The facts and fluff of thematic investing

Bill Gates once said, “We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten”. We all love a story, but how do we separate a good story from a genuinely good investment idea. In a recent webinar, Steve Johnson, Gareth Brown and Kevin Rose discussed why people are so attracted to thematic investing, some of the trends set to change the world and how we can separate the facts from the fluff.

You can listen to the full webinar at the bottom of this article or fast forward to the relevant area using the time stamps provided.

Why are we so attracted to themes? (1:38)

Steve – Our brains are wired to look for a story. In Daniel Kahneman’s book, he discusses this idea that to stop and think about things takes time and effort, and if we are presented with a good story up front then we don’t need to worry about the stopping part.

Gareth – Evolution is the main explanation. Throughout our lives important lessons have been passed on through story-telling, which is a powerful way to share insights, but it makes us suckers for a narrative

Kevin – The appeal of thematic investing lies in the fact that they take something that is complicated, investing, and turn it into something that sounds incredibly simple. The overwhelming aspect of numbers and ratios is broken down into something much more manageable.

Trends changing the world (3:37)

Gareth – Renewable energy has become a very important part of the energy mix in the last few years, and it’s starting to benefit from a growing tailwind as prices become more competitive

Kevin – An industry that we are quite confident will grow, is digital advertising. It’s not a new thing but online growth and access to definable metrics are providing companies with more transparency in growing their sales.

Steve – The Chinese middle class. It has been a theme that a lot of Australian investors have been focussed on and its real. Areas of the country that are rising out of poverty and into the middle class will have a big impact on Australian products sold into China.

Successful investments thanks to tailwinds (6:59)

Steve – a2 milk has seen some sensational results for investors as they capitalise on demand from the growing Chinese market

Kevin – Alphabet. They are the 800lb gorilla in the digital advertising space. Combined with Facebook they own 50% of advertising dollars going into the market so there is huge growth there.

Gareth – ARB Corporation had huge growth over a 16-year period, fuelled by the demand for 4WD bull bars and accessories

Problem(s) with thematic investing (10.40)

Steve – A good story trends to come with a high share price. Value often doesn’t come with a theme behind it

Gareth – Moats absolutely matter. You need a competitive advantage. Good stories attract a lot of competition and if a company doesn’t have a lock on its customers, that competition will revert those returns to average at best, and in some cases, a blow up

Steve – We are always thinking, is the trend real? Does the business have the ability to capture a good chunk of that growth? And what does the current valuation imply about that future growth?

Hyped sectors that probably won’t deliver (14.18)

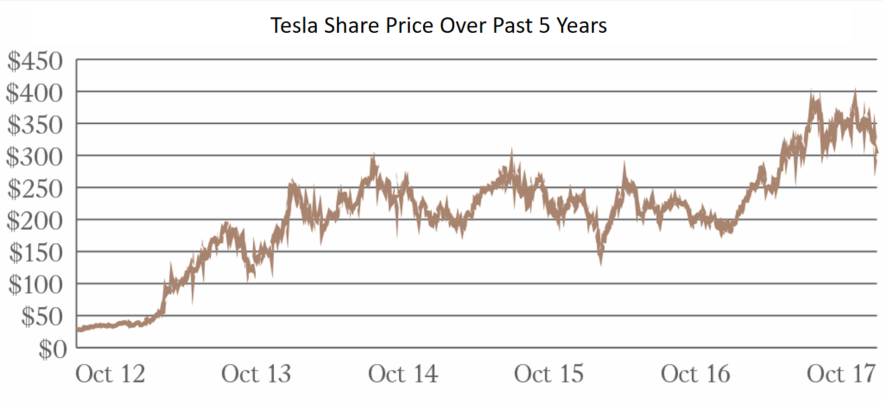

Gareth – We recently travelled around Europe to see the impact of electric vehicles (EV’s), including going to Norway which is the Tesla capital of the world, as well as a conference in Munich. There were plenty of slides around the threats and opportunities for each of the car manufacturers. I’m very confident of more EV’s in 10 year’s time but I’m not confident that Tesla will be the dominant player.

Kevin – Their stock price has continued to rise in what appears to be “best case scenario momentum”, with future success being priced in today. They have ½ the implied enterprise value of GM, but produce 100th the number of cars. That’s a hefty price to pay for a story.

So how do you spot a good anti-narrative (19.05)

Steve – Buying a business in decline is psychologically difficult. We find our best opportunities are in the areas where the story is not great. Mining services in Australia has been a great example of this

Gareth – Italian small cap El.En was another example of a narrative that we thought offered promising growth. Where the market was focussed on the fact that it was small cap, it was Italian, it was slow growth and there are lots of risks, we benefitted from the strong potential tailwinds

Steve – It’s about trying to find opportunities where the stock price has been caught up in a negative thematic, but we think it’s as important as the market makes us believe

Kevin – Cable One illustrates that point well, where the idea of customers cutting their ties in favour of alternatives like Netflix stagnated the share price. However, the underappreciation of their internet business provided enormous future opportunity

Value traps and sectors in decline (24.49)

Steve – We think long and hard about whether the trend is real and the impact that it is going to have. Charlie Munger once said, “It’s hard to pay a low enough price for a business in decline”, and I think its applicable to quite a few industries and businesses at the moment

Gareth – Look at Fairfax. On the face it looked cheap, but over the last decade there has never been a good time to invest

Kevin – Another company, Sears, is a great example of a value trap. It had a good brand, a great portfolio, but when the retail sectors started to demise, it had nothing to fall back on

Valuing any business (29.11)

Steve – You need to be able to answer 3 questions

1. How much cash are you going to get?

2. When are you going to get it?

3. How sure are you?

Rules of thumb when investing (30.57)

Steve – There are two ends to the spectrum.

Gareth – Investing in stocks with growth potential

Kevin – Making money from the anti-narrative

If you are interested in receiving the Forager monthly and quarterly reports, please register here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

With approximately $445 million in funds under management (as at July 2025) and a focus on long-term investing, Forager Funds is a unique Australian asset management company. Forager runs an Australian Shares Fund and International Shares Fund - both of these are unlisted products.

Now with a 15-year track record, Forager is a sustainable business but remains nimble enough to invest in smaller listed companies not accessible to many investment managers.

1 topic

With approximately $445 million in funds under management (as at July 2025) and a focus on long-term investing, Forager Funds is a unique Australian asset management company. Forager runs an Australian Shares Fund and International Shares Fund -...

Expertise

With approximately $445 million in funds under management (as at July 2025) and a focus on long-term investing, Forager Funds is a unique Australian asset management company. Forager runs an Australian Shares Fund and International Shares Fund -...

Expertise

Comments

Comments

Sign In or Join Free to comment