The end February marks the start of a Seasonally positive period

Andrew McCauley

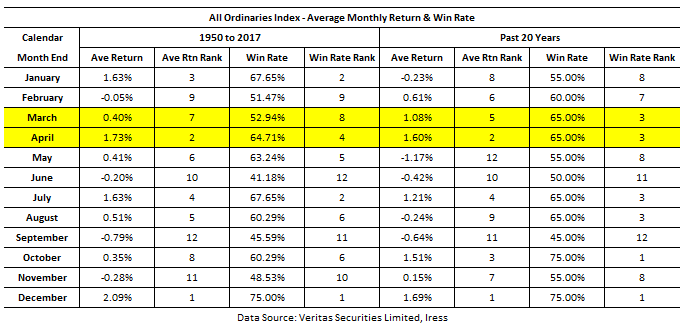

With regard to the All Ordinaries Index, I note that over the past 20-years, the only 2-month interval to provide consecutive average monthly gains of greater than 1% were March & April.

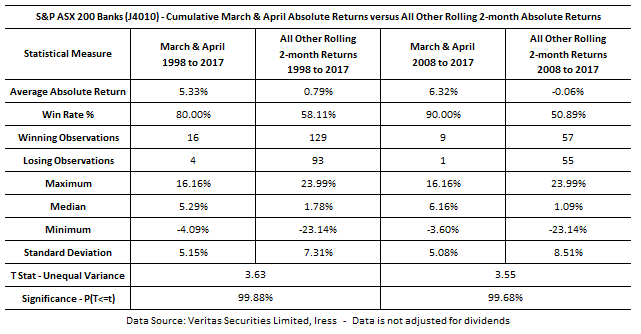

I would suggest that a fair share of this upward seasonal bias can be attributed to the consistently positive price performance of the Australian Banking Sector during the months of March & April. This positive Banking Sector tendency is largely related to a law introduced in 1997, that requires investors to continuously hold shares 'at risk' for at least 45 days to be eligible for the franking tax offset. The return data suggests that investors acquire bank shares at least 1 to 2 months earlier than the earnings release & ex-dividend day in order to maximise potential price appreciation combined with the 'at risk' value of the fully franked dividends.

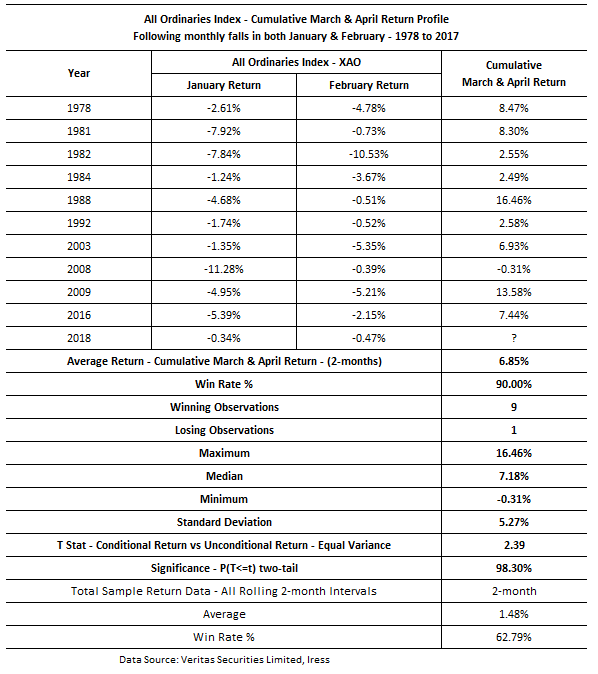

Interestingly, over the past 40-years, when the All Ordinaries Index experienced declines in January & February, the cumulative performance of March & April was significantly enhanced.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew has over 25 years’ experience in the Australian financial markets sector with extensive knowledge of both equity derivatives and statistical analysis (predictive techniques). Andrew is responsible for delivering evidence based market analysis to Institutional and High Net Worth clients. Andrew recently co-authored a paper on High Frequency Trading that was published in The Journal of Trading.

Andrew McCauley

Statistical Research & Data Analyst

Andrew has over 25 years’ experience in the Australian financial markets sector with extensive knowledge of both equity derivatives and statistical analysis (predictive techniques). Andrew is responsible for delivering evidence based market...

Expertise

Andrew McCauley

Statistical Research & Data Analyst

Andrew has over 25 years’ experience in the Australian financial markets sector with extensive knowledge of both equity derivatives and statistical analysis (predictive techniques). Andrew is responsible for delivering evidence based market...

Expertise

Comments

Comments

Sign In or Join Free to comment