The Long View: Investing through adversity

My colleague Tim Armour has shown how markets periodically experience corrections that are part of the investment environment. Recent volatility has been jarring but the global economy is largely supportive of corporate earnings and markets. History highlights the paramount importance of staying invested through volatile economic periods to provide long-term rewards.

Overdue and not entirely unwelcome: That’s one way to look at the correction in the S&P 500 earlier this year. Although swift declines can be unsettling, they have long been part of the investment environment.

“We were overdue for some kind of correction,” portfolio manager Tim Armour says. “I am not overly concerned about this pullback. Markets do better over the long term when they experience corrections periodically; they can’t go up all the time.”

Tim says that generally solid economic data continues to provide a healthy backdrop for markets in much of the world. In the United States, corporate profit growth remains healthy, tax reform could boost gross domestic product (GDP) and consumer spending is relatively strong.

Abroad, China’s GDP accelerated for the first time in seven years in 2017, and the economies of other emerging markets continue to show strength. Japan’s economy is in its best shape in years, and Europe is on the rebound. Overall, the International Monetary Fund expects global GDP to hit 3.9% in 2018.

“We still feel good about the economic backdrop for corporate earnings, and we think there are plenty of opportunities to invest in companies that have the potential to reward investors,” Tim says.

Volatility also reinforces the value of diversification, and the role of bonds, Mike Gitlin, head of fixed income, says. “Investors need to stay balanced in their equity and fixed income weightings in their portfolios, especially during times like this. It’s important that investors focus on the four primary roles of fixed income in a balanced portfolio: diversification from equities, income, inflation protection and capital preservation.”

Some core bond strategies may not provide the diversification from equities that investors expect, and that could be a problem. “That said, the current pullback may present a great opportunity for investors to upgrade their bond portfolios to what we refer to as true core: that means reallocating to bond funds that offer the potential for both solid income and diversification from equities,” Mike says.

Tim says the most important thing to do during periods of volatility may be one of the hardest. “You have to contain your emotions. It’s not easy to do on the way up, and it’s not easy to do on the way down, but it is the key to creating wealth over time. Sticking with the fundamentals, employing good asset allocation and maintaining a balanced portfolio with a long-term horizon is the best approach.”

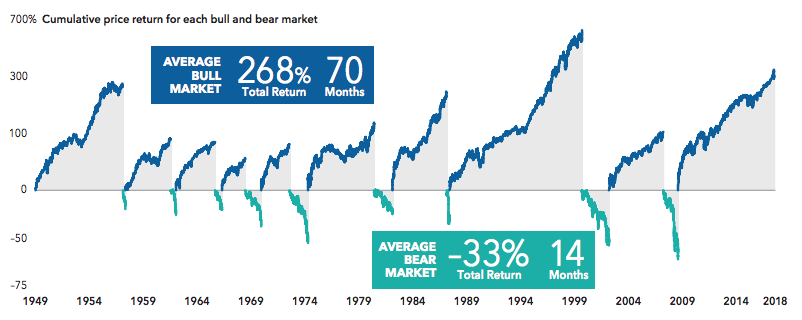

Bull vs Bear: Long-term gain beats short-term pain

The downside looks less daunting with a long-term perspective. Declines can be painful, but missing the upside could be worse.

“None of us can predict what the market is going to do in the short term. But what we can do is identify good companies that we think are growing and will be better and bigger companies 10 years from now. If we get that right, through all sorts of market cycles, we are going to do well for our investors.” Tim Armour, Portfolio Manager

Swift and dramatic change can take a toll on investors. When markets falter, some may be inclined to reduce their exposure to equities. Yet history shows that periods of turmoil and steep market declines have subsequently proven to be among the best times to invest. Recent volatility may have caused some investors to panic and head for the exits, but a long-term focus can help put bear markets into perspective.

Since 1949 there have been nine periods of 20%-or-greater declines in the S&P 500. And while the average 33% decline of these cycles can be painful to endure, missing out on part of the average bull market’s 268% return could be even worse. The much shorter duration of bear markets (14 months on average), is also a reason why trying to time investment decisions can be difficult and is usually ill advised. Rather than indiscriminate selling, investors who are nervous about heightened volatility may want to consider objective-based funds with the flexibility to invest in a broad investment universe and a history of resilience during downturns. Investors should also re-examine their bond exposure for excess risk, as diversification from equities is one of the primary roles of fixed income in a balanced portfolio. Recent history, and the long-term record, shows how rapidly the market can turn. The volatility of returns of the S&P 500 dating back about 60 years indicates that investors may be doing real damage to their long-term finances by trying to time the market.

Why are some declines steeper? It’s the economy

Some of the most severe declines are associated with recessions. Short and not that sharp: Since 1945, nearly half of the declines have lasted less than eight months.

“The U.S. economy has been in an expansion for a while now, but I think it still has a ways to go. There doesn’t appear to be anything systemic, or any big imbalances, that we think are of a significant size and nature, that would push the U.S. economy into a recession within the next 12 to 18 months.” Darrel Spence, Economist

Every decline is different. A look back at U.S. stock market history since World War II shows that retreats have varied widely in intensity and length. But many declines during that period share a common pattern. In fact, nearly half of the declines since 1945 lasted less than eight months. And, in nearly one-third, the market was back at a new high less than 10 months after it peaked. One important factor in determining whether a decline is major or minor is what’s happening in the economy at the time. The median decline in the S&P 500 during retreats associated with a recession is 10.7% greater than those not associated with a recession, while the duration of the decline is substantially longer. The reason? Earnings fall much more dramatically around major pullbacks than around minor bear markets. Those declines in the lower centre of the chart are among the most serious and have all been associated with a recession. In relatively recent times, the financial crisis and the tech bust have both had significant impacts on investor sentiment. Market crises are traumatic and costly. But ultimately, the market has not only survived, but thrived. For more than a century, the U.S. market has endured wars, recessions, assassinations, bubbles and busts. And each time it has come back. Through it all, the market has demonstrated a remarkable strength and resiliency in the face of challenges.

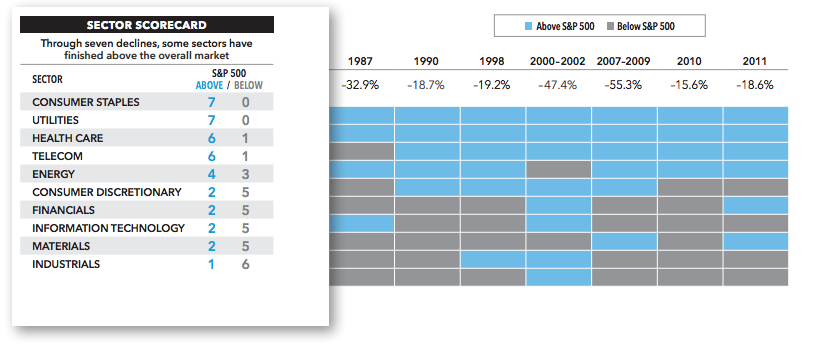

Some sectors can provide a measure of protection

Security selection and diversification can play a role when markets retreat. Index return doesn’t tell the whole story – some sectors have outpaced the market.

“The recent volatility has served as a reminder that markets can and will change, so we’ll continue to take a measured, long-term approach, with capital preservation very important in security selection and portfolio construction. I believe that in this environment, our ability to add value will come primarily through security selection backed by fundamental research.” Hilda Applbaum, Portfolio Manager

During the financial crisis that jolted the markets a decade ago, there was nowhere to hide. From its peak on October 9 October 2007, to its low on 9 March 2009, the S&P 500 dropped 55.3%. Every sector in the index suffered a serious setback, with the financials sector losing 81.7% of its value. But some sectors held up better than others. Consumer staples, for example, retreated about 29%, while health care dropped 38%. Small comfort, but still relative outperformance.

One of the consequences of the market’s decline during the financial crisis was that many investors questioned the value of diversification. During periods of instability, however, it’s important to maintain perspective, balance and flexibility. A portfolio that has the ability to nimbly explore evolving opportunity sets, using both allocation and security selection, can add value by investing in the right stocks and bonds based on a fundamental, valuation-based approach.

The benefits of diversification may have been lacking in 2008 and early 2009, but generally the principle remains fundamentally sound. Diversification through a strategic allocation to stocks and bonds around the world remains the hallmark of a portfolio that can help investors pursue their objectives in the long run. Such a portfolio can also help investors maintain a long-term perspective and place short-term drivers of the market into perspective.

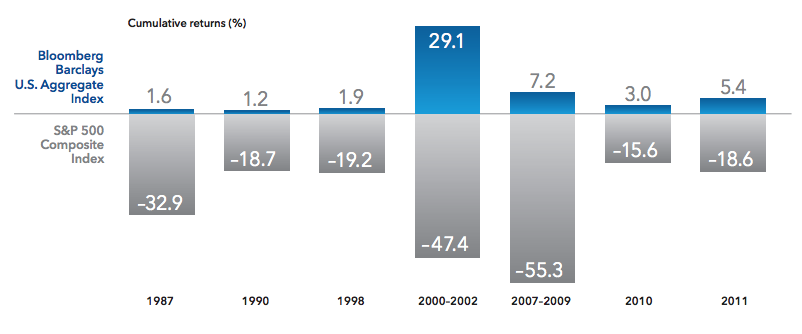

Buffers: Bonds can provide resilience when equities decline

Bonds can help mitigate volatility and provide balance in a diversified portfolio. Bonds have provided a measure of capital preservation in periods of market turbulence.

