Spice and excitement from monetary policy through 2019.

There’s not only a widening wedge between the US Federal Reserve (Fed) and all the other central banks, but between the Fed and Trump as well. We take a look at the policy rate differential between the US and just about everyone else, and why you could expect something to change in 2019. Get ready for some spice and excitement!

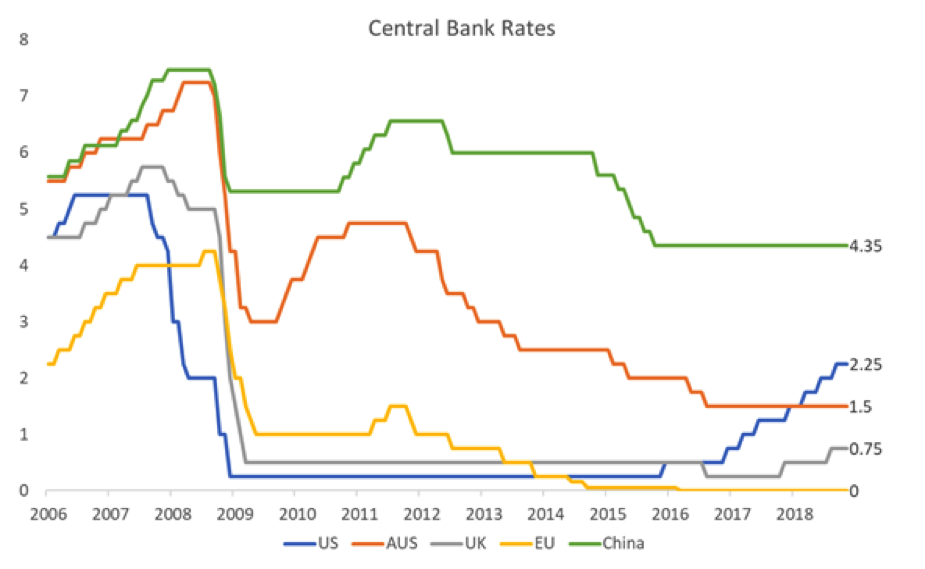

It’s extremely peculiar to see the Fed raising rates while no one else is doing anything, particularly in the modern day of connected economies. If it continues, the US dollar will only strengthen, making life tougher in emerging markets and potentially bringing Trump to blows with his central bank if growth is hit. However, the resulting international dislocation of capital will likely have to reverse at some point, causing more market volatility over the medium term.

The US made it clear early in the crisis that they didn’t think zero policy rates were sustainable and that they wanted to normalise rates as soon as possible. Bernanke cut his teeth as an expert on Japanese monetary policy and wanted to avoid the trap of low growth, high debt and low rates – hence stimulating growth with low rates and quantitative easing (QE), then bringing rates back above 2% as soon as possible. I would argue that they would have expected fiscal policy to become more conservative at the same time, which hasn’t happened yet under Trump.

Growth in the US has been healthy, unemployment is low, and price and wage inflation is high enough to justify normalisation, which started in late 2016. The Fed is likely to take rates up further from 2.25% to 3.0% in 2019 and has been the master of getting away with it over the last decade; they pulled off some smooth QE with little resistance and now they’ve finessed rates up without impacting the economy – but no one has followed suit.

Figure 1. Central bank rates in major economies. Source Bloomberg.

The Fed going it alone

Contrast the US with Europe, the UK or even Australia, where rates have gone nowhere over the last two years. You’ll see that the economic justification is the same as the US: unemployment is low and inflation is similar to pre-crisis, sitting at around 2% in all these regions.

Despite this, central banks have rates on hold at lower levels than the US. In Australia, the RBA only stopped lowering rates in late 2016 when the US was preparing to raise rates. Europe shows no signs of moving, and the UK has only dipped its toe in the water.

Despite all the economic indicators looking strong, central banks have been cautious of impacting growth, viewing growth and inflation as fragile. If they’re wrong and rates are held too low, I’d expect to see poor allocation of capital and higher inflation coming through in coming years. Even if they’re right about weak growth, they won’t have any monetary policy weapons to fight the next recession.

The pressure valve on policy mismatch is weaker currencies, and we’ve seen the Aussie dollar falling to the low seventies this year against the US dollar. Capital has flown towards higher yields in the US and will continue to do so. If the RBA stays put, the Aussie is likely to trade into the sixties in 2019 – but at what point does this become a problem? At 50c?

The situation is even worse in emerging markets, with Chinese bond yields at their lowest relative point to the US in eight years and the currency around its lowest point since prior to the peg in 2008. Central banks in India and Indonesia have given up resisting rate hikes, preferring to protect the currency rather than let growth run. The strong dollar isn’t ideal for the US either, undermining the country’s push for economic nationalism.

Expect some excitement ahead...

The current mismatch of monetary policy between the US and other countries like Australia is unsustainable – but who’s right? Will the RBA capitulate and raise rates when the dollar hits 50c?

Would blood be spilt on Martin Place if housing prices get hit by rate hikes? Or is the Fed being too aggressive, potentially resulting in growth collapse or Trump blowing up the Fed?

Either way, I’d expect some spice and excitement from monetary policy through 2019.

Find out more about Walsh and Company

High-quality investment opportunities are not always readily accessible to investors. We provide investors with access to market segments that are often beyond reach, helping them build better, high quality diversified portfolios. Find out more.

--

The above is general information only and does not consider any particular investor’s circumstances. It is based on the opinion of the author alone and is not intended to be a research report. The information should not be relied upon to make an investment decision without seeking further information and/or advice from a financial adviser and considering whether any investment is appropriate in the circumstances.

This article may contain statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. The author does not make any representation as to the accuracy or likelihood of fulfilment of the forward-looking statements or any of the assumptions upon which they are based. Actual results, performance or achievements may vary materially from any projections and forward-looking statements and the assumptions on which those statements are based. Readers are cautioned not to place undue reliance on forward looking statements and assume no obligation to update that information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

BML's Chief Investment Officer, Ted Alexander, has been managing investment portfolios since 2008 in London and Sydney. Ted has been the lead Portfolio Manager on multiple funds with a cumulative AUM of over $1.6bn, covering equities and bonds in US, Europe, and Asia, and has led sector research on healthcare, technology, and telecoms.

Ted was the Portfolio Manager on the Orca Global Fund from 2018 to 2022. The fund invested using the same process as the BML Global Fund, with 30-40 stocks, and targeting uncorrelated alpha. The BML Global Fund was launched in 2023.

Ted holds a Master of Philosophy in Economics from the University of Oxford as a Rhodes Scholar and First Class Honours in Economics from the University of Tasmania.

1 topic

BML's Chief Investment Officer, Ted Alexander, has been managing investment portfolios since 2008 in London and Sydney. Ted has been the lead Portfolio Manager on multiple funds with a cumulative AUM of over $1.6bn, covering equities and bonds in...

Expertise

BML's Chief Investment Officer, Ted Alexander, has been managing investment portfolios since 2008 in London and Sydney. Ted has been the lead Portfolio Manager on multiple funds with a cumulative AUM of over $1.6bn, covering equities and bonds in...

Expertise

Comments

Comments

Sign In or Join Free to comment