TOL - 15th Aug, 2025

"The highest quality company on the ASX" - Jun Bei Liu remains bullish on Pro Medicus

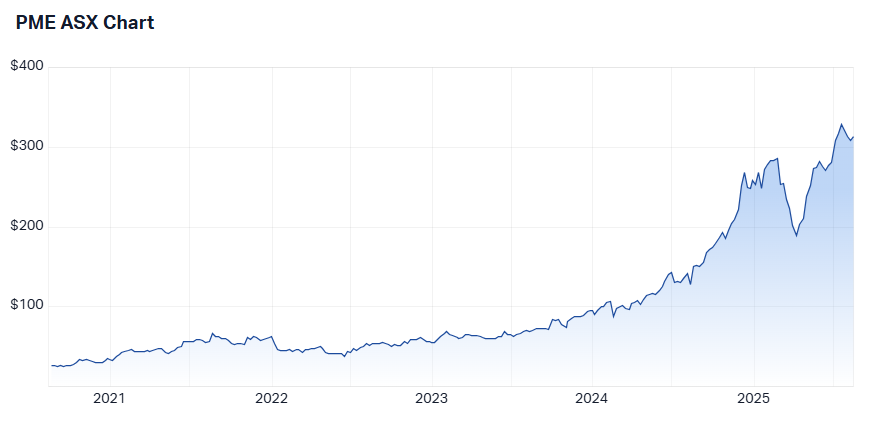

She was bullish on PME at $25 and is still adding, confident there’s plenty of upside left in the trade.

Pro Medicus’s (ASX: PME) FY25 results prove the company is cementing its position as a dominant player in its total addressable market, now holding the psychologically important 10% share of North America.

Beyond the stellar numbers, CEO Dr Sam Hupert used the results to highlight PME’s unique edge: competitors simply can’t match its technology.

“We continue to see Cloud as a strategic advantage for us, as our competition has not been able to re-engineer their systems to fully take advantage of cloud and have had to resort to hybrid options, which we feel is a backward step.”

It’s one of the key reasons why investor enthusiasm for PME keeps building. This healthtech growth stock is carving out a moat that rivals are struggling to breach.

For Jun Bei Liu, who first bought PME at $25 during COVID and has been right to stay bullish ever since, the thesis remains as strong as ever.

"This is probably the highest-quality company listed on the ASX. It has very predictable earnings and continues to grow massively, with a huge addressable market."

We spoke with her about PME’s latest results, how the company is outmaneuvering competitors, and the incremental developments CEO Dr. Hupert just announced that investors should watch closely.

Pro Medicus' FY25 Results

- Revenue up 31.9% to $213m vs. $212.5m ests (0.2% beat)

- Net profit after tax up 39.2% to $115.2m vs. $113.7m ests (1.3% beat)

- Final dividend of 30 cps, full-year dividend of 55 cps

- Cash up 35.5% to $210.7m

- Record year for new contract wins, contract renewals and sale of additional modules to existing clients

What was the key takeaway from PME's result in one sentence?

In one sentence: solid, strong, and quality.

We thought the result was really solid - in line with expectations, but so it should be, because that’s what a quality company does: it delivers. There was a slight outperformance on expectations, without too many surprises for investors.

Were there any surprises in this result that you think investors need to be aware of?

Yes, there were positive surprises. The result itself was very strong, but the key incremental news is the release of their digital pathology platform. It will be native within their key product, Visage 7, and is expected to launch in late 2025, in the fourth quarter.

This is important because more hospitals are pivoting to broader enterprise imaging contracts, which will help them expand both reach and market share. It’s a really positive development, and I think over the long term we’ll start to see bigger and bigger contract wins from Pro Medicus.

Would you buy, hold or sell PME off the back of this result?

Rating: BUY

This is probably the highest-quality company listed on the ASX. It has very predictable earnings and continues to grow massively, with a huge addressable market. They’ve now captured 10% of the US market and still have a long growth trajectory ahead, with more verticals coming through.

For example, over the next 12 months they can pretty much see what their revenue will look like — and that level of predictability is rare for most businesses, which are still dependent on the economic cycle or other variables.

How much upside do you see in the share price, currently above $300, from here?

Based on what we know today, our target price is about 30% higher than the current share price.

However, every time they move into a new area and demonstrate success - for example, with this new platform - and start winning larger contracts, that target price should expand. So while it’s 30% higher for now, over time, as more verticals come online, the upside could be many times the current share price.

So, close to $400 based on what we know right now?

That’s right.

In the CEO interview, Dr. Hupert talked about PME’s competitive advantage as a 100% cloud-based solution. What does this tell you about PME’s edge?

I think it’s huge. Pro Medicus is cloud-native - everything is hosted in the cloud. Their product is already being used by many AI companies in the imaging space, which makes it easy for those businesses to adopt and integrate.

That creates the potential for it to become the standard of practice. We know in technology that first-mover advantage is huge, and PME is native to that movement. I think it will continue to be adopted by more hospitals and businesses over time.

Are there any risks investors need to be aware of?

The risk is that this is a growth company, and it’s expensive. For a growth company, you need to continue hitting growth targets.

Our valuation is based on expected growth and addressable market. If they start losing contracts - which we don’t expect - or miss growth targets, that’s a risk. And because the stock is expensive, it can be more volatile, making it a higher beta stock.

This is the nature of investing in growth, you hold it alongside other types of investments, like value stocks, gold, and so on.

From 1 to 5, where 1 is cheap and 5 is expensive, how much value are you seeing on the ASX today?

Rating: 4

I don’t think the ASX overall is expensive. Some stocks, like Pro Medicus, are expensive - but they should be, given their growth.

The rest of the market has a lot of sectors that don’t look expensive. I think that’s where the opportunity is. I expect the market will take another leg up with rate cuts and the resilience we’ve seen in corporate earnings. Investors should stay invested.

Which sectors look attractive?

Companies involved in housing: builders, apartment developers, and related businesses. Valuations there require a longer-term view because earnings are at trough levels due to patchy consumer demand.

But when fundamentals turn, analysts tend to underestimate the operating leverage on the upside.

There’s also value in smaller companies as large caps have outperformed significantly, but we’re seeing rotation from expensive large names into cheaper alternatives. That’s where I think we’ll see strong outperformance over the next 12 months.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

3 topics

1 stock mentioned

1 contributor mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management