3 sustainable growth stocks outside the ASX50

Clime Investment Management

Clime Investment Management

The few large-cap growth stocks on the ASX tend to trade on steep premiums to the market. Therefore, investors seeking meaningful and sustainable growth are likely to find it outside the ASX 50. This report discusses a range of quality mid and small-caps as Clime analysts update company valuations post reporting.

Magellan Financial Group

We recently initiated a 1.0% position in MFG, buying 245 shares at $28.91 on the 7th of February. A key rationale for this investment is that the resilient performance of Magellan’s global equities strategies through the recent market volatility is likely position the business for strong retail inflows.

In early 2018, Magellan’s performance was looking good in an absolute sense, but tracking only in line with benchmark on a 5-year view. Combined with stronger performance from domestic competitors, this was translating to softer flows of new business, with net outflows in the retail space. However, this began to improve in the second half of the calendar and the global equities strategies performed particularly well through the market volatility in the December quarter. This outperformance is even starker when compared to key domestic competitors, such as Platinum and Antipodes. As a result, retail inflows have already begun to improve. In April 2018, Magellan reported -$64m of retail outflows and in January 2019 this had improved to +$110m of retail inflows. $110m equates to an annualised 6.7% of Magellan’s retail funds under management.

Together with Magellan’s full year result in August 2018, the company also announced an increase in the dividend payout policy to 90-95% of funds management net profit. This was effectively a 20% increase in the dividend and reflects the strong cash generation and very low capital investment requirements of the business. The stock has rallied by 14% since our investment, benefiting from a strong first half result, while it still offers a 5.4% dividend yield on Clime forecasts, which is expected to be 75% franked.

Magellan’s first half result beat consensus at the net profit line by 4%, reflecting better than expected fee revenue, lower costs and a lower tax rate. An added benefit of the improvement in retail flows is higher fee earning funds in the revenue mix, which should support revenue margins into the medium term.

GUD Holdings

We initiated a 1.0% position in GUD on 12 February, buying 580 shares at $12.19. GUD is Australia’s leading provider of automotive parts to the trade sector, with strong brand positions including Ryco. The business has also been able to successfully grow through acquisition of smaller suppliers, where GUD is often an uncontested purchaser. Historically, GUD owned a number of underperforming segments, but these have largely been divested, making this a cleaner and higher quality investment prospect. Today, 90% of earnings are derived from the automotive segment, with 10% coming from the Davey water pump business. In 1HFY2019, the business achieved a return on equity of 22% and earned an EBIT margin of 21%.

GUD’s share price has recently come under pressure as a result of weakness in vehicle related stocks, reflecting the fall in new car sales. The stock is down approximately 20% from August 2018 levels.

However, GUD is not servicing new vehicles but the total car market of Australia (18.6m cars vs ~1.2mpa of new car sales). Moreover, most of their business is for cars aged 5-10 years. Consequently, we consider that earnings are relatively defensive. In the recent half year result, the business achieved 5% organic sales growth, despite the soft consumer environment and in a period with very little new product sales. Management noted a stronger pipeline of new products being released in the current half, which should be supportive for the next result.

Management has also indicated that the pipeline for bolt-on acquisitions is strong. GUD’s scale, including national distribution, often makes them the natural owner for these businesses and provides scope for value-add post acquisition. The GUD balance sheet is in a relatively strong position, with net debt to EBITDA at 1.4x and $80m of unutilised bank facilities in place. Combined with ongoing free cash flow generation, the company is well placed to continue to make accretive acquisitions into the medium to long term.

GUD reported 1H19 NPAT and EPS from continuing operations up 14% on the pcp. Discontinued operations made a $2.5m NPAT contribution in the pcp. Management noted 5% organic sales growth in Automotive and a 13% contribution from acquisitions, with Disc Brakes Australia acquired at the start of the period and AA Gaskets at the end of the pcp. There was an initial negative reaction from the market, largely reflecting a higher expected contribution from acquisitions, leading analysts to question the organic growth. However, this largely reflected a transitional issue with AA Gaskets. This business was acquired from Bapcor, which had residual stock that was cleared in the half, reducing the contribution from this business. The stock price has subsequently recovered from the immediate reaction after the result.

