TOL - 5th Nov, 2025

The most hated and confusing bull market in history – why stocks may have much further to run

Global markets are soaring but Citi says this bull run isn’t fuelled by euphoria. Nervous investors may be what keeps it alive.

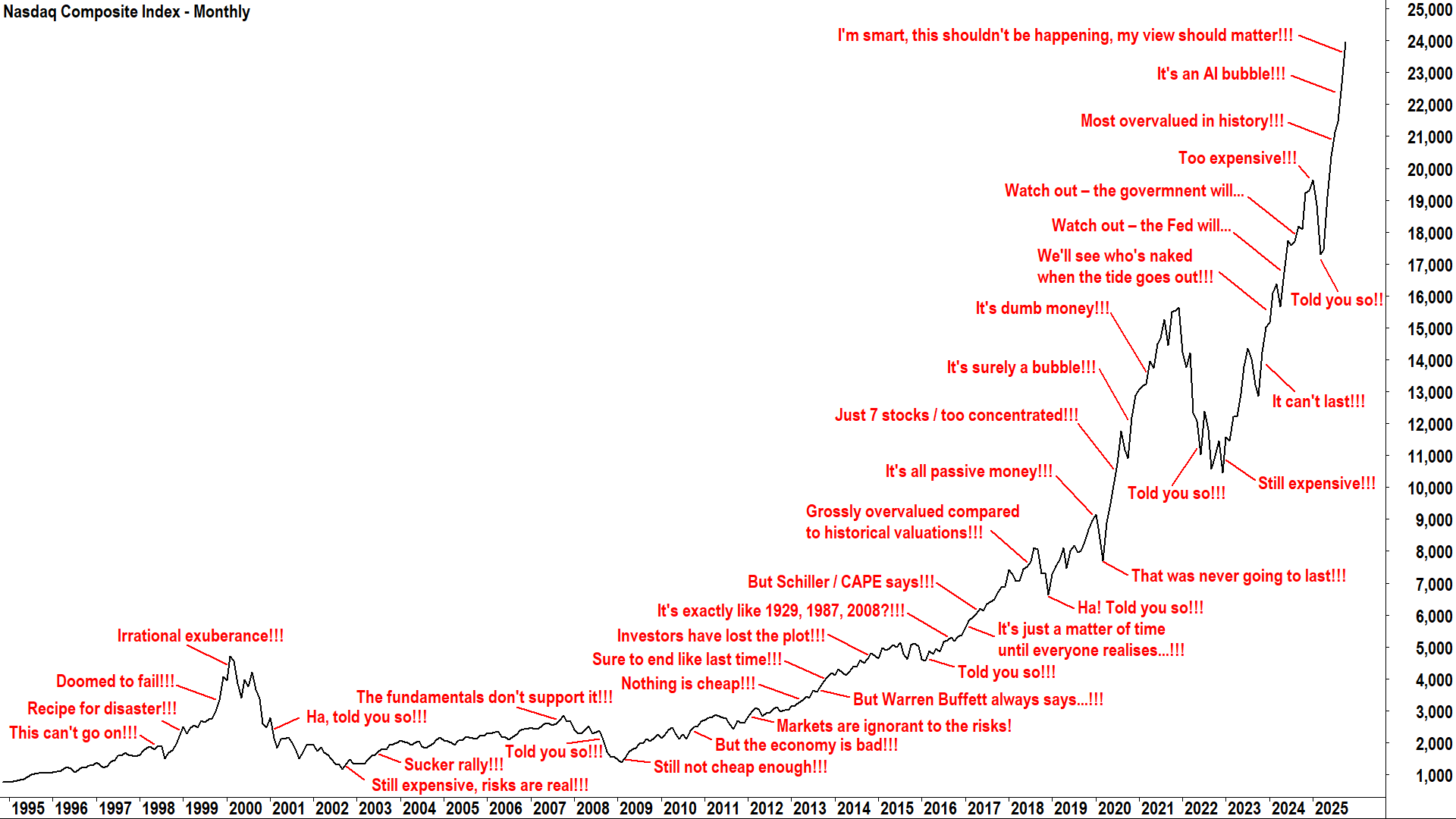

Stocks are ridiculously overvalued… They’ve never been this expensive!

