Six burning questions on investors' minds right now

COVID-19, the black swan event virus that heralded the end of the sharemarket’s longest bull run ever, has led to extreme volatility and some of the biggest market moves in history. In response, central banks and governments have promised to do ‘whatever it takes’ to support their economies. Monetary policies including emergency interest rate cuts and quantitative easing have been announced, as well as massive government stimulus including potentially ‘helicopter money’ in the United States. Markets hate uncertainty, and currently many variables are unknown. However, in time the virus should be contained, and markets are expected to recover. In this wire, we answer six frequently asked questions to help you navigate these challenging times.

1) Should you sell your shares?

For investors in quality businesses who have a long-term time horizon, the answer is often no. This is because selling out after a major market correction crystallises a loss that is currently unrealised. However, it will always depend on investors’ circumstances. For some investors, their need for liquidity or a change to their risk appetite means that a sale of shares is required. The emphasis is on ‘quality’ when making the decision to sell or hold. The severity of the impact of the COVID-19 containment measures on company cashflows will vary, and the reality is that some businesses will not survive. Some industries such as tourism, retail, and airlines are on the front line of this crisis and are likely to need life support from their governments to survive.

Companies with strong balance sheets, low levels of debt, and a strong management team are likely to outlast their competitors.

Before selling, investors should consider the prospects for the businesses they are invested in based on the best information available today, disregarding the price they paid for the shares.

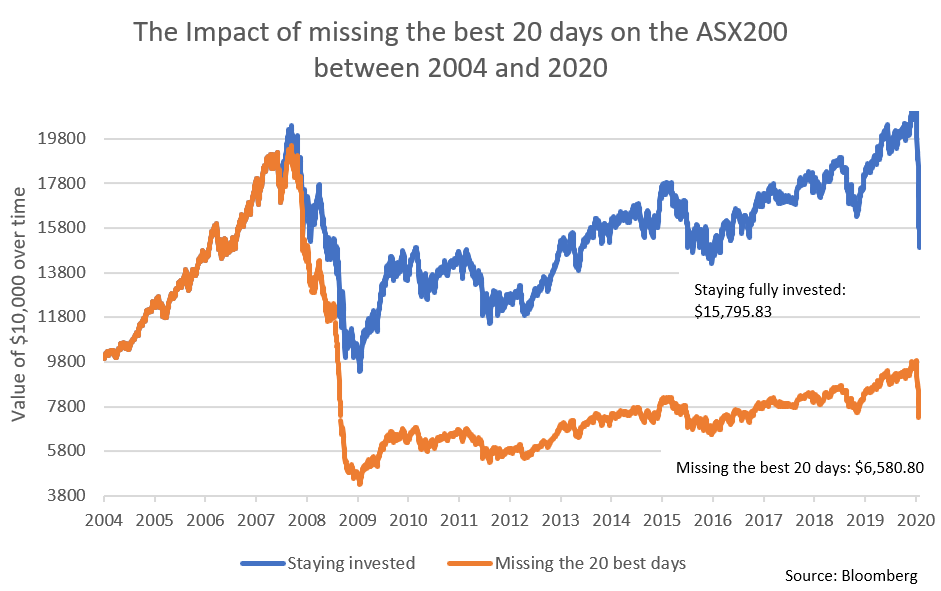

The rebound of share prices from previous recessions has been strong, and investors who exit today will miss out on the next rebound. Those who sell today may well realise a lower return over the long run than those who remain invested in a business that survives. As the chart shows, missing out on the 20 best days in the market between 2004 and 2020 would have resulted in a balance of $6,580 compared to a balance of $15,795 from an initial $10,000 invested in the ASX200. This is despite the ~20% fall we have seen over the last month.

The best returns in the market are often only days apart from the worst days. The table below illustrates this, with some of the greatest daily increases directly following the greatest falls.

Volatility during these periods means that markets can whipsaw as market participants react to new events. The table below illustrates this, with the worst days in the market often followed by a sharp move up shortly after. Electing to sell when volatility is at its zenith will mean missing out on both the good and bad days, and performance across different stocks and industries will vary.

2) Can I get access to my capital?

Yes. Despite the market volatility, liquidity in share markets has been strong, and has increased in the last few weeks. Those who wish to trade can generally do so, and daily turnover has been above normal. Although, those invested at the higher risk end of the sharemarket, such as in small and micro-cap stocks, may notice that the spread between the buy and sell prices has widened which does increase the cost to trade.

3) What types of equities should I own?

Companies with strong cashflows, robust balance sheets, and defensive positioning are expected to outperform during this period of volatility and should rebound when markets recover. A large part of the impact of COVID-19 appears to be priced into markets, although this is based on a best guess, and until a vaccine is found, the short and medium-term outlook continues to evolve.

During previous downturns, investors flocked to large-cap stocks to reduce risk during periods of market turmoil, whereas small-caps tend to receive flows when risk appetite returns.

4) Is it going to get worse?

As at 1 April 2020, Australian and global sharemarkets are currently ~25% cheaper than their highs on 19 February 2020. Although it is impossible to predict the bottom, on some measures, such as price/forward earnings, valuations are now at levels where markets are ‘cheap’.

However, as the economic impact increases and businesses struggle to maintain their cashflows, we expect to see more earnings revisions. Some companies are issuing downgrades merely weeks after issuing their earnings guidance for 2020. In some cases, guidance is being abandoned altogether. This uncertainty means that the market is moving more quickly than analysts’ coverage, and therefore investors who have decided that a stock is cheap based on current price/earnings (P/E) levels need to be mindful that the denominator may move lower. Earnings downgrades make relying on P/E valuations difficult until the path of future company earnings is clearer. Unlike other recessions, which have been driven by credit or liquidity crunches (which is also happening in some parts of credit markets currently), the differentiator here is the health issue and the uncertainty around how long it will last. Fiscal and monetary stimulus efforts can help to minimise the effects of a recession, but until the spread of the virus slows and the curve of infections flattens, the economic impact is difficult to model.

