One stock you can’t live without?

Globally there are over 112 million American Express cardholders. According to Interbrand, American Express is the 23rd most recognised brand globally, ahead of companies such as Pepsi, Gucci, Porsche and, somewhat surprisingly, both Visa and Mastercard. With a market capitalisation of over US$110bn it is a global behemoth. Interestingly, at last reporting date there were only 21,078 shareholders. Far more people have the Amex card than shares in the parent, and while owning the card has its rewards, we suspect owning shares in the company over the long term has been the more rewarding experience, with earnings per share increasing more than 22 fold over the last 32 years. The company continues to expand its presence globally, including in Australia. In this article we explain why American Express is a significant shareholding in the Auscap Global Equities Fund.

The Origins of American Express

American Express was founded in 1850 by Henry Wells and William Fargo (who also founded Wells Fargo bank), commencing operations as an express mail business in New York. For years American Express had a monopoly for express shipments through New York. Its evolution into financial services began in 1857 with the launch of a money order business to compete with the US Post, followed by travelers cheques in 1891.

Diners Club introduced the world’s first travel & entertainment charge card in 1950, however its monopoly was short-lived with American Express leveraging its brand to launch a premium card in 1958 with a $6 annual fee relative to Diners Club at $5. American Express’ card attracted 250,000 customers prior to launch date and 1 million customers within five years.

American Express has since evolved with the launch of the Gold card in 1966 which offered superior customer service and membership of the American Express club, the Platinum Card in 1984, originally by invitation only, and then in 1999 the “black card” or Centurian Card which is available to more affluent customers. Today American Express’ brand strength as measured by independent third parties is the strongest of all financial services companies.

American Express Business Overview

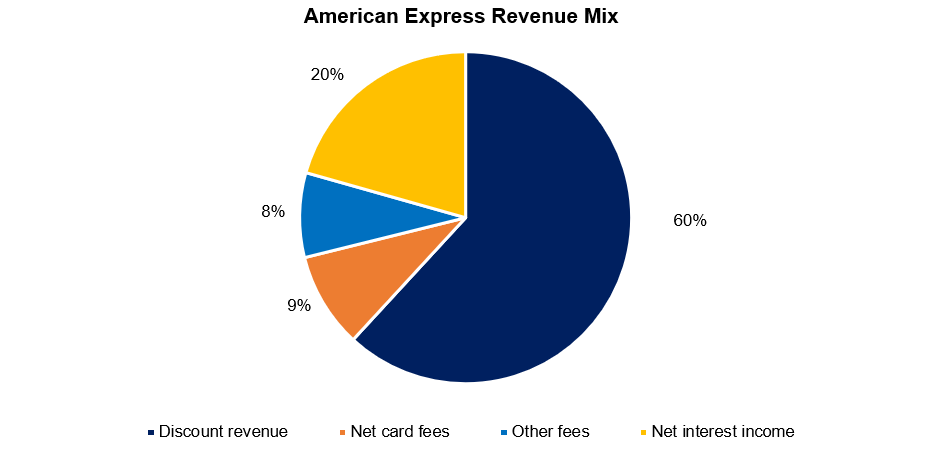

American Express operates what it calls a “spend-centric” business with circa 80% of revenue derived from fees and customer spend, called “discount revenue” where fees are charged to merchants for accepting American Express, and the remaining 20% of revenue being derived from net interest income.

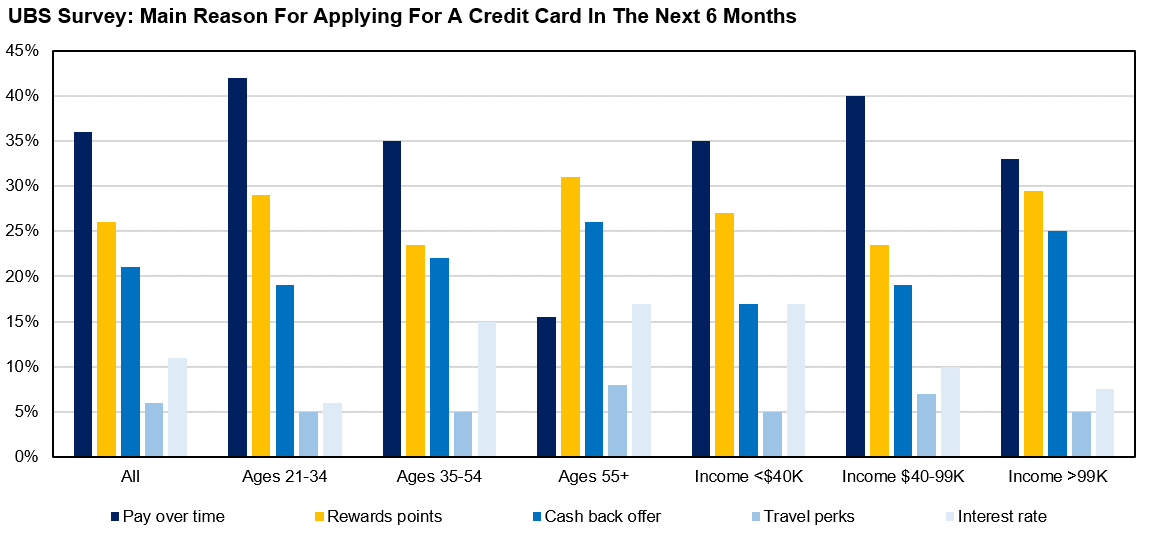

American Express’ business has a flywheel effect, where high quality rewards attract high quality customers that in turn attract merchants. According to a UBS survey, rewards points are a critical factor for choosing between various credit card options, particularly for younger and higher socio-economic demographics, both of which are American Express’ target customers.

The quality of American Express’ customer base has also improved over time given the popularity of charge cards. Charge cards have an annual fee, but no pre-set spending limits or interest charges, with balances paid at end of each month. Customers like the rewards and the cards are an easy substitute for cash. Given these customers have historically been of better creditworthiness this has improved average credit performance of the business as well as overall spending per customer.

American Express’ high-quality customer base leads to an average annual customer spend ~3x higher than competitor cards as well as market-leading credit performance. American Express has an average customer FICO credit score of 740 which is considered “very good” by credit bureaus. This growing customer base has also driven greater merchant acceptance over time, with American Express now on parity with Visa & Mastercard for acceptance in the United States.

The company has a long term track record of lifting spend per customer, achieved via:

- increased card usage, with ~60% of annual loan growth coming from existing customers;

- positive product mix shifts, predominantly from upgrading customers to higher tier cards; and

- fee increases associated with greater reward offerings.

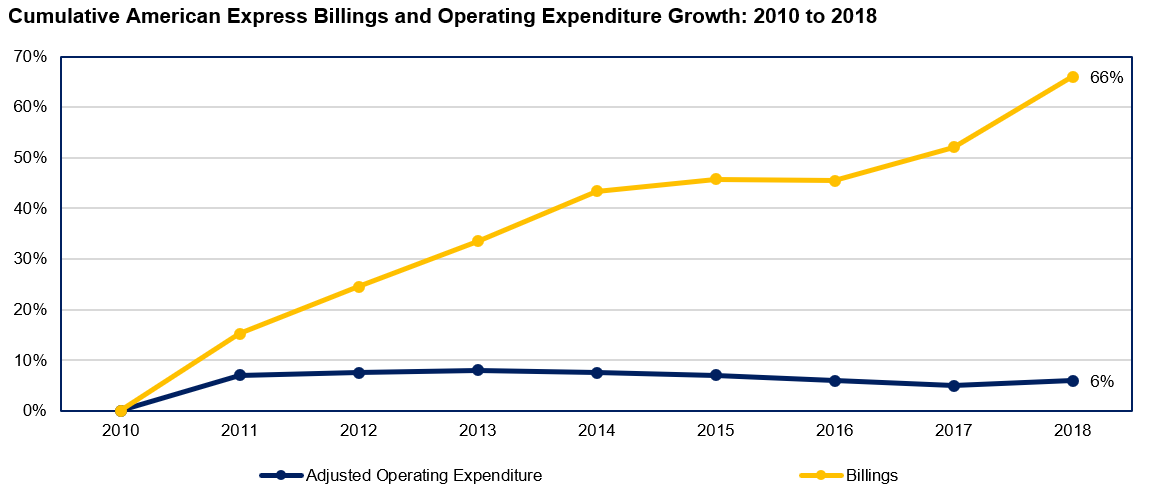

American Express has also been able to deliver consistently strong operating leverage and maintain a sector-leading return on equity. Since 2010, the company has lifted billings by 66% while expenses have increased by only 6%. This operating leverage combined with continued share-buy backs, which have reduced shares on issue by nearly 40% since 2000, have driven its strong return on equity.