It’s just a few stocks… It’s all because of inflated AI expectations!

It’s dumb money… It will end in tears… It always has!

For all the talk of irrational exuberance, it may surprise many to learn that the latest leg of the current global bull market is not being driven by euphoria at all – but by anxiety. In the US, the Nasdaq Composite, fuelled by high-growth, AI-linked tech giants, has surged to new record highs, as has the benchmark S&P 500.

Across Europe, benchmark indices like the DAX and CAC 40 are marking multi-year peaks, while in Asia and even here in Australia, equity benchmarks are pushing levels not seen in many years.

According to major investment bank Citi – markets aren’t irrational at all, but rather, more cautious than probably ever. In a new research note titled “Reluctant Bulls: Sentiment vs Positioning”, the bank measures the mood among institutional investors, noting an environment of uneasy participation. As the report’s authors put it, “we have been struck by the nagging concerns related to valuation, bubbles, credit and macros … yet allocations to US large cap equities appear steadfast.”

The result, Citi argues, is a market climbing a classic “wall of worry” – and, crucially, one that may still have further to run.

Nervous investors, committed capital

Citi’s strategists – Scott Chronert, Drew Pettit and Patrick Galvin – recently completed a round of client meetings across the US and Australasia. What they found was not a roomful of raging bulls, but an audience quietly fretting about valuations and the sustainability of the AI-fuelled rally.

“Valuation. Bubble. Valuation. Bubble,” the report begins, reflecting the repetitive cadence of investor responses. Even as global stock markets have rallied strongly this year, the conversations keep circling back to the same fears – that AI enthusiasm is overheated, that credit risks are building, and that labour-market resilience may not last.

And yet, despite this laundry list of worries, investors remain heavily allocated to equities. Citi’s own Levkovich Index – its long-running “Panic/Euphoria” gauge – shows positioning euphoria at levels comparable to the post-pandemic rebound. But that stands “in sharp contrast to a more nervous tone evident in our client discussions,” the analysts note. “Thus, the notion of reluctant bulls seems a more appropriate description for many investors in the current market environment.”

The underlying reason, Citi argues, is structural. Many global investors have little choice but to remain invested in US stocks. Domestic markets lack depth, liquidity and diversification, and the US still accounts for roughly 63% of the MSCI All Country World Index. For pension funds and sovereign wealth funds, opting out on the basis of one’s fears simply isn’t an option.

That reliance, Citi says, has created a peculiar mix of psychological caution and mechanical commitment – a generation of fund managers haunted by the memory of the tech bubble and GFC, but compelled by mandate to keep buying. “Even as markets have climbed higher,” Citi notes, “we have not seen bullish spikes in survey data … sentiment remains fairly neutral to slightly net bearish despite a solid climb from April lows.”

They add that mutual-fund and ETF allocations to US equities remain well above ten-year medians – yet a “barbell” has developed where cash holdings in money-market funds have also risen. In practice, this means investors are both risk-on and risk-averse at the same time: they’re buying the market because they must, but they’re hedging with cash buffers.

Citi’s US stock market targets

So, what does Citi recommend for investors looking to allocate capital to US equities? Despite acknowledging stretched valuations, the bank maintains an overall constructive stance, albeit with an emphasis on quality growth and selective positioning.

Base case: S&P 500 at 6,600 by year-end 2025, based on 21.4 times forecast 2026 earnings of US$308 per share.

Bull case: 7,200, assuming stronger 2026 earnings of US$316 and a richer 23 times multiple.

