ASX 200 futures are trading 4 points higher, up 0.05% as of 8:30 am AEDT.

The Dow and S&P 500 extend gains while the Nasdaq takes a breather, Morgan Stanley says the rally in tech stocks is not sustainable and expects the sector to return to new lows, US manufacturing tumbles to a three year low which triggered an uptick in bonds and gold, and the RBA interest rate decision will take place at 2:30 pm AEST (with expectations of the first pause since April 2022).

Let's dive in.

Source: Market Index

S&P 500 SESSION CHART

S&P 500 closes towards session highs after a choppy open (Source: TradingView)

MARKETS

S&P 500 closes towards session highs, up 3.9% in the last four sessions

Nasdaq underperforms but off session lows of -1.1%

US Dollar Index falls 0.5% to close at a two month low

Morgan Stanley says US tech rally overdone, valuations stretched (Bloomberg)

Bearish sentiment on stocks is the best thing rally has going for it (Bloomberg)

Hedge funds retrench after getting pummeled during wild March (Reuters)

STOCKS

General Motors (-1.1%): US sales jump 18% in the first quarter (CNBC)

Rivian (-1.6%): Misses Q1 production estimates, reaffirms 2023 target (Reuters)

WWE (-2.2%): Agrees to merge with the Endeavour-owned UFC (Reuters)

EARNINGS

US first quarter earnings season unofficially kicks off on 14 April.

JPMorgan and Citi are the first big banks to report

S&P 500 earnings forecast to fall 6.6% year-on-year in Q1, according to FactSet

This follows a 5.8% decline in Q4

Materials, healthcare and tech are sectors expected to lead the earnings decline

Discretionary and industrials expected to hold up the best

ECONOMY

US manufacturing near three-year low, casts a shadow over economy (Reuters)

OPEC cut could make the Fed’s job more difficult, says Bullard (Bloomberg)

China's factory activity grew at a slower pace in March 2023 (Reuters)

Japan business sentiment slumps to 2-year low as global slowdown bites (CNBC)

Australian home prices rise for the first time in a year in March (Reuters)

US home prices rise 0.2% in February, biggest monthly gain since May-22 (CNBC)

US-listed sector ETFs (Source: Market Index)

Deeper Dive

US manufacturing: Weakest in nearly three years

The ISM manufacturing PMI came in at 46.3, the lowest since May 2020, the month after the Covid recession ended.

According to Bianco Research, the have been 16 times where the ISM was come in below 46.3. 12 or 75% of these instances, the US economy was either in a recession or about to enter a recession.

The PMI report was weak across the board, with new orders down 2.7 pts to 44.3, the prices index fell from 51.3 to 49.2 and employment took a notable step down.

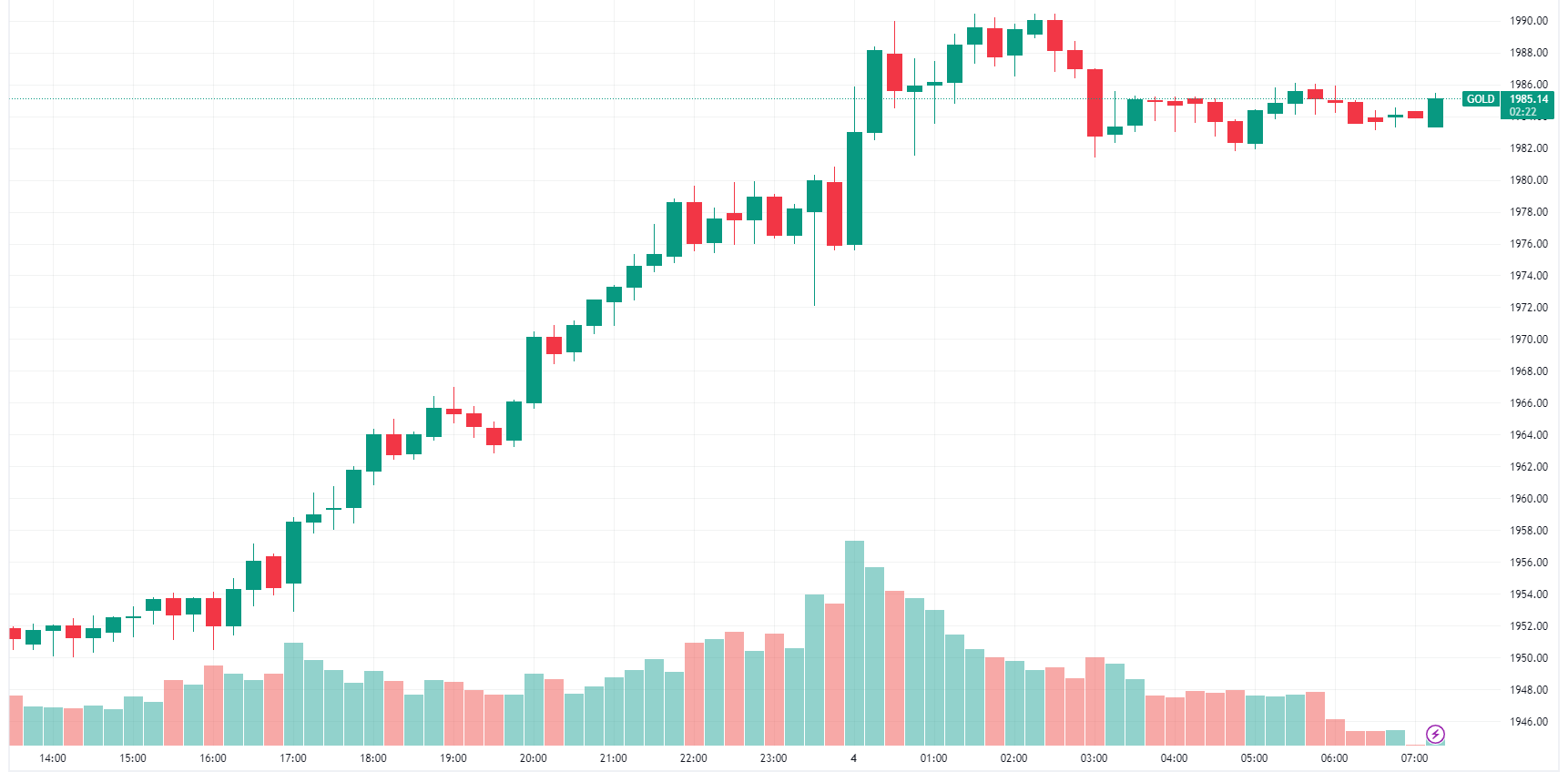

The weak manufacturing print has put the recession trade back into the spotlight, seeing an uptick in demand for bonds and gold. Gold was already in an intraday uptrend in the lead-up to the ISM print but experienced a notable spike at when the data came out at midnight.

Gold intraday chart (Source: TradingView)

RBA Preview: Expectations and what the data tells us

This afternoon's decision on interest rates is going to be a close call. As of yesterday, the Bloomberg survey of economists had 19 economists calling for a pause and 11 economists calling for a 25 basis points hike to 3.85%.

For those in favour of a pause, they look to the big drops in the monthly inflation indicator as well as plenty of evidence in the forward indicators that economic growth is slowing significantly.

For those in favour of a hike, they argue inflation is still three times the RBA's own target as well as ongoing upside risks for wage growth.

What everyone can agree on is that the labour market has remained much tighter than first thought - and that a reduction in interest rates is still quite far away.

For what it's worth, the market is expecting no rate hike tomorrow. To set the scene as to how the ASX 200 performs on rate hike days (referencing the start of the hiking cycle in May 2022):

2 larger-than-expected hikes last May and June and ASX 200 fell -0.42% and -1.53% respectively

7 hikes in-line with expectations and the ASX 200 rose an average 0.12%

1 smaller than expected hike last October and the ASX 200 surged 3.5%

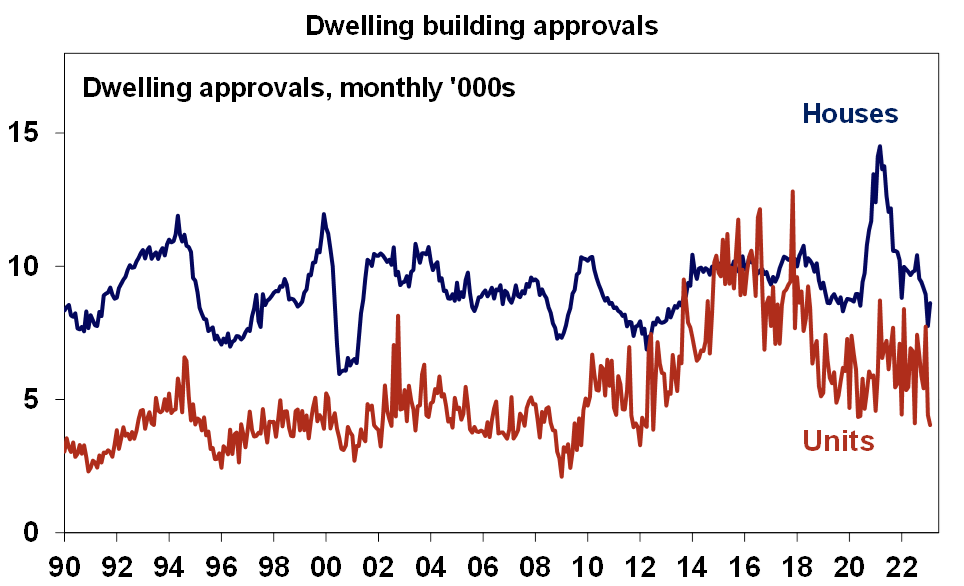

Another reason to pause: Tumbling building approvals

Our chart comes from the newly anointed Deputy Chief Economist at AMP (and Signal or Noise series regular) Diana Mousina. Another argument in favour of a pause is the state of building approvals. Most economists expected a rebound from last month's 27% collapse. Not everyone expected those approvals to rise by only 4% in February. It suggests activity is still low because of the higher cost of borrowing and an increase in building materials costs. Remember, less approvals means less supply - and that's not what prospective home buyers need to hear.

Gold: Spot prices rallied 0.8% from session lows of -0.95% thanks to the ISM print. The local gold sector was relatively heavy on Monday, with most names down around 1-4%. Can the overnight reversal see some positive flow for local goldies?

Tech: There was a slight risk off tone to the overnight session, with the Nasdaq underperforming the S&P 500 and Dow. Risk barometers like the ARK ETF and Bitcoin also eased. The ASX 200 Info Tech Index is up almost 5% in the last four sessions, so do we see a bit of a pullback take place?

Energy: Its been a day since OPEC announced the unexpected supply cut. Woodside was incredibly choppy on Monday, closing 2.7% higher from session highs of 5.9%. Is the market going to prioritise a) the face value cut aka less supply and higher prices or b) cutting as a symbol of demand weakness?

Broker Watch

Speaking of the challenging labour market, mining services companies have had a rough time over the last three years finding staff. That construction worker shortage very much still exists despite a strong pipeline of infrastructure project approvals and the generally solid commodities cycle.Goldman Sachs has run its ruler over the four ASX stocks exposed to the mining services industry. Here are their verdicts:

BUY for ALS Limited (ASX: ALQ) and Seven Group Holdings (ASX: SVW). Both have approximately 21% target price upside baked into their forecasts.

NEUTRAL on Downer EDI (ASX: DOW). The business has a defensive profile and a long-term exposure to decarbonisation thematics. But in the short term, they really need people.

SELL on Monadelphous (ASX: MND). Along with those staffing issues, CAPEX is stalling at the company which isn't good news for its immediate earnings runway.

This Wrap was first published for Market Index and written by Hans Lee and Kerry Sun.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire and Market Index's pre-opening bell news and analysis wrap. Available weekday mornings and written by Kerry Sun.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies (“Livewire Contributors”). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

Sign In or Join Free to follow and be notified when I next publish