* American Express definition of normal business operating expenditure excluding reward costs, see American Express investor presentation dated 13 March 2019

Drivers of Medium-Term Earnings Growth

American Express has multiple levers to underpin its solid double-digit earnings growth outlook over the medium term. These include:

1. Greater Offshore Penetration

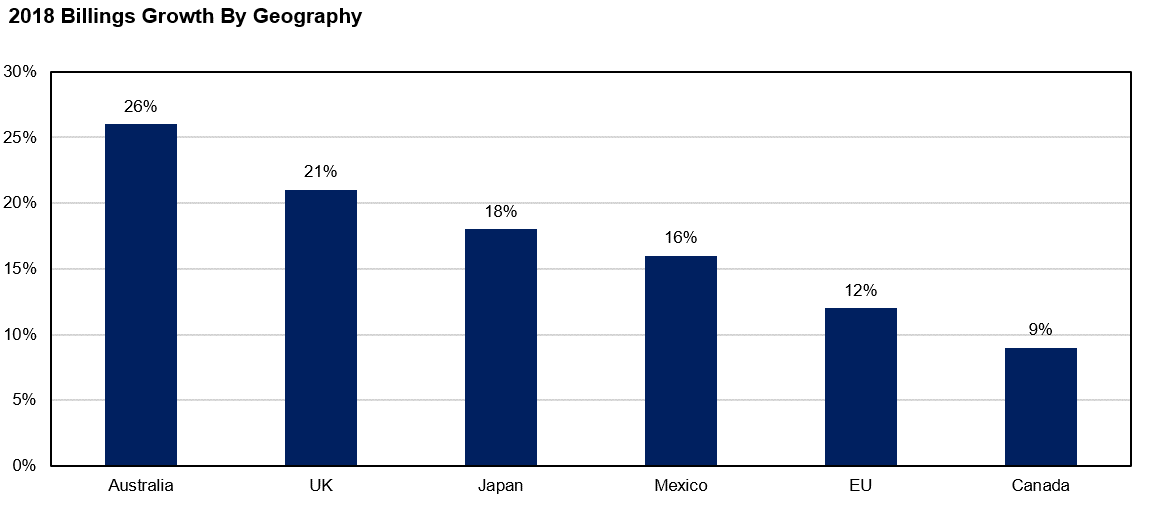

American Express is aiming to take its US learnings and apply them offshore. Management have identified the United Kingdom, Canada, Japan, Australia and Mexico as key growth opportunities. American Express is also the first non-China based network to receive preparatory approval to build its business in China.

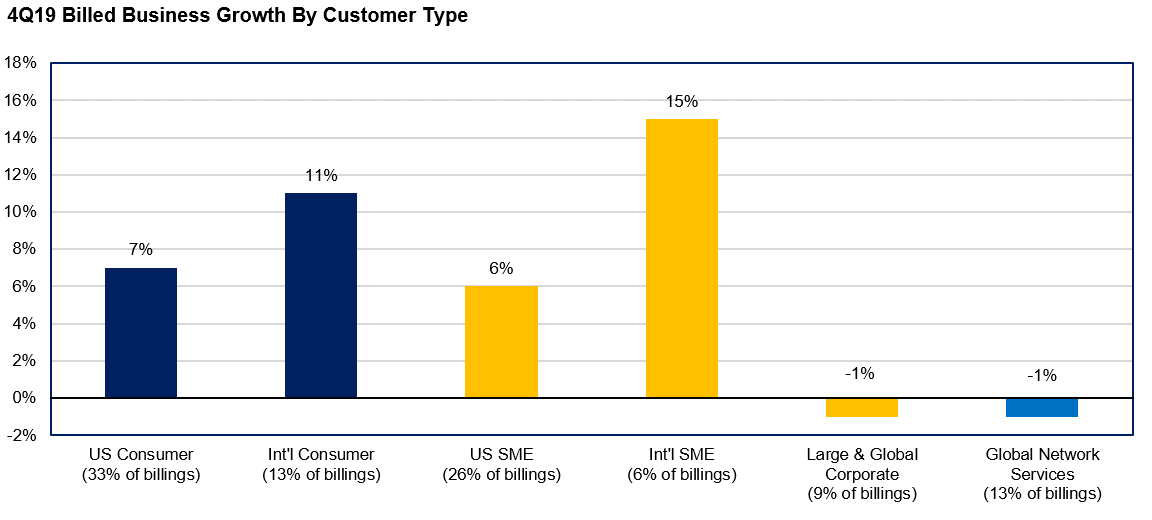

American Express’ aim is to increase international coverage by approximately 20% from 2019-2021. As evidenced in the following chart, the company is already making good progress. American Express’ low market share and the more favourable competitive environment in each geography should provide a long runway for growth. International markets are currently just a quarter of group earnings, despite international markets representing over 70% of global payments.

2. Small & Medium Enterprise (SME) & Corporate Expansion

American Express serves over 3 million businesses and has 14.5 million card members in the commercial sector. In the US SME market, it is the leading issuer of cards and larger than its nearest five competitors combined. International SME is currently the fastest growing segment within the company. With circa 70% of Business to Business (B2B) payments still completed using cheques, American Express believes it has a long-term structural growth opportunity.

The company has been able to accelerate growth in this segment more recently via the introduction of its Account Payables automation solution, which provides an online portal that enables payments to third parties. American Express is seeing a 43% lift in spending from US SME consumers who adopt this solution. The company also sees opportunities in entering the working capital segment.

3. Greater Co-Brand Partnerships

American Express has more than 50 co-branded partners around the world. These include over 20 airline partnerships, with leading operators such as Qantas, Singapore Airlines, British Airways and Delta. Recently Amazon selected American Express as their co-brand business card partner in the US.

4. Opportunities Within Existing Customers

American Express sees a large untapped opportunity within its existing customer base, who currently account for approximately 60% of loan growth. In 2018 there were over 1 million upgrades and additional products facilitated for existing customers. The result was a 30% lift in spending when customers upgraded their product and a 40% lift when they added an additional product.

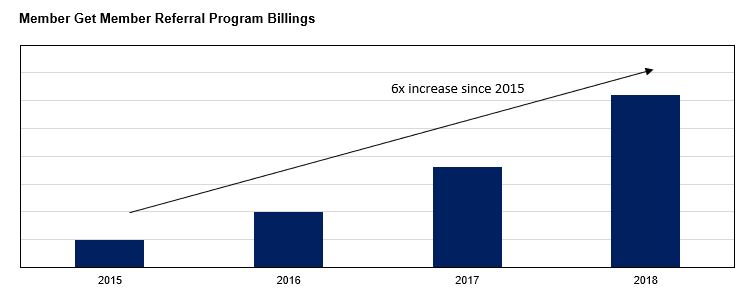

Existing customers also play a crucial role in expanding the customer base. The “Member get Member” referral program is the company’s second largest acquisition channel globally. It is a cost-effective form of marketing and will typically attract quality customers who have similar attributes to their referees. 33% of those who were successfully referred to under this program successfully referred someone else.

Alignment of Interests

Agency costs, where management interests do not perfectly align with shareholders, can result in behaviour that can be costly for shareholders. As a result, having structures in place that increase the alignment of interests is important. At American Express there is a requirement for any board member that has been on the board for more than 5 years to own at least US$1m of American Express stock. Currently the Chief Executive Officer owns circa US$28m worth of shares. Further, the executive compensation scheme has a greater focus on long term incentives (LTIs) rather than short term incentives (STIs), with LTI targets twice the size of the STIs and based on 3-year financial and total shareholder return metrics.