The S&P 500 closed at 6,890 on Wednesday, so Citi’s forecasts are hardly inspiring. Further, the bank notes the potential for downside should the earnings growth required to keep investors climbing the wall of worry not materialise: “We believe this ‘reluctant bull’ description sets up for a wall of worry whereby incrementally positive fundamentals will be rewarded – but disappointments will be seized upon with selling,” the analysts write.

We are entering a more volatile stage of this bull market.

Where Citi is adding and reducing risk now

Beyond short-term targets, Citi’s global asset-allocation team, led by Dirk Willer, has assessed the shifting risk landscape and issued its latest “house view” on where investors should be adding or cutting exposure. The message: stay pro-risk, stay selective, and keep the AI theme central to portfolio construction.

Adding to equities – particularly the US and China: Citi remains overweight global equities, with a clear preference for the United States and China. The team believes the AI-driven growth story is far from over and that “Fed cuts engineering another soft landing” should extend the cycle into 2026. They call this “early-bubble bullishness” – still supportive rather than speculative. In contrast, the UK remains a key underweight due to its defensive market composition and limited AI exposure

Staying short credit: Citi continues to view investment-grade credit as a macro hedge, arguing that “credit will benefit much less from a continued AI boom” and offers protection if the U.S. economy slows. Their strategists warn that “recent high-profile credit blow-ups have reaffirmed our view” and that the best risk-adjusted hedge for equity portfolios remains short U.S. and European IG credit

Rotating within commodities: Citi is switching from gold to base metals. After a powerful run-up, Citi has downgraded gold to neutral and upgraded base metals to overweight, citing “debasement fears overdone” and renewed optimism for global growth into 2026. Copper and aluminium are seen as major beneficiaries of the global AI infrastructure build-out, while gold’s “consensus long positioning” makes it vulnerable to profit-taking

Remaining long emerging markets and emerging market local bonds: Citi prefers emerging-market duration and FX carry trades, where volatility has eased and positioning remains “clean.” With the Fed expected to cut twice more this year, EM local bonds and currencies are expected to outperform relative to developed-market peers.

The net result: Citi remains pro-risk but pragmatic – bullish on equities, cautious on credit, constructive on commodities, and patient on duration. In their words, “additional risk should be deployed for year end, if we can have a decent US earnings season.”

The Wall of Worry

Nervous sentiment, the strategists argue, is not a contrarian signal of imminent collapse but a sign of durability. “Markets will continue to navigate euphoric positioning through the lens of quizzical, unsettled sentiment,” they write. “If incremental fundamentals prove supportive, this may define a classic wall of worry.”

For readers unfamiliar with the phrase, it’s often said that “every bull market climbs a wall of worry”. This means prices keep rising not because everyone is confident, but precisely because so many investors are still anxious – about valuations, earnings, geopolitics, or the next downturn. That scepticism prevents markets from overheating too soon and it leaves sidelined cash ready to chase every dip.

The paradox of the reluctant bull is that scepticism itself becomes fuel for the rally. As long as investors doubt its staying power, cash will remain on the sidelines, providing the latent demand required to keep stock prices climbing.

In my experience, it’s when confidence turns to complacency that risk truly builds. Citi’s report suggests we’re nowhere near that point yet – today’s investors are not dancing on the table – they’re worrying about valuations, about bubbles, and about history repeating. But they still have to buy – because not buying isn’t an option.

And that’s the cruel irony of professional money management. Sitting in cash during a bull market is a miserable state that no fund manager would wish on their worst enemy! Their job is to invest – and preferably to beat the market. If they don’t invest, they’re not really doing their job. So, reluctantly or otherwise, they will keep buying.

(References: Citi Research, “US Equity Strategy: Reluctant Bulls – Sentiment vs Positioning”, 24 Oct 2025; “Global Asset Allocation: House Views – October 2025”, 23 Oct 2025)

This article first appeared on Market Index on Friday 31 October, 2025.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

{kind=link}

5 topics

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment