TOL - 12th Aug, 2025

The lithium bear market is finally over (or is it?) Latest demand, supply, and price drivers, plus ASX lithium stocks to watch

Lithium has spiked in the last few weeks, leading many to speculate the low is in. We investigate the latest price drivers to see if it is.

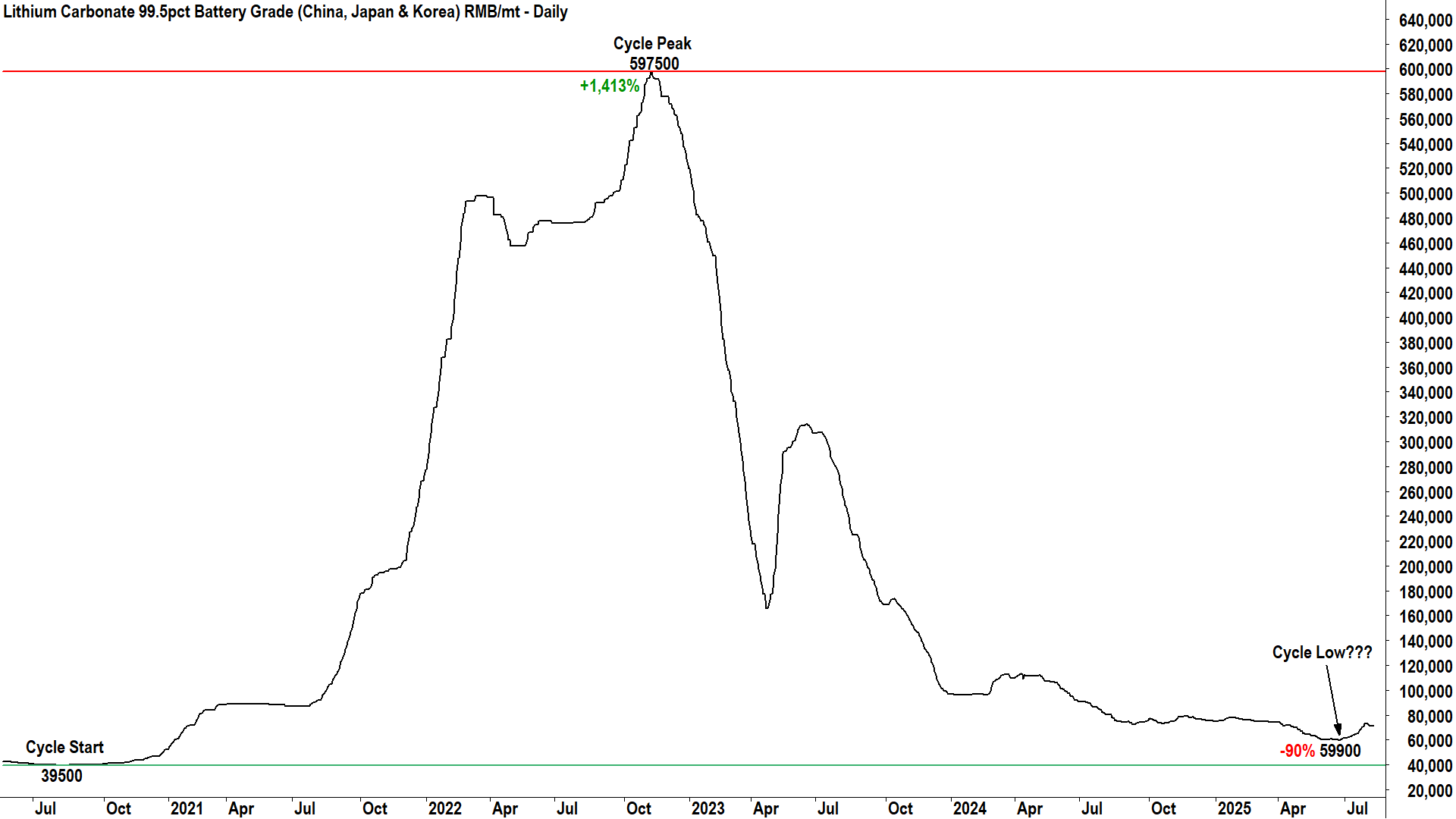

After a near-3-year bear market that saw lithium contracts fall as much as 90% from their 2022 highs, a sharp six-week rally from late June has caught many investors off guard. Key lithium price contracts surged between 35-45%, only to fall 10-15% into early August. The violent price swings have raised a pressing question: Is this the start of a structural recovery in lithium markets, or is it merely another false dawn driven by a quirky speculative bubble?