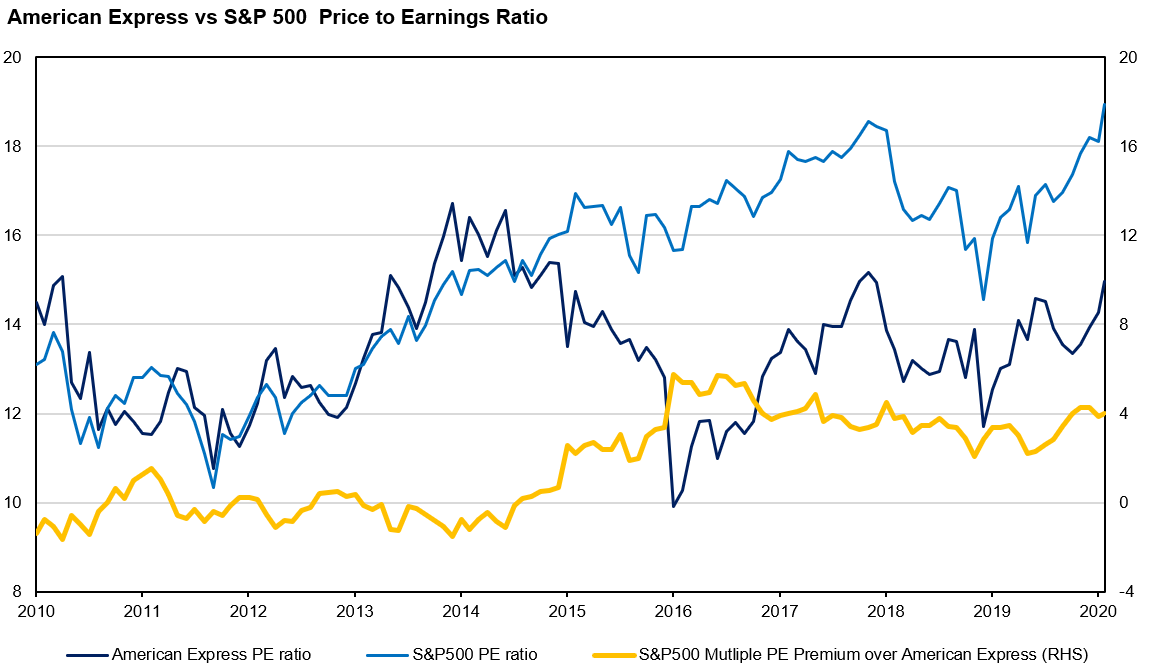

Valuation

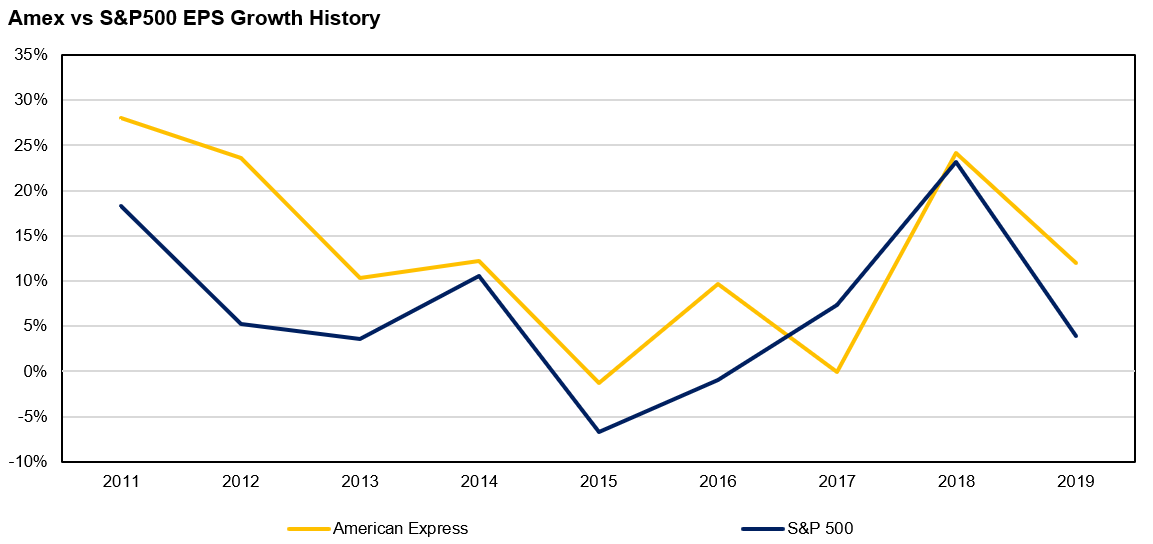

American Express has, in all but one year over the last decade, demonstrated superior earnings growth compared with the broader US market.

