Should we fear a tidal wave of mortgage resets?

In meeting with clients over recent months, one of the common questions I’ve been asked has concerned the potential “income shock” to be faced by households given the apparently large number of interest-only mortgage loans that may need to be reset into principal and interest loans over coming years. This note suggests that while this shock may well be a challenge for some households, overall this adjustment is not likely to pose major downside risks for the economy.

Almost a million households face a looming potential income shock

Media headlines try to be dramatic, and one of the most dramatic headlines in recent months has been the spectre of more than one million households facing a potentially steep increase in home loan repayments over coming years as their IO loan periods expire and their loans convert to principal and interest (P&I) loans.

There’s been a lot of numbers bandied about, and what follows is my own break-down of the relevant metrics that I think need to be considered – using data pieced together from Reserve Bank research*.

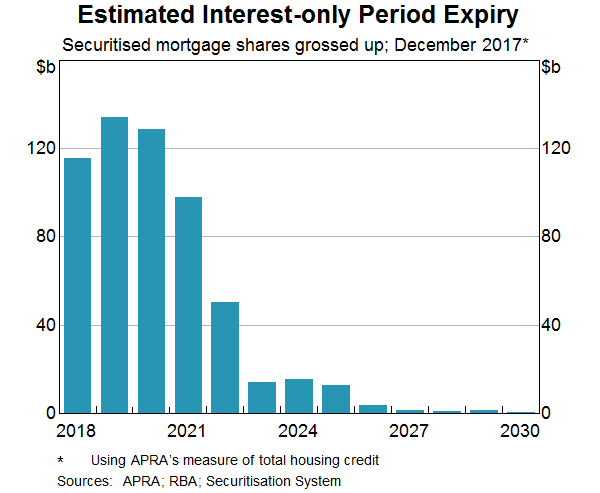

At face value, the numbers appear frightening and some concern is understandable. For starters, just over 30% of the $1.7 trillion outstanding home loans (investor plus owner occupier) are IO loans, and around two thirds of those – worth round $350 billion – are scheduled to be converted into P&I loans over the three years to end-2020. As seen in the chart below, this amounts to around $120 billion in loan conversions each year.

For the households concerned, the payment shock could be significant. Assistant RBA Governor Christopher Kent noted a “representative” household facing such a mortgage reset could have a loan of around $400,000 payable over 30 years. Assuming an interest rate of 5%, the annual repayments on an initial 5-year IO loan period would have been $20,000 per year. Annual payments on a P&I loan over the remaining 25 years – assuming the same interest rate – would jump to $28,000, or $26,000 if the remaining loan period were re-set at 30 years.

Either way, that’s a jump in payments of around 30 to 40%! With $120 billion re-set each year and assuming an average mortgage of $400,000, it implies around 300,000 households could face such an income shock – worth $2.1 billion in aggregate – each year for the next three years.

Hence the nasty headlines.

The nation-wide income shock should be contained

So far so bad, but how do these numbers compare against the aggregate size of the economy? It turns out the aggregate income shock could be at worst a flesh wound.

How so? For starters, it’s worth remembering we’ve got a $1,800 billion economy and around 10 million households. So it already implies only around 3% of households would be affected by these mortgage re-sets in any given year – and about one in ten over three years.

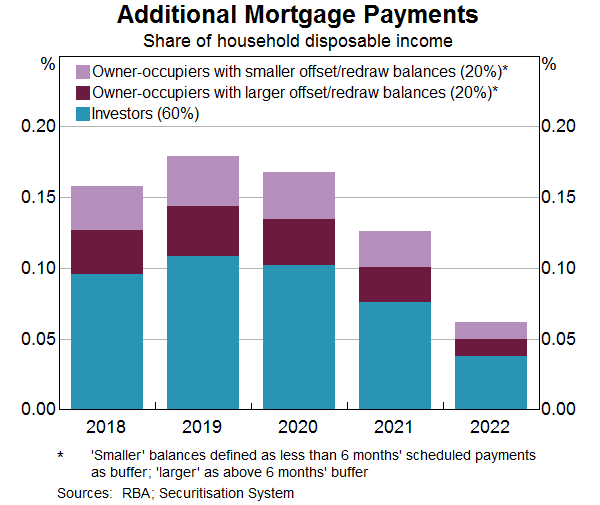

Total annual household disposable income is currently around $1,200 billion. So a total aggregate household income shock of $2.1 billion amounts to around 0.18% of household income each year. What’s more, about 60% of these re-sets would affect investors rather than home-owners – who in general have higher levels of income and wealth and might be better able to manage the higher repayments.

The RBA’s specific estimates are outlined in the chart below.

By David Bassanese | 22 August 2018

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Ilan was a founding team member of BetaShares and is responsible for corporate & product strategy. Previously, Ilan worked for The Boston Consulting Group (BCG), one of the leading global strategy consulting firms.

Ilan was a founding team member of BetaShares and is responsible for corporate & product strategy. Previously, Ilan worked for The Boston Consulting Group (BCG), one of the leading global strategy consulting firms.

Expertise

Ilan was a founding team member of BetaShares and is responsible for corporate & product strategy. Previously, Ilan worked for The Boston Consulting Group (BCG), one of the leading global strategy consulting firms.

Expertise

Comments

Comments

Sign In or Join Free to comment