For context, lithium prices had collapsed over the better part of the last three years as a wave of supply from new hard rock mines in Australia, brine fields in South America, and lepidolite in China, overwhelmed even the impressive growth in electric vehicle (EV) and battery storage demand. But the fundamentals are potentially beginning to shift, at least marginally – yet there’s been nothing “marginal” about the rising hopes among lithium’s faithful – judging by social media, those are definitely soaring again! 🚀

%20RMB-mt.png)

%20RMB-mt.png){kind=link}

This article draws on the latest research on lithium from the likes of UBS, Barrenjoey, Canaccord Genuity, Macquarie, Morgan Stanley, and others to assess if there has been a fundamental change in lithium's supply-demand balance or if this was just another sentiment-fueled spike, amplified by futures trading and policy noise within China. We explore the latest demand and supply side factors, as well as the latest price expectations, and of course, what it all means for ASX lithium stocks.

Latest lithium demand-side factors

On the demand front, the latest data is strong – well outside the US, that is. EV sales in China and Europe posted solid year-on-year gains in June, with Chinese sales growing 30% year-on-year to 1.1 million units and European registrations rising 21% to 358,000 units. In the US, at 113,000 units, sales contracted 13%. Battery production in China – which accounts for over 80% of global volume – jumped 53% year-on-year to June, with energy storage also seeing meaningful growth.

These end-use indicators have caused some brokers to revise up their expectations. Canaccord Genuity, in its 25 July note titled “Lithium | Demand’s in Charge Now”, conceded that its earlier pessimism was misplaced. It now sees global EV sales growing at 30% year-on-year, with China up 32%, the EU up 26%, and the rest of the world up 41%. Even after accounting for a decline in US tax incentives due in September (The One Big Beautiful Bill will end US$7,500 tax credits for new EV purchases), the firm expects robust structural demand to continue driving lithium consumption. Canaccord has revised up its demand growth by 200kt lithium carbonate equivalent (LCE) per annum through 2030.

Midstream activity, however, has not caught up. In its new monthly lithium report, “Joey’s Lithium Monthly”, Barrenjoey observed that while cathode production rose 51% year-on-year in June, Chinese raw materials buyers remained cautious in the face of growing inventories – which have hit a record 130kt LCE, or about 31 days of consumption. This mismatch suggests that although end-user demand is healthy, the rest of the value chain is still dealing with a hangover from the previous cycle.

Barrenjoey did however also note “continued strength in end-use demand for lithium”, citing strong EV sales, but also those robust Chinese battery production numbers. It also pointed to very strong battery cathode production, which covers the vast majority of battery usage cases, 51% higher year-on-year to June.

Latest lithium supply-side factors

The story of lithium’s rally in June and July cannot be told without reference to China’s so-called “anti-involution” campaign – a policy slogan adopted by the Chinese leadership to address overcapacity and “disorderly competition”, particularly in sectors like steel production, batteries, and electric vehicles (it’s also arguably to blame for the recent spike in metallurgical coal prices – but that’s an article for another day!).

As noted by Barrenjoey, the anti-involution theme was launched by President Xi Jinping at a high-level meeting in early July, and was followed by coverage in China’s top policy journal Qiushi, as well as repeated mentions in subsequent Politburo meetings. While no formal production cuts were or have been announced, the market interpreted the rhetoric as a signal that supply-side reform in lithium is now on the agenda – potentially akin to what occurred in the steel sector in 2015-16.

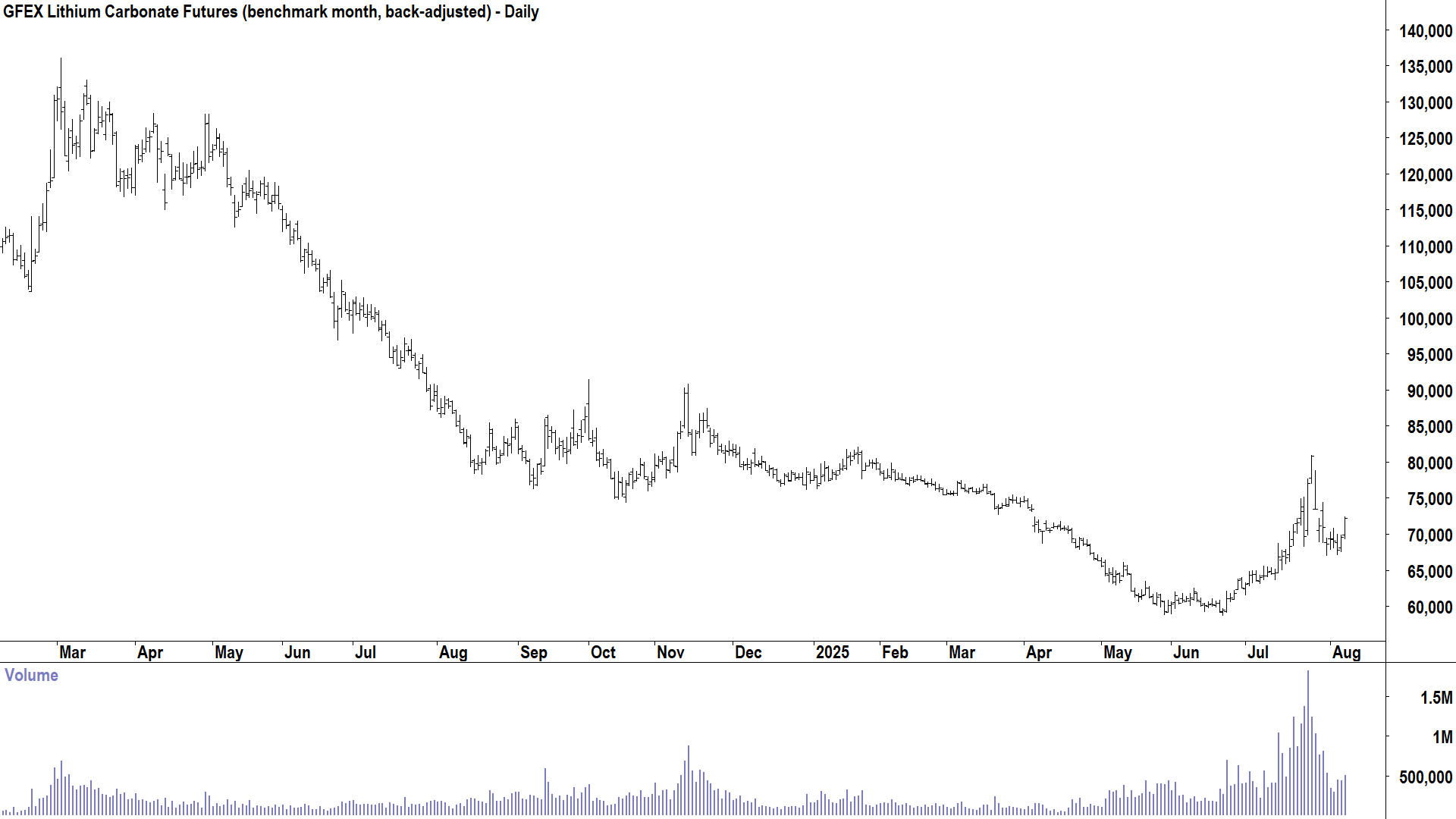

The reaction was immediate. Lithium carbonate futures on the Guangzhou Futures Exchange (GFEX) surged above 80,840 RMB/t by 25 July, more than 37% higher than the June all-time low of 58,720 RMB/t set on 23 June. Speculation intensified on the back of permitting issues at eight lepidolite mines in Jiangxi province, including CATL’s large-scale Jianxiawo operation, and the shutdown of Zangge Mining’s brine operations in Qinghai Province due to licensing breaches.

But as Macquarie and Morgan Stanley have each pointed out in recent respective research reports, these disruptions were mostly procedural and unlikely to result in major long-term production losses. The Jiangxi mines were allowed to continue operating while resubmitting reserve assessments, and Zangge’s capacity was small relative to the 1.5-1.6 million tonne per annum global market (~11kt LCE target for CY25 according to Morgan Stanley, “DataDig: Lithium supply response with strong demand”, 21 July 2025; “less than 2% of China's LCE annual output” according to Macquarie, “Critical Minerals Chronicle”, 29 July 2025).

The consensus among the brokers is what mattered more was sentiment. Macquarie, in its “Critical Minerals Chronicle” published 29 July, called it a case of “Tail wagging the dog”. This implies the run-up in lithium prices as a classic unwind of overly bearish positioning, driven by news of mine reviews and the anti-involution policy rhetoric. But it warned the rally had become “overextended,” and pointed to the sharp correction on 28 July during which lithium futures on GFEX hit “limit-down” across several contracts (most exchanges have maximum move circuit breakers that halt trading when a particular contract has moved up or down by that amount).

This was the turning point. GFEX immediately imposed strict daily trading limits, capping speculative participation (causing prices to continue to correct, falling as much as 17% before steadying in recent sessions). Shortly after, CATL stated it was optimistic about receiving renewed permits for its Jianxiawo mine, further dousing hopes of material supply disruption. The benchmark November 2025 lithium carbonate contract on GFEX is now trading at 69,900 RMB/t at the time of writing.

{kind=link}

Back to the “real” supply-side picture (note my own scepticism that anti-involution is going to have any lasting impacts on the lithium market!). On potential supply disruptions from marginal producers – arguably the critical swing factor in lithium pricing – Barrenjoey had this to say, “We see mine shuts as a relatively low probability event, given the significance of these mines to local employment and tax revenue.” The broker did point out two critical dates for investors to watch, though: the 9 August expiry of mining permits at Jianxiawo and the 30 September deadline for the resubmission of resource assessment reports by those 8 Yichun lepidolite mines.

Putting aside the issue of potential near-term supply disruptions, most brokers concluded that oversupply remains the dominant force in lithium pricing. Statistics for June showed that Chinese lithium chemical production – which accounts for over 60% of global production – rose 19% year-on-year to June. According to Barrenjoey, Jiangxi, Sichuan and Qinghai accounted for over 85% of China’s lithium chemical supply.

China’s spodumene imports from external sources are also ramping up, with imports from Zimbabwe up 94% and from Nigeria up 126% year-on-year to June – and are rising fast. As a result of the seemingly continued wall of lithium minerals supply, Macquarie had this to say, “In spite of this short-term blip, we believe the lithium market fundamentals remain largely unchanged and will remain over-supplied in the very near term.” Barrenjoey offered this: “In our view, fundamentals have hardly changed, with both China and ex-China supply still ramping up.”

Latest lithium price forecasts

Demand + Supply = Price

Right? So, putting all of the abovementioned factors together, what have the big brokers concluded about lithium prices? Is the “big low” finally in?

Good news, lithium bulls! Across the brokers, there is broad consensus that lithium prices likely bottomed in June. But bad news, lithium bulls! There remain diverging views on how sustainable the rebound will be.

Canaccord, which revised its 2026 and 2027 forecasts up by 5% and 20% respectively, is now constructive. It sees demand gradually outpacing supply and believes that pricing has room to continue climbing as inventory is worked through. That said, it acknowledged that latent capacity – including high-cost, temporarily shuttered operations – could keep a lid on more dramatic upward price gains.

Barrenjoey took a more cautious stance, noting that production remains elevated in both China and ex-China regions, and inventories are still building. It believes the rally was sentiment-led, not structural. The prices of ASX lithium stocks, it warned, now reflect spodumene pricing between US$1,090-1,280/t – a substantial premium to the current spot price of US$750/t.

Morgan Stanley, meanwhile, highlighted that based on its latest demand and supply assessments, the market surplus in 2025 has narrowed from 106kt in December to 63kt today. But this is still a surplus, and it too flagged sentiment as the main driver of recent bullish price action in both lithium minerals prices and ASX lithium stocks.

Macquarie believes the market could be disappointed by the magnitude of supply disruptions out of China, and that “A rangebound lithium market could emerge to support margin accrual along the value chain without lithium prices over- or undershooting for an extended period of time.“

Ultimately, the picture that emerges is one of cautious optimism. Most brokers believe the worst is over, but that a durable price recovery will require either further supply cuts, sustained demand growth, or both.