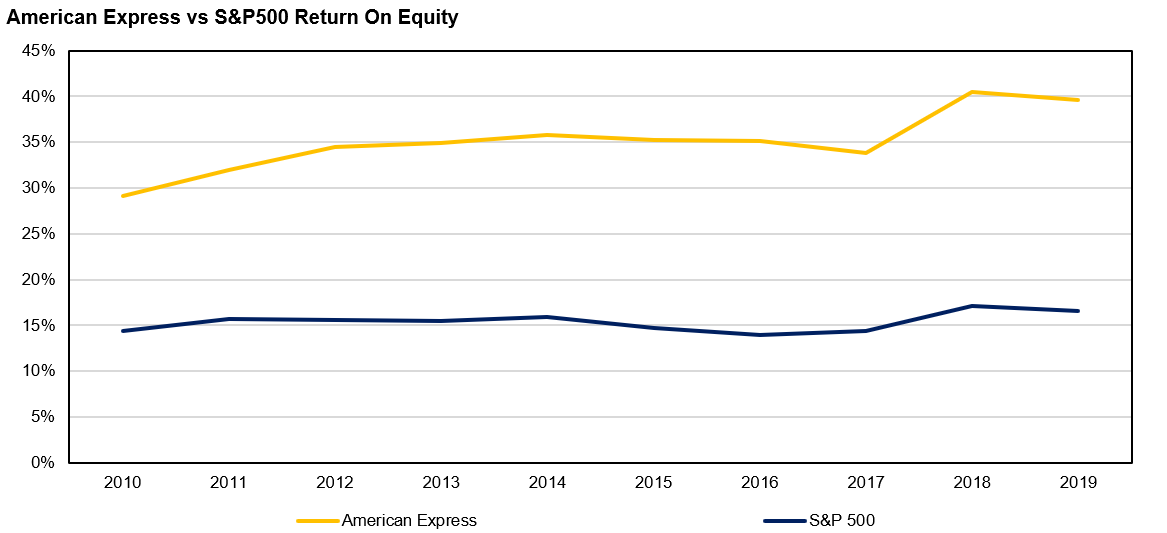

Its historical return on equity is impressive, averaging 35% over the last decade, demonstrating the quality of the business.

Despite these characteristics, American Express currently trades on less than 15x forward earnings, a discount to the broader market. With a medium-term outlook for double-digit earnings growth per annum, a long-term demonstrated track record of shareholder value creation and an impressive current return on equity of 40%, we regard a price to earnings multiple of 15x as attractive for a company of the quality of American Express.

American Express has many qualities that we look for in an investment. It is a globally leading and trusted brand with a long-term track record of solid earnings growth, high cashflow conversion, a strong return on equity and an attractive valuation. It is one of Auscap’s top ten holdings in the Auscap Global Equities Fund.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short portfolio using Proprietary funds. Prior to 2007 he worked at Macquarie Bank within the Investment Banking Group. Tim is a CFA charterholder, a CMT charterholder, a Senior Associate of FINSIA, a Graduate of the Australian Institute of Company Directors (GAICD) and has a Bachelor of Laws (Hons) from the University of Sydney and a Bachelor of Commerce from the University of Sydney.

........

Tim Carleton is a Principal and Portfolio Manager at Auscap Asset Management (Auscap), a boutique equities long/short investment manager. This article contains information that is general in nature and does not constitute investment or any other form of advice. This article does not take into account the objectives, financial situation or needs of any particular person nor does it constitute a recommendation to be relied upon when making an investment or any other decision. You need to consider your financial needs before making any decision based on the information in this article and a person should obtain and consider the relevant disclosure document before deciding whether to invest in an Auscap fund. No part of this article is to be reproduced or disclosed without the prior written consent of Auscap. In relation to any MSCI data in this article, the MSCI data is comprised of a custom index calculated by MSCI for, and as requested by, Auscap. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short...

Expertise

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short...

Expertise

Comments

Comments

Sign In or Join Free to comment