Once investors have this level of clarity, we expect pricing will reflect the fundamentals.

5) When should I buy?

Even for investment professionals, it can be difficult to know when to ‘buy the dip’. Markets tend to overreact on both the down and up swings, and the recent moves we have seen (falls of 20% in four weeks alone) indicate how fast markets can move. The market correction has provided opportunities to invest in some high-quality businesses at more attractive prices, but the returns may not emerge in the short term. Management teams that can adapt to the ‘new normal’ are more likely to put in place strategies that will set them up for long-term success. Currently the correlation of stocks across the market is high and the selloff has been indiscriminate as share prices react more to macroeconomic news rather than individual company fundamentals. In time, we expect this will dissipate and ‘quality’ stocks should rise.

Buying at the bottom of the market is an impossible task and for those who do, it is mostly based on luck.

The adage of not attempting to ‘time the market’, can help investors to avoid buying too early or missing out. Instead, focus on the fundamentals of company earnings and stick to your long-term strategy. Sentiment is a major driver of returns in the short-term and ignoring the noise can be difficult, but the rationale for having a diversified portfolio across and within asset classes is for times like these.

6) Will share markets recover?

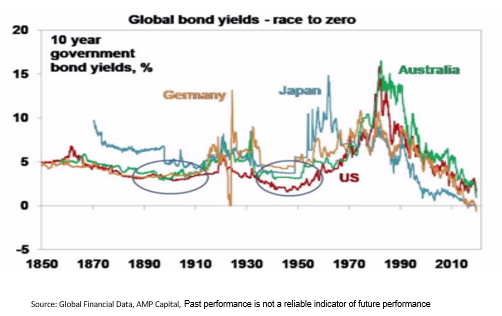

While we don’t know when the pandemic will end or the full impact on global supply chains and the global economy, we do believe that markets will recover. For sharemarkets, the rebound could be V- or U-shaped when the virus peaks, earnings expectations are clearer, and as investors consider the alternatives. As the following charts show, cash rates and bond yields globally are at historic low levels after emergency interest rate cuts over the last few weeks. Investors should once again look to increase their allocations to shares when the dust settles, and shares look attractive on a relative basis.

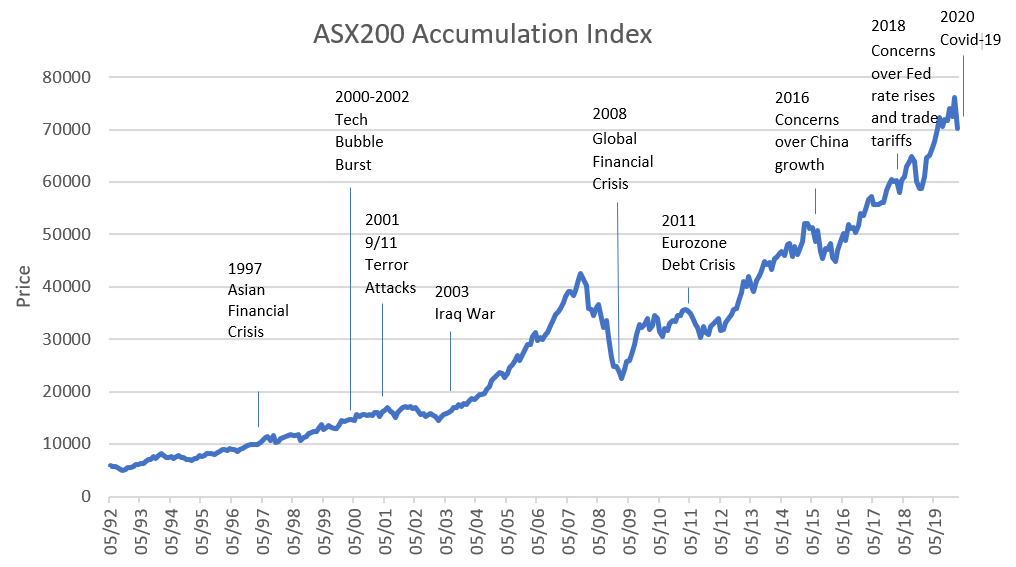

Many events have roiled markets in the past but looking at a long-term chart can provide some perspective. To quote Warren Buffett: "In the 20th century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. Yet the Dow rose from 66 to 11,497." NY Times 16 October 2008

In these extraordinary times, keeping a cool head can pay dividends.

Never miss an insight

Stay up to date with our latest thoughts by hitting the follow button below. You can also visit our website for more insights from Fidante's various boutiques. .

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Sinéad joined Fidante in January 2020 and has 17 years experience in the investment management industry. Her role is to serve as a conduit between the fund managers and the financial advisory community, with a special focus on retirement strategies.

Featuring

Sinéad Rafferty,

Fidante

Sinéad joined Fidante in January 2020 and has 17 years experience in the investment management industry. Her role is to serve as a conduit between the fund managers and the financial advisory community, with a special focus on retirement strategies.

1 topic

Sinéad joined Fidante in January 2020 and has 17 years experience in the investment management industry. Her role is to serve as a conduit between the fund managers and the financial advisory community, with a special focus on retirement...

Comments

Comments

Sign In or Join Free to comment