“There are four roles of fixed income in a diversified portfolio: diversification from equities, income, inflation protection and capital preservation. Nowhere in there does it say, ‘Try to be as equity-like as possible.’ That’s not the fifth role.” Mike Gitlin, Head of Fixed Income

Bonds play a variety of roles in a diversified portfolio, including providing income, capital preservation and inflation protection. They also help mitigate volatility. When equities are volatile, bonds typically provide balance to a portfolio. The chart shows that in market declines of at least 15% during the past three decades, bonds have provided relatively significant positive returns. That’s one of the reasons to invest in bonds, even in a rising rate environment.

The U.S. Federal Reserve raised interest rates three times in 2017 and once in 2018 to a range between 1.5% and 1.75%. Looking ahead, the Fed is expected to raise rates several times in 2018, but the Fed has indicated that rate hikes will be gradual, which can moderate the impact on the value of bonds. Investors who take a broadly diversified approach in their fixed income allocation and avoid excessive credit risk shouldn’t feel a dramatic impact from Fed policy

We believe the ability to provide resilience in periods of equity market corrections should be one of the goals of short-, intermediate- and core-bond strategies. Funds that provide diversification from equities can be good building blocks to help create durable portfolios. They also allow investors to rebalance their asset allocation at an appropriate time in market cycles. This approach can help investors achieve long-term investment and savings goals.

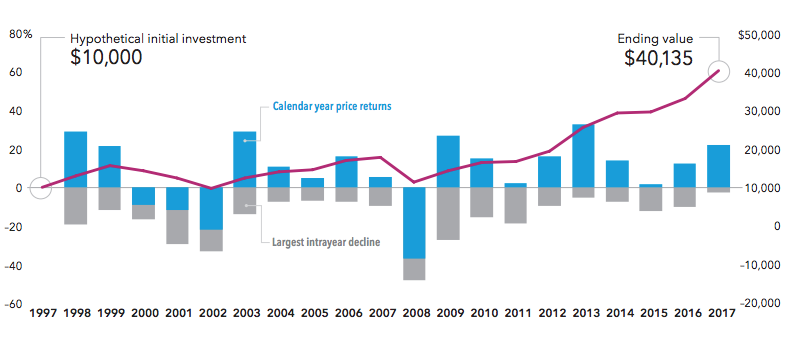

Long-term investors have weathered market declines

Don’t let intrayear declines derail long-term investments. Avoid the urge to time the market.

“We’ve recently been through a volatile and, in some ways, surprising period. When we go through times like this, it’s easy to respond by focusing on the short term. But I think the right thing to do in such an environment is to push your time horizon. You need to be thinking for the long run.” Carl Kawaja, Portfolio Manager

Declines happen, and it’s not easy to keep calm and carry on. Indeed, there is a natural human instinct to make changes, including portfolio adjustments, based on what one thinks will happen. This impulse isn’t confined to periods when stock prices are falling — it’s equally tempting when stocks are rising. Just as some investors are inclined to reduce equity exposure following a market decline, others are reluctant to maintain stock investments during a rising market because they worry that a correction might occur.

And the market provides plenty of opportunity to make changes. The S&P 500 has had intrayear declines every year for the last 20 years. But while the market has its declines, it also goes up. Overall, the market has gone up 16 out of 20 calendar years since 1997. As a result, a hypothetical initial investment of $10,000 in the stock market, as represented by the S&P 500, would have grown to an ending value of more than $40,000 as of December 31, 2017. During the past several years, the world’s equity markets have demonstrated a very low level of volatility. Volatility could be returning to more normal levels, which can represent an opportunity for long-term investors with a systematic investing plan. Regular investing does not ensure a profit or protect against losses. Investors should consider their willingness to keep investing when share prices are declining.

© 2018 Capital Group All rights reserved. CR-324827 AxJ

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Paul Hennessy is managing director, Australia & New Zealand, at Capital Group. As a relationship manager, he is responsible for covering the institutional client base in Australia and New Zealand. He has 33 years of investment industry experience and has been with Capital Group for eight years. Prior to joining Capital, he was head of Australian and New Zealand distribution for Macquarie Bank’s fund management division. Before that, he was global head of relationship management for Macquarie Securities and CIBC World Markets in North America.

1 topic

1 contributor mentioned

Paul Hennessy is managing director, Australia & New Zealand, at Capital Group. As a relationship manager, he is responsible for covering the institutional client base in Australia and New Zealand. He has 33 years of investment industry experience...

Expertise

Paul Hennessy is managing director, Australia & New Zealand, at Capital Group. As a relationship manager, he is responsible for covering the institutional client base in Australia and New Zealand. He has 33 years of investment industry experience...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management