The best value stock to own is a growing value stock

In 2020 growth has been the only game in town. Zero interest rates and quantitative easing (QE) forever are sending value managers to the slaughterhouse. If you are feeling uneasy about paying high teen multiples of sales for cash-burning growth stories but are still looking for asymmetric risk/return opportunities. This Aussie small-cap company might just whet your appetite.

Shriro Holdings (ASX:SHM) is a leading Kitchen Appliances and Consumer Products marketing and distribution group operating in Australia and New Zealand. The Group markets and distributes an extensive range of products under company-owned brands (including Omega, Robinhood, Everdure and Omega Altise), and third-party brands (such as Casio, Blanco and Pioneer) in Australia and New Zealand.

I can hear you yawning now – where is the global TAM (total addressable market), where is the sizzle?

Hang on... they also do barbecues!

Shriro has an exclusive partnership with Heston Blumenthal selling BBQs in Australia and New Zealand, Europe and North America. After years of start-up losses (all expensed through the P&L) this business is turning the corner and is smack bang in the middle of the post-pandemic stay at home, play at home thematic.

Shriro debuted on the ASX in 2015 at $1.00 per share, giving it a market capitalization of $95m and an enterprise value of $121m.

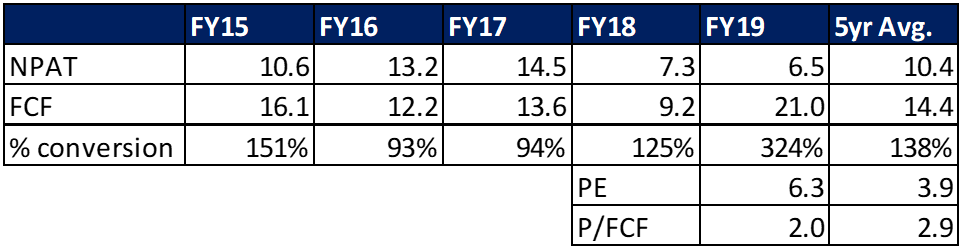

The company has had a few false starts since listing, with some restructuring needed following the east coast housing slowdown of 2018 and the imposition of US tariffs on Chinese made goods impacting the launch of their BBQ range in the USA. Net profit fell from $14.5m in 2017 to $6.5m in 2019. Despite these headwinds, Shriro has generated $90m of cumulative Free Cash Flow since its 2015 IPO – of which $42m has been paid to shareholders as fully franked dividends. An additional $48m has paid down debt, with the current balance sheet having $17m of net cash (post-payment of 1H20 dividend).

If you had invested in the IPO and held until now, you would have received 44% of your original investment in fully franked dividends but had a mark-to-market capital loss of 38.5%, resulting in a total shareholder return of 5.5% (pre franking). Whilst not an optimal investment outcome, at least your capital has been preserved.

Currently, SHM is trading at $0.61 per share equating to a market capitalization of $58m and an enterprise value of $41m.

SHM is trading on a historic FY19 PE (adjusted for cash) of 6.3x and a 5yr average PE (adjusted for cash) of 3.9x.

What’s changed? The business is now growing!

At the 1H20 result, SHM reported net income of $4.7m (growth of 74% year on year and 18.5% ex job keeper).

Even if SHM were breakeven in 2H20 (which seems a low probability given the seasonally stronger second half has started strongly with July and August sales up 20% YoY) SHM would be trading on 9x PE. That’s an 11% earnings yield. If SHM delivers a usual seasonal earnings mix, FY20 could produce net income of c. $10m. That’s a 24% earnings yield.

SHM has a lot of the characteristics we like in a company. It has a robust post-pandemic stay at home tailwind, conservative accounting (no intangibles on the balance sheet), it is capital-light and has high returns, it generates cash and funds its growth.

What’s not to like? The primary risk to the businesses is its relationship with Casio (which goes back to 1982), which may be terminated one day. But at current prices, the risk looks more than priced in.

Disclosure: Totus owns SHM in the Totus Alpha Fund (SHM is our only sub $100m market cap long position).

An ounce of performance is worth pounds of promises

Totus Capital is a Sydney based investment manager focused on Australian and developed market equities. Our long/short capabilities utilise fundamental bottom up research to identify mispriced securities. For further information, please visit our website.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim joined Totus Capital in 2019, having previously worked at Centennial Asset Management as an analyst, focusing on ASX small and micro-cap companies. Tim holds a Bachelor of Chemical Engineering (Honours Class I and the University Medal) degree from the University of Sydney.

1 stock mentioned

Tim joined Totus Capital in 2019, having previously worked at Centennial Asset Management as an analyst, focusing on ASX small and micro-cap companies. Tim holds a Bachelor of Chemical Engineering (Honours Class I and the University Medal) degree...

Expertise

Tim joined Totus Capital in 2019, having previously worked at Centennial Asset Management as an analyst, focusing on ASX small and micro-cap companies. Tim holds a Bachelor of Chemical Engineering (Honours Class I and the University Medal) degree...

Expertise

Comments

Comments

Sign In or Join Free to comment