Sector and themes to watch in 2021

The most confounding thing about financial markets in 2020 was that, in totality, the mood of the global equities market seemed completely different than the mood of everything else happening to humanity — i.e., millions of lives lost worldwide, ongoing concerns for health and employment, political instability, racial injustice, and the list goes on.

The MSCI World Index in the calendar year delivered a positive return of almost 16% (trading in a 46% range after a year-to-date low of -30% at the end of March) while the annual earnings of companies within the index are expected to have fallen by 7%. This represents a price-earnings multiple expansion of around 25%.

During 2020, the price appreciation of public equities reflected a high level of optimism about the ability of the global economy to recover from the pandemic and come out stronger than before. In 2021 we believe that the listed price of publicly traded companies will more closely tie to the underlying near-term earnings trajectory and financial strength of those companies.

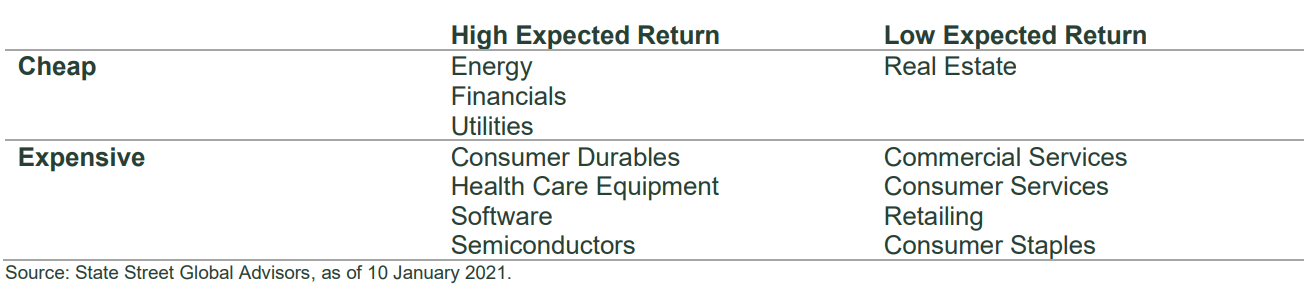

While valuation is an important theme when we select stocks, we find attractive stocks at both ends of the price-tobook valuation spectrum. There are cheap stocks we like, and there are cheap stocks we don’t like; expensive stocks we like, and expensive stocks we don’t like. Among stocks that look expensive as measured by price-tobook ratio, we see a subset as attractive once we conduct a nuanced analysis of where they derive their value. For example, in developed markets tech hardware and semiconductors have average or slightly above average value scores according to our proprietary value measures, despite being extremely expensive on price-to-book alone. Figures 1 and 2 show that we expect high returns to be found among both cheap and expensive stocks.

Figure 1: Developed Market Sector Return Expectations, by Sector Valuation

Figure 2: Emerging Market Sector Return Expectations, by Sector Valuation

Price Momentum

During 2020 we discussed concerns regarding market concentration in expensive and high-momentum stocks, and we are still concerned about companies that may, due to their size, impact market indices in aggregate if they pull back. Figure 3 shows that the embedded price momentum built into the S&P 500 over the past few months reached levels not seen since the height of the dot-com bubble.

Figure 3: Embedded Price Momentum in S&P 500 Index (11-month return, lagged one month)

Opportunities in 2021

Since market concentration in expensive, high-sentiment stocks reached all-time highs last August, some out-offavor stocks are showing some signs of improving sentiment — and creating better opportunities for us to find companies that tick all the boxes. In aggregate, the following segments are where we see the greatest opportunity with a nine- to 12-month horizon.

The Bottom Line

After a year of high optimism in equities markets — an optimism that often seemed disconnected from the year’s many challenges — we believe that equity prices will increasingly reflect underlying fundamentals in 2021. Multiple expansion will not be enough. Our nuanced assessment of value in context with other key investment themes, including sentiment and quality, points to opportunity among both cheap and expensive stocks. Although market concentration in stocks benefiting from extraordinarily high price momentum remains high, some out-of-favor stocks are displaying improving sentiment, widening the range of stocks that are attractive across multiple themes and dimensions of investment performance.

We stand on the threshold of a new investment reality as COVID vaccines roll out and monetary and fiscal conditions change in response to a global economic recovery. In 2021, we believe our investment process, which uses a balanced set of attributes to select stocks, will be well positioned to capture the opportunities that markets will offer in this new environment.

Access high quality companies at attractive prices

Rather than building portfolios around the stocks weights represented in the benchmark index, our approach explores the market’s full opportunity set, constructing a portfolio based on stocks total return and total risk characteristics. Click to follow button to stay up to date with all our latest insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Many people think equity investing is all about finding companies that offer the best returns. We’re focused on the best way to form equity portfolios to deliver the best risk-adjusted returns, in line with specific return and risk objectives. Our experience is in applying our investment knowledge across as many companies as possible in a highly objective way.

........

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor. All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

The views expressed are the views of Active Quantitative Equity through December 10, 2020 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Investing involves risk including the risk of loss of principal. Quantitative investing assumes that future performance of a security relative to other securities may be predicted based on historical economic and financial factors, however, any errors in a model used might not be detected until the fund has sustained a loss or reduced performance related to such errors.

The trademarks and service marks referenced herein are the property of their respective owners. Third-party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

© 2020 State Street Corporation.

Many people think equity investing is all about finding companies that offer the best returns. We’re focused on the best way to form equity portfolios to deliver the best risk-adjusted returns, in line with specific return and risk objectives. Our...

Expertise

Many people think equity investing is all about finding companies that offer the best returns. We’re focused on the best way to form equity portfolios to deliver the best risk-adjusted returns, in line with specific return and risk objectives. Our...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The most consistent ASX dividend stocks

Livewire Markets

Equities

Buy Hold Sell: 5 ASX names built for income

Livewire Markets