ASX lithium stocks – latest views

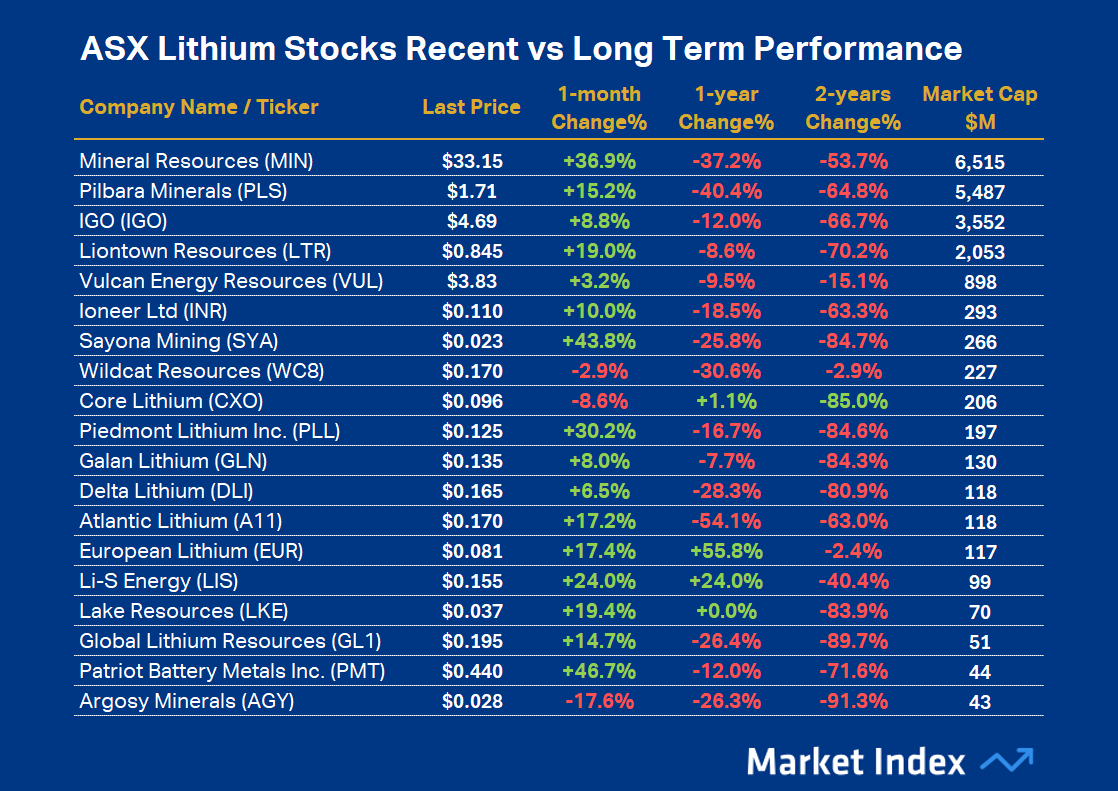

ASX-listed lithium producers enjoyed a strong bounce in tandem with the broader commodity rally. Pilbara Minerals (ASX: PLS), Liontown Resources (ASX: LTR), and IGO (ASX: IGO) all surged (see table below), but have since settled back to trade modestly below recent highs. Still, they are generally well above their cycle lows.

{kind=link}

Canaccord saw fit to raise its target prices for the trio by 17% to $2.70, 36% to $0.95, and 20% to $4.80, respectively. The broker is buy rated on PLS, but is only hold rated on LTR and IGO. It also upgraded Core Lithium (ASX: CXO) from hold to speculative buy and raised its price target on the stock from $0.10 to $0.15.

Morgan Stanley noted its preference in the sector remained Mineral Resources (ASX: MIN), which it rates as overweight. It also likes PLS as overweight on “improved production/costs with P1000 ramp complete”. The broker’s MIN price target is $35, and its PLS price target is $1.85.

Yet, other analysts are warning that share prices may be running ahead of reality. UBS also noted that the valuations of PLS, LTR and IGO imply spodumene prices well above spot – despite no major change in market-wide supply conditions. UBS is presently sell rated on all three lithium producers.

Macquarie added that rising short interest in both PLS and LTR suggests institutional investors may be betting on a pullback – potentially in anticipation of another bout of speculative cooling or an underwhelming earnings season. Still, it has an outperform rating on PLS and IGO, with price targets of $1.50 and $4.50, respectively. It is underperform rated on LTR, though, with a price target of $0.55.

(We’ll crunch the numbers on various lithium stocks broker ratings and price targets and bring you a dedicated article on the latest broker consensus soon!).

Conclusion: Lithium low - sentiment or reality?

The evidence suggests lithium's recent rally was driven less by shifts in underlying supply or demand, and more by sentiment – sentiment triggered by China’s ambiguous anti-involution campaign plus fears over local mine disruptions. These narratives, though powerful, are yet to be backed by enforceable policy / actual supply impacts.

The speculative surge has faded, halted just as fast as it began by tighter trading controls and the pragmatic assessments from key players like CATL. For now, the fundamentals remain stretched: inventories are high, supply continues to grow, and latent capacity could return with minimal notice if prices climb too far, too fast.

Still, there are genuine bright spots. EV and battery storage demand is proving resilient – and no one has had any reason to doubt lithium’s incredibly bullish demand-side narrative. Some higher-cost supply has been pared back, which is a positive, and project delays and or those Chinese production disruptions could mean the medium-term market balance tightens more than previously forecast.

The question now is whether lithium’s June bounce was the start of a new uptrend or just another echo in a market still finding its floor. Either way, prices are no longer in freefall – even sideways is a major improvement here – but without clearer supply discipline or a sharper inflection in demand, lithium may be plodding along the bottom for some time to come.

This article first appeared on Market Index on Thursday, 7 August 2025.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

5 topics

19 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment