The next stop for Webjet

Established in 1998, Webjet Limited is the foremost online travel agency (OTA) in Australia and New Zealand, leading the way in online travel tools and technology. Webjet says its focus has always been to offer the greatest convenience and choice by enabling customers to compare, combine and book the best domestic and international travel deals – including flights, hotel accommodation, holiday package deals, travel insurance and car hire worldwide. Their core business is the Australian online flight search site. Many people use this as a ‘billboard’ to compare flights, then book directly with the airlines to save on booking costs. Although this is an issue for the company, it is largely mitigated by Webjet relying on only a fraction of customer conversion. Webjet is at the forefront of online innovation – from the world’s first travel services aggregator technology through to leading the industry in blockchain innovation.

Growth Strategy

Webjet’s aim is to be a leading global business to business (B2B) operator. As businesses continue to grow in each region, Webjet is able to cross sell inventory offerings between the various businesses. This provides the broadest range of distribution capability to hotel partners, and delivering the broadest range of choice to agency partners.

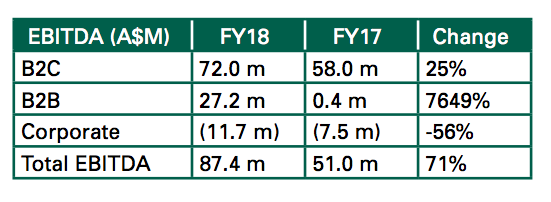

At their full year results presentation in August, Webjet’s B2B Hotels or WebBeds segment achieved bookings growth of 214%. While the segment benefitted from the acquisition of JacTravel (the last major acquisition by Webjet in 2017), organic bookings growth still rose an impressive 79% in FY 2018. Pleasingly, the B2B segment has a strong geographical footprint and is experiencing growth from all regions. Bookings grew 109% in the America’s, 235% in Europe, and 530% in Asia, leading to the segment making a meaningful contribution to the company’s overall earnings. This can be seen below.

Destinations of the World (DOTW) Acquisition

As a part of their stated B2B acquisition growth strategy, WEB recently acquired Destinations of the World (DOTW), a Dubai headquartered B2B accommodation wholesaler, for $240m. The acquisition will be funded by a fully underwritten 1 for 9 entitlement offer (priced at $11.50 a share) and $102m of debt funding.

DOTW operates throughout the Americas, Asia Pacific, Europe and the Middle-East connecting hoteliers with travel agents and 3rd party wholesalers. Management said the acquisition continues to cement WebBeds as the number 2 B2B player in the global market. DOTW is highly complementary to their existing portfolio and significantly increases exposure to the WebBeds presence in Europe and the Middle-East. In addition to providing 5,600 unique new contracts, the overlap in existing directly contracted hotels will deliver increased depth to our global inventory offering. DOTW is expected to contribute incremental earnings before interest, tax, depreciation and amortisation of at least $10m for the year to June 2019 and generate initial cost synergies of $4m.

November AGM Update

- Four-year compound headline and organic growth in customer bookings through 30 June 2018 were 44%, and 28%, respectively

- Total transaction value and Revenues were 54% higher than the prior year at $3bn and $291m, respectively

- EBITDA rose by 71% to $87.4m, and NPAT by 30% to $43.2 million

- Underlying EPS increased by 38% to 37.5 cents, and 20 cps in dividends were declared or paid.

- Webjet delivered a total shareholder return of 12% in FY18, on the back of 77% in FY17 and 148% in FY16. Management reiterated guidance and said it’s on track to deliver underlying EBITDA of at least $110 million from its existing operations this financial year.

These full year forecast’s do not include any synergies from the merger ( financials surrounding DOTW mentioned above).The update disappointed the market with the share price falling since the announcement.

Our View

In our view the stock sell down is an overreaction; Webjet has been wrongly grouped with other high P/E growth stocks that make little or no money. At current levels, the business trades on 20x earnings with forecast EPS growth of 30% - compelling value in our opinion.

Financials

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

1 stock mentioned

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Comments

Comments

Sign In or Join Free to comment