Citadel Group

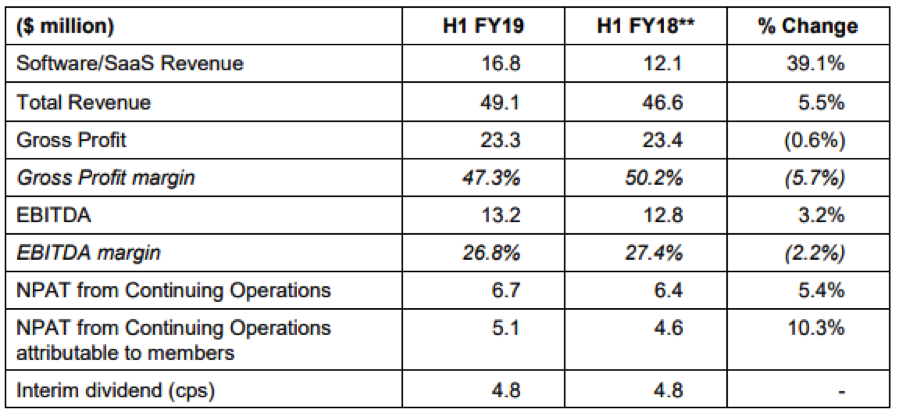

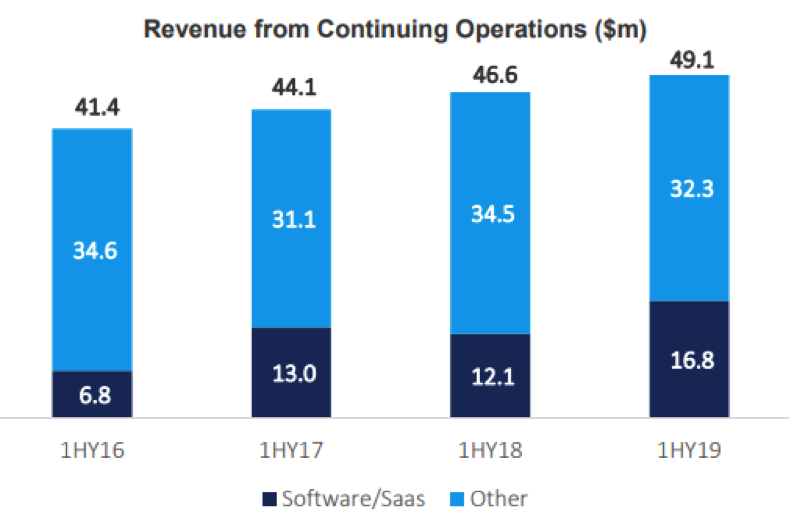

CGL delivered a weaker than expected 1H19 result, although the financial performance is obscured by a higher contribution from Software/SaaS revenues. SaaS contracts generate upfront fees at a fraction of software licenses but have higher customer lifetime value.

Operationally the business has momentum across its SaaS suite, particularly Citadel IX (SaaS), and the look remains upbeat. CGL has eight clients using Citadel IX covering 26,000 seats, including its first international government client in South East Asia. The company is targeting 200,000 seats by 2020, with 100,000 seats under negotiation.

The reporting of the opportunity pipeline changed from a Total Addressable Market (TAM) figure to a ‘Weighted Pipeline’, which represents the estimated aggregate Total Contract Value (TCV) of active sales opportunities, weighted by the probability of contract wins. Previously CGL pointed to a sales TAM of $800m with $480m of SaaS opportunities. In the 1H19 release, management estimated a Weighted Pipeline totalling $132m (at 31 Dec), up from $109m (at 30 June).

CGL’s SaaS strategy leverages its pedigree as a specialist advisory and enterprise software solution provider to complex and high-security environments into more scalable SaaS products. Although 1H19 headline figures were below expectations, operationally the strategy appears to be on track with several SaaS customer wins across government and public institutions, which will flow into future results.

Accompanying the 1H19 announcement, CGL announced the resignation of Founder and Director Miles Jakeman, following the Board’s decision to conduct an external process for Chair succession. The Board is seeking global tech experience. Jakeman holds 7.58 million shares (15.4%).

Clime Group owns shares in MFG, CGL and GUD.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

3 stocks mentioned

Clime Investment Management

Funds Management & Stock Research

Clime Investment Management

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

Expertise

Clime Investment Management

Funds Management & Stock Research

Clime Investment Management

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

Expertise

Comments

Comments

Sign In or Join Free to comment