pandemic started. Risk off trade mainly with bond yields, USD and NASDAQ were best...Russell and metals were negative. NASDAQ pop is driven by Baidu up 16% and Tesla up 8%. US 10 year yield above 1.1%...the bonds are better risk/return now. Trump has decided not to turn up to inauguration and Democrats are moving to impeach while Trump needs to survive to pardon a lot of people in the next few weeks. US is now getting hit hard with new pandemic variant waves as more parts of the world falls into restrictions of lockdown…even China is affected. Japan is supposedly found their own variant. Just what we need…more diversity in virus! Pandemic is going to drive short term downgrades while reflation is out and proud. Bonds long term yields are better than inflation and equity div yields.

Remain nimble, contrarian and cautiously pragmatic with elevated global macro risks!!! Buckle up...it’s going to get bumpy!!!

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and CEO at Deep Data Analytics (www.deepdataanalytics.com.au) which is an integrated data analytics driven investment strategy service provider.

........

Deep Data Analytics provides this financial advice as an honest and reasonable opinion held at a point in time about an investment’s risk profile and merit and the information is provided by the Deep Data Analytics in good faith. The views of the adviser(s) do not necessarily reflect the views of the AFS Licensee. Deep Data Analytics has no obligation to update the opinion unless Deep Data Analytics is currently contracted to provide such an updated opinion. Deep Data Analytics does not warrant the accuracy of any information it sources from others. All statements as to future matters are not guaranteed to be accurate and any statements as to past performance do not represent future performance. Assessment of risk can be subjective. Portfolios of equity investments need to be well diversified and the risk appropriate for the investor. Equity investments in listed or unlisted companies yet to achieve a profit or with an equity value less than $50 million should collectively be a small component of a balanced portfolio, with smaller individual investment sizes than otherwise. Investors are responsible for their own investment decisions, unless a contract stipulates otherwise. Deep Data Analytics does not stand behind the capital value or performance of any investment. Subject to any terms implied by law and which cannot be excluded, Deep Data Analytics shall not be liable for any errors, omissions, defects or misrepresentations in the information (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the information. If any law prohibits the exclusion of such liability, Deep Data Analytics limits its liability to the re-supply of the Information, provided that such limitation is permitted by law and is fair and reasonable.

Copyright © Deep Data Analytics. All rights reserved. This material is proprietary to Deep Data Analytics and may not be disclosed to third parties. Any unauthorized use, duplication or disclosure of this document is prohibited. The content has been approved for distribution by Deep Data Analytics (ABN 67 159 532 213 AFS Representative No. 1282992) which is a corporate approved representative of BR Securities (ABN 92 168 734 530 and holder of AFSL No. 456663). Deep Data Analytics is the business name of ABN 67 159 532 213.

1 topic

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and...

Expertise

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and...

Expertise

Comments

Comments

Sign In or Join Free to comment