The investment clock has turned to credit

COVID-19 has hit most investors’ portfolios hard and fast. With the initial impacts behind us, investors are turning their attention to the investment landscape looking forward. A lot has changed, and the investments which suited your portfolio pre-COVID-19 may not be the ones that are useful now.

For investors focused on income, the world has changed dramatically:

- Term Deposit rates / Government Bond yields have fallen to record lows;

- Equity dividends are at risk; and

- Listed Property Trusts (and other sectors) may be in for a round of capital raisings… but

- Credit yields, the yield on corporate bonds and loans, have increased, with falls in prices providing more attractive source of income.

The challenges for term deposits / government bonds

We entered 2020 with unusually low interest rates globally, which were then slashed further in March as central banks rushed through emergency cuts to official cash rates.

With falling rates, the income available from term deposits and government bonds has now reached historical lows, which will make it difficult to support a comfortable retirement lifestyle. Major bank term deposit rates, for example, currently offer around 1% (or less) interest rate.

And while true cash retains its role as the defensive asset in troubled times, the traditionally "defensive" role of government bonds is now questionable, with very limited room for capital appreciation (from further rate falls), but risks of capital losses if rates begin to normalise.

The risks for equity income

Investors need to prepare for dividends to be cut.

COVID-19 has caused a sharp "earnings gap" for corporates, as companies suffer from reduced revenue (or in some cases a total loss of revenue due to temporary shut down) until economic activity can resume. This "earnings gap" is hard to bridge. There are numerous levers a company can try to pull in order to survive through to a post-COVID-19 world, but many of these hurt the equity investor:

- reduce the cost structure: renegotiate with suppliers and distributors

- cut capex

- cut dividends (a very real risk for those relying on equity income)

- raise fresh capital through (dilutive) rights issues (loss of value for existing investors)

Cutting dividends is one of the first and easiest ways for companies to preserve cash, as dividend payments are entirely at the discretion of the corporate. These changes are already underway (take the recent ANZ and Westpac results as an example).

While companies can choose to cut dividends, companies cannot choose to skip their legal interest payments to lenders, such as bondholders. The legal entitlement of loan and bondholders to their coupons is valuable for investors who rely on income. Moreover, it cannot be diluted in the event the Company issues additional shares.

The opportunities in corporate credit

The shakeup in markets in the past two months has seen bond and loan prices fall (i.e. yields have increased), and as a result, the sector offers more attractive forward-looking returns than have been available for many years.

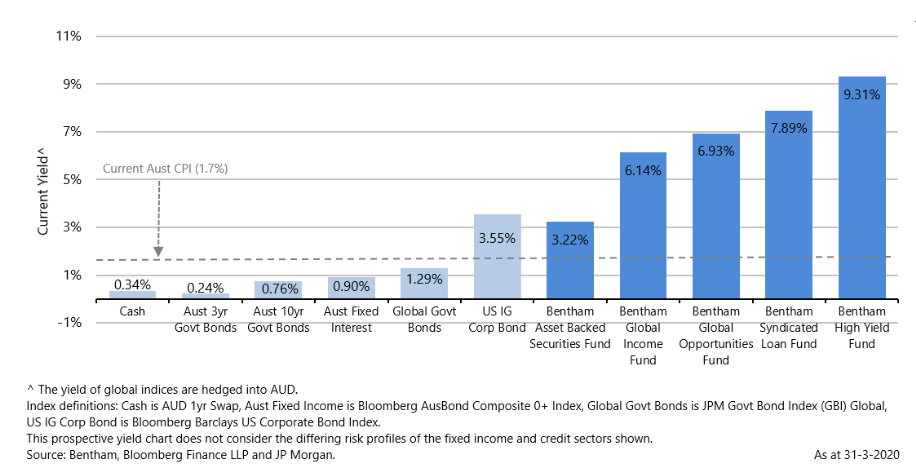

See the chart below for the yields available from various types of corporate credit (investment-grade bonds, high yield bonds, loans) and also cash and government bonds as at the end of March 2020.

Corporate credit has become a more attractive source of income - the investment clock has turned to credit

The resilience of credit

In our view, the risks of investing in corporate bonds/loans have indeed risen, but not as markedly as is currently priced in. Credit markets are pricing in a deep recession. Defaults will no doubt tick up in the months ahead, and this is already antecipated in credit pricing

In 2020 the banks and Governments have - so far - shown remarkable support for corporates looking to bridge that earnings gap. We've seen corporates globally drawing down on their revolving credit facilities to shore up their cash positions, and we've seen banks underwriting new liquidity lines to support their clients through to the other side of the COVID-19 chasm. If banks and governments continue to extend this support, it could limit the degree of defaults in credit markets.

Credit investments don't require a return of the global growth story in order to perform. The hurdle is much lower for credit than for equity markets. A successful credit investment just needs the borrower to keep paying its coupon and return the principal at the end of the bond's maturity. Regardless of the discount at which you buy a bond or loan (US senior loans are trading on average at 85c in the dollar right now), the borrower is obliged to repay the full-face value (or 100c in the dollar) at maturity. This creates what is know as "pull to par" - a corporate bond or loan typically reprices back towards par as its maturity gets closer.

This feature, combined with the senior position of credit in the capital structure, makes credit a very 'resilient' asset class. It tends to fall less than equities in a downturn and can recover faster.

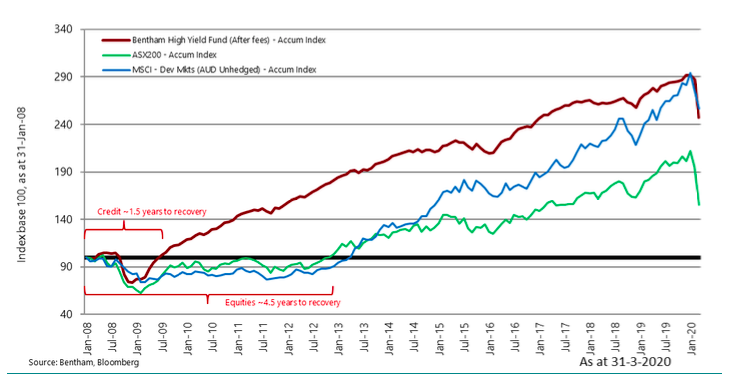

The resilience of credit demonstrated following the GFC

2008 was an excellent example of the resilience of credit coming out of a downturn - credit markets took roughly 1.5 years to recover, while equity markets took roughly over 4.5 years.

The hands of the investment clock have turned

As earnings have become less certain, growth is under question and dividends are suppressed, it is not that surprising that the certainty of coupon payment from bonds and loans (credit) may provide a more resilient investment.

Look beyond for new sources of income

Bentham invests in institutional quality asset classes that diversify risk while generating regular monthly or quarterly income for investors. Click 'follow' below to hear more of our insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Richard Quin is the CEO, founding Partner, and Lead Portfolio Manager of Bentham Asset Management, a specialist global fixed interest, and credit investment manager based in Sydney.

Featuring

Richard Quin,

Bentham

Richard Quin is the CEO, founding Partner, and Lead Portfolio Manager of Bentham Asset Management, a specialist global fixed interest, and credit investment manager based